Business Case Development for M&A

The business case provides the financial justification for an acquisition, demonstrating that the deal will create shareholder value and generate acceptable returns on investment.

What is an M&A Business Case?

An M&A business case is a comprehensive financial analysis that:

- Quantifies value creation from the acquisition

- Projects financial performance of combined entity

- Calculates ROI and other return metrics

- Demonstrates deal meets hurdle rates

- Identifies key value drivers and risks

- Provides financial scenarios (base, upside, downside)

Purpose: Secure internal approval (Board, IC) by proving the deal makes financial sense.

Business Case Components

1. Transaction Overview

Deal Summary

- Target company name and description

- Deal structure (cash, stock, combination)

- Purchase price and enterprise value

- Financing approach

- Expected close timeline

Deal Economics at a Glance

| Metric | Value |

|---|---|

| Enterprise Value | $[X]M |

| Equity Value | $[X]M |

| EV/Revenue | [X.X]x |

| EV/EBITDA | [X.X]x |

| Premium to Market | [X]% |

| Synergy Value | $[X]M |

| Net Purchase Price | $[X]M (EV - Synergies) |

2. Financial Projections

Standalone Projections

Build 5-year standalone forecasts for both:

- Acquirer (current business trajectory)

- Target (based on historical performance + management projections)

Key Assumptions

- Revenue growth rates by segment

- EBITDA margins and operating leverage

- Capex and working capital needs

- Tax rates and NOLs

- D&A and amortization

Use conservative assumptions. Overly aggressive projections undermine credibility and lead to poor investment decisions. Apply haircuts to management's projections (typically 10-20%).

Pro Forma Projections

Combine acquirer + target with adjustments:

- Synergies (revenue and cost)

- Deal costs (one-time integration expenses)

- Purchase accounting impacts (step-up depreciation, goodwill)

- Financing costs (interest on new debt)

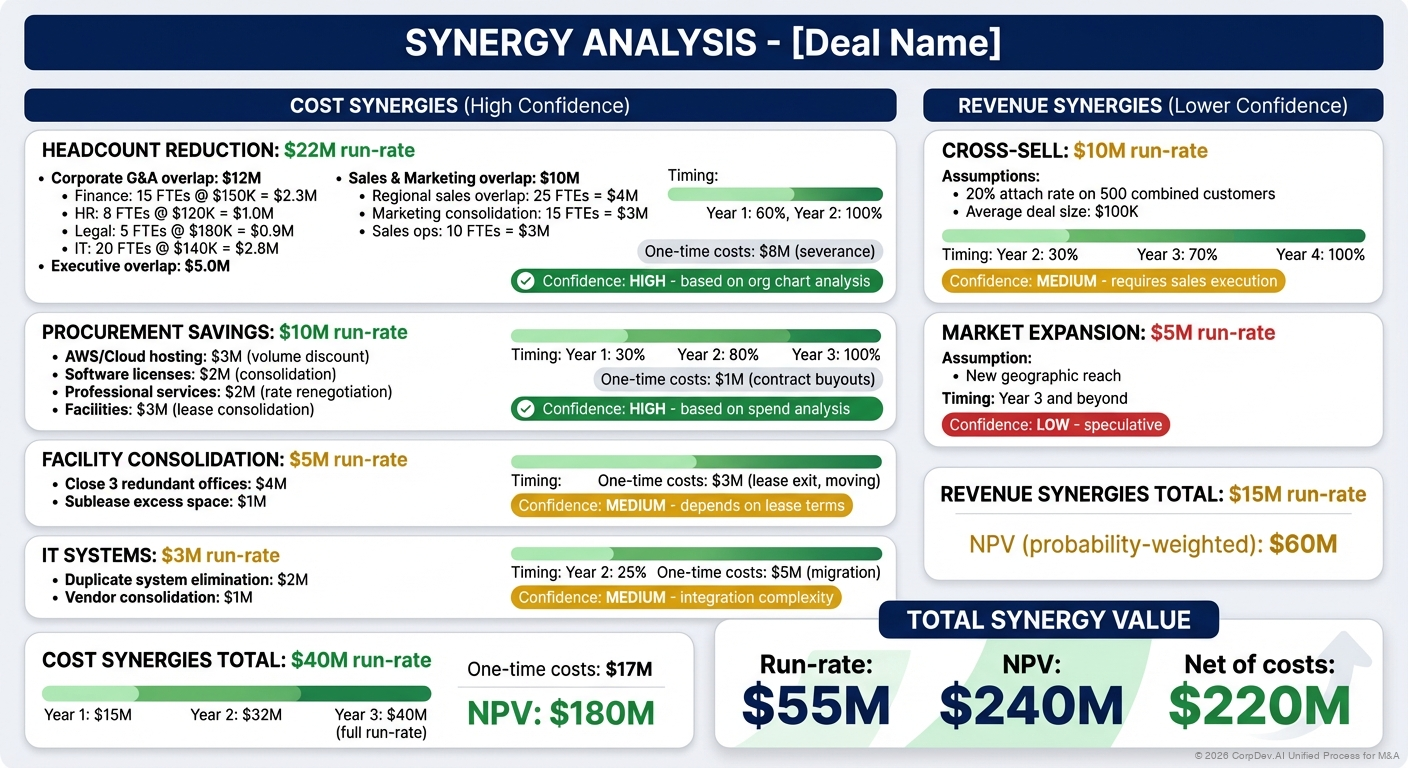

3. Synergy Analysis

Revenue Synergies

| Source | Year 1 | Year 2 | Year 3 | Steady State | Confidence |

|---|---|---|---|---|---|

| Cross-selling acquirer products to target customers | $[X]M | $[X]M | $[X]M | $[X]M | High/Med/Low |

| Cross-selling target products to acquirer customers | $[X]M | $[X]M | $[X]M | $[X]M | High/Med/Low |

| Price optimization | $[X]M | $[X]M | $[X]M | $[X]M | High/Med/Low |

| New product acceleration | $[X]M | $[X]M | $[X]M | $[X]M | High/Med/Low |

| Total Revenue Synergies | $[X]M | $[X]M | $[X]M | $[X]M |

Cost Synergies

| Source | Year 1 | Year 2 | Year 3 | Steady State | Confidence |

|---|---|---|---|---|---|

| Headcount reduction (overlapping roles) | $[X]M | $[X]M | $[X]M | $[X]M | High |

| Facility consolidation | $[X]M | $[X]M | $[X]M | $[X]M | High |

| Procurement/vendor optimization | $[X]M | $[X]M | $[X]M | $[X]M | Med |

| IT systems consolidation | $[X]M | $[X]M | $[X]M | $[X]M | Med |

| Shared services (HR, Finance, Legal) | $[X]M | $[X]M | $[X]M | $[X]M | Med |

| Marketing/sales efficiency | $[X]M | $[X]M | $[X]M | $[X]M | Med |

| Total Cost Synergies | $[X]M | $[X]M | $[X]M | $[X]M |

Synergy Realization Timeline

- Year 1: [X]% of run-rate synergies

- Year 2: [X]% of run-rate synergies

- Year 3: 100% of run-rate synergies

Cost synergies are more predictable than revenue synergies. Typical approach: underwrite cost synergies conservatively, treat revenue synergies as upside. Board approval should not depend on aggressive revenue synergy assumptions.

Integration Costs

| Category | Cost | Timing |

|---|---|---|

| Severance and retention bonuses | $[X]M | Year 1 |

| Facility closure/lease exit costs | $[X]M | Year 1-2 |

| IT migration and integration | $[X]M | Year 1-2 |

| Professional fees (legal, consulting) | $[X]M | Year 1 |

| Rebranding and marketing | $[X]M | Year 1-2 |

| Other one-time costs | $[X]M | Year 1-2 |

| Total Integration Costs | $[X]M |

Rule of Thumb: Integration costs typically = 10-15% of deal value for transformational deals, 5-10% for bolt-ons.

4. Valuation Analysis

Valuation Methods

Run multiple methodologies to triangulate fair value:

| Method | Implied Value | Weight |

|---|---|---|

| DCF Analysis (WACC-based) | $[X]M - $[X]M | 40% |

| Comparable Companies | $[X]M - $[X]M | 30% |

| Precedent Transactions | $[X]M - $[X]M | 30% |

| Weighted Average | $[X]M | 100% |

Purchase Price Analysis

Purchase Price: $500M

Less: Synergy PV (3-year): ($150M)

Net Purchase Price: $350M

Implied Net Multiples:

- Net EV/Revenue: 2.5x (vs. 3.5x gross)

- Net EV/EBITDA: 8.0x (vs. 11.5x gross)

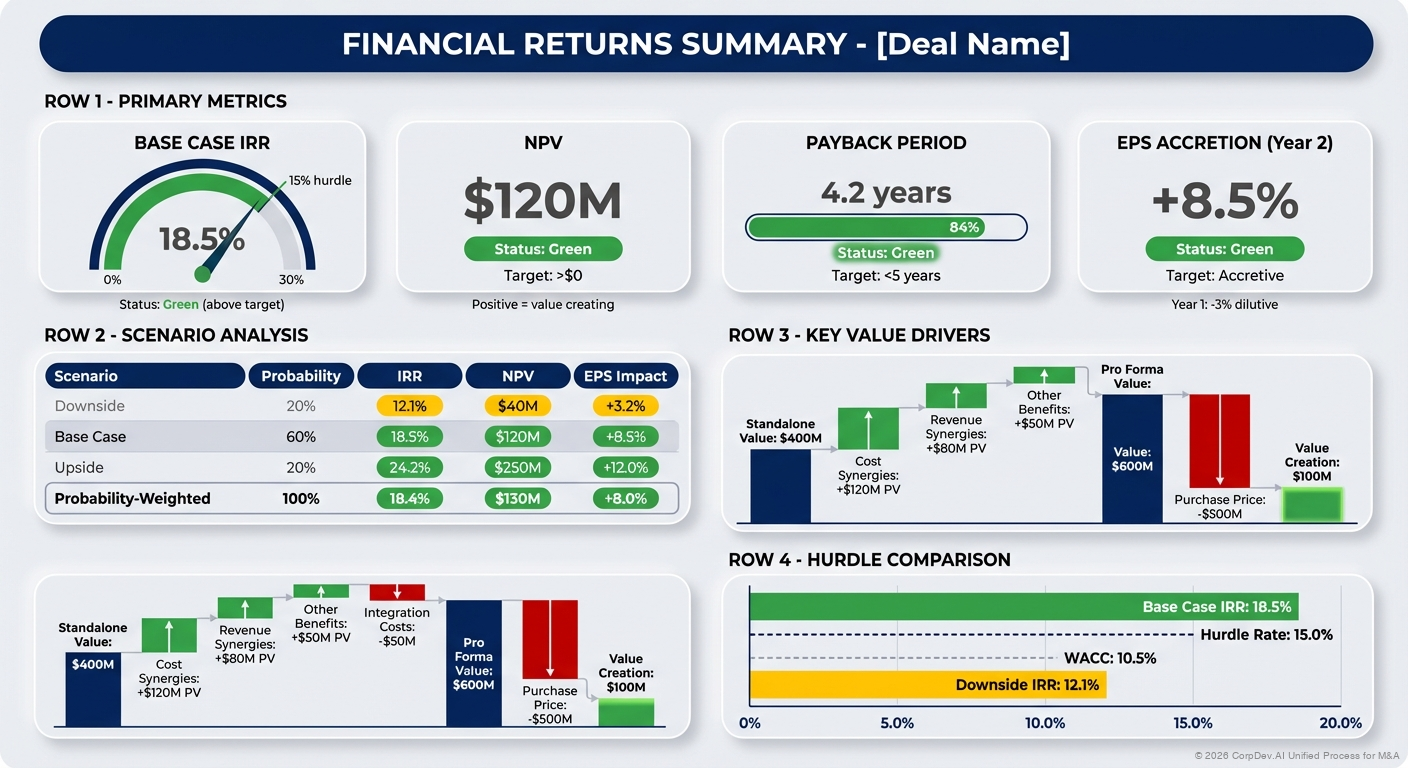

Value Creation Bridge

| Component | Value |

|---|---|

| Target Standalone Value | $400M |

| + Revenue Synergies (PV) | $80M |

| + Cost Synergies (PV) | $120M |

| + Other Benefits (PV) | $50M |

| - Integration Costs (PV) | ($50M) |

| = Total Pro Forma Value | $600M |

| - Purchase Price | ($500M) |

| = Value Creation | $100M |

5. Returns Analysis

Key Return Metrics

| Metric | Target | Base Case | Upside | Downside |

|---|---|---|---|---|

| IRR | >15% | 18.5% | 24.2% | 12.1% |

| Cash ROIC (Year 3) | >WACC+5% | 14.2% | 18.5% | 9.8% |

| NPV | >$0 | $120M | $250M | $40M |

| Payback Period | <5 yrs | 4.2 yrs | 3.1 yrs | 6.5 yrs |

| EPS Accretion (Year 2) | >5% | 8.5% | 12.0% | 3.2% |

IRR Calculation

Year 0: -$500M (purchase price) - $40M (transaction costs) = -$540M

Year 1: $45M (incremental FCF)

Year 2: $75M (incremental FCF)

Year 3: $95M (incremental FCF)

Year 4: $110M (incremental FCF)

Year 5: $125M (incremental FCF) + $600M (terminal value)

IRR = 18.5%

Return Hurdles by Deal Type

| Deal Type | Typical IRR Hurdle | Notes |

|---|---|---|

| Bolt-on acquisition | 15-20% | Lower risk, faster integration |

| Transformational deal | 20-25% | Higher risk premium required |

| Turnaround/distressed | 25%+ | Execution risk, uncertainty |

| Strategic/defensive | 12-15% | Strategic value beyond IRR |

6. Scenario Analysis

Three-Scenario Framework

Build detailed models for each scenario:

Base Case (60% probability)

- Management plan adjusted for conservatism

- 75% of identified synergies achieved

- Market conditions remain stable

- Integration proceeds on schedule

Upside Case (20% probability)

- Strong market tailwinds

- 100%+ synergies captured

- Revenue synergies materialize

- Faster integration

Downside Case (20% probability)

- Market headwinds or recession

- 50% of synergies achieved

- Integration delays/cost overruns

- Customer/employee attrition

Probability-Weighted Returns

Expected IRR = (60% × 18.5%) + (20% × 24.2%) + (20% × 12.1%) = 18.4%

Expected NPV = (60% × $120M) + (20% × $250M) + (20% × $40M) = $130M

Sensitivity Analysis

Test key assumptions:

| Variable | -20% | -10% | Base | +10% | +20% |

|---|---|---|---|---|---|

| Revenue Growth | 14.2% | 16.1% | 18.5% | 20.7% | 23.1% |

| Synergy Capture | 12.8% | 15.8% | 18.5% | 21.0% | 23.2% |

| Multiple on Exit | 15.1% | 16.9% | 18.5% | 19.8% | 21.0% |

| Integration Costs | 19.8% | 19.1% | 18.5% | 17.9% | 17.2% |

Tornado Chart: Identify which variables have greatest impact on returns.

7. Financial Impact

P&L Impact (Pro Forma)

| ($M) | Acquirer Standalone | Target Standalone | Synergies | Pro Forma Combined | % Change |

|---|---|---|---|---|---|

| Revenue | $2,000 | $500 | $50 | $2,550 | +27.5% |

| Gross Profit | $1,200 | $300 | $30 | $1,530 | +27.5% |

| - OpEx | ($800) | ($200) | $80 | ($920) | +15.0% |

| EBITDA | $400 | $100 | $110 | $610 | +52.5% |

| EBITDA Margin | 20.0% | 20.0% | - | 23.9% | +390bps |

Balance Sheet Impact

| ($M) | Pre-Deal | Deal Impact | Post-Deal |

|---|---|---|---|

| Cash | $300 | ($540) | ($240) |

| Goodwill | $500 | $350 | $850 |

| Total Assets | $3,000 | $810 | $3,810 |

| Debt | $800 | $540 | $1,340 |

| Equity | $2,200 | $270 | $2,470 |

| Net Debt | $500 | $780 | $1,280 |

Credit Metrics Impact

| Metric | Pre-Deal | Post-Deal (Year 1) | Target | Year 3 Pro Forma |

|---|---|---|---|---|

| Net Debt/EBITDA | 1.3x | 2.8x | <3.0x | 1.8x |

| EBITDA/Interest | 12.0x | 8.5x | >5.0x | 15.2x |

| FCF/Debt | 25% | 15% | >20% | 28% |

Equity Impact

| Metric | Pre-Deal | Post-Deal Y1 | Post-Deal Y3 |

|---|---|---|---|

| EPS | $2.50 | $2.58 (+3.2%) | $3.25 (+30%) |

| P/E Multiple | 18.0x | 17.5x | 18.0x |

| Share Price | $45.00 | $45.15 | $58.50 |

| Market Cap | $4.5B | $4.5B | $5.9B |

If deal is EPS-dilutive in Years 1-2, prepare strong narrative on long-term value creation and path to accretion. Public company boards are highly sensitive to near-term dilution.

8. Financing Plan

Sources & Uses

| Sources | $M | Uses | $M |

|---|---|---|---|

| Cash on hand | $240 | Purchase price | $500 |

| New debt | $300 | Refinance target debt | $100 |

| - | - | Transaction costs | $40 |

| Total Sources | $540 | Total Uses | $540 |

Financing Strategy

- Maintain investment-grade rating

- Target leverage of 2.5-3.0x Net Debt/EBITDA

- Refi existing revolver to $500M

- Commitment letter from banks secured

- Deleveraging plan: reach <2.0x by Year 3

Building the Business Case: Step-by-Step

Step 1: Gather Inputs

Required Data

- Target financial statements (3-5 years historical)

- Target management projections

- Acquirer financial model

- Market comps and transaction comps

- Synergy estimates from functional teams

- Integration cost estimates

- Financing terms and costs

Step 2: Build Financial Model

Model Structure

- Historical actuals (3-5 years for both companies)

- Standalone projections (5 years for both companies)

- Transaction assumptions (purchase price, structure, financing)

- Purchase price allocation (goodwill, intangibles, step-ups)

- Pro forma adjustments (synergies, integration costs, financing)

- Integrated projections (5 years pro forma P&L, BS, CF)

- Returns calculations (IRR, NPV, ROIC, payback)

- Scenarios (upside, base, downside)

- Sensitivities (key drivers, tornado chart)

Model Best Practices

- Separate assumptions from calculations

- Color code (blue = input, black = formula, green = link)

- Include scenario toggles

- Build circular reference solver for revolver/cash

- Include detailed footnotes and sources

Step 3: Validate Assumptions

Sanity Checks

- Revenue growth rates vs. historical and market growth

- Margins vs. industry benchmarks and historical trends

- Synergies vs. % of revenue/cost base (reasonability)

- Integration costs vs. deal size and complexity

- Valuation multiples vs. comps range

- Return metrics vs. hurdle rates and alternatives

Red Flags

- ❌ Revenue growth >2x historical without clear drivers

- ❌ Margin expansion >500bps without specific initiatives

- ❌ Synergies >30% of target revenue (too aggressive)

- ❌ No integration costs (unrealistic)

- ❌ IRR just barely clears hurdle (no margin of safety)

Step 4: Test Scenarios

Scenario Testing Questions

- What if revenue growth is 50% lower than projected?

- What if synergies are only 50% realized?

- What if integration takes 2x longer and costs 2x more?

- What if we face a recession in Year 2?

- What if key customers leave (customer concentration risk)?

Break-Even Analysis

- What's the minimum synergy capture needed to hit hurdle rate?

- What's the maximum price we can pay and still create value?

- How long can we afford delayed synergy realization?

Step 5: Prepare Recommendation

Investment Committee Memo

## Executive Summary

[2-3 paragraphs summarizing deal, strategic rationale, and financial recommendation]

## Strategic Rationale

[Why this deal makes strategic sense - see Strategic Rationale article]

## Financial Analysis

### Valuation

- Purchase Price: $[X]M

- Implied Multiples: [X.X]x Revenue, [X.X]x EBITDA

- Fair Value Range: $[X]M - $[X]M

- Premium/Discount: [X]%

### Returns

- Base Case IRR: [X]%

- Base Case NPV: $[X]M

- Payback Period: [X] years

- EPS Impact: [X]% accretive in Year 2

### Value Creation

- Total Synergies: $[X]M ($[X]M revenue + $[X]M cost)

- Net Value Creation: $[X]M

- ROIC (Year 3): [X]%

## Risk Assessment

[Key risks and mitigations - see below]

## Financing

[Sources/uses, impact on leverage, credit metrics]

## Recommendation

Recommend approval at purchase price of $[X]M, representing [X.X]x EBITDA multiple and [X]% IRR base case return.

Risk Assessment

Financial Risk Matrix

| Risk | Probability | Impact | Mitigation | Residual Risk |

|---|---|---|---|---|

| Revenue synergies not realized | Medium | High | Conservative base case excludes revenue synergies | Low |

| Integration costs exceed budget | Medium | Medium | 20% contingency in budget; phased approach | Low |

| Customer attrition | Low | High | Retention bonuses; customer communications plan | Medium |

| Talent loss | Medium | Medium | Retention packages for key employees | Low |

| Market downturn | Low | High | Conservative revenue assumptions; stress testing | Medium |

| Regulatory approval delay | Low | Medium | Early engagement with regulators; backup timing | Low |

| Financing market disruption | Low | High | Committed financing; deleveraging plan | Low |

| IT integration complexity | High | Medium | Phased migration; expert consultants engaged | Medium |

Risk Quantification

Model key risks in downside scenario:

- Revenue: -20% vs. base case

- Synergies: -50% vs. base case

- Integration costs: +100% vs. base case

Downside Still Acceptable?

- Downside IRR: [X]% (>12% minimum threshold ✓)

- Downside NPV: $[X]M (>$0 ✓)

- Downside leverage: [X.X]x (Investment grade maintained ✓)

Business Case Checklist

A Strong Business Case:

- Clear value creation story with quantified NPV/IRR

- Conservative assumptions that withstand scrutiny

- Realistic synergies with detailed source-by-source build-up

- Identified integration costs with contingency

- Multiple scenarios showing range of outcomes

- Sensitivity analysis on key value drivers

- Downside protection - acceptable returns even in pessimistic case

- Risk assessment with mitigation plans

- Financing plan that maintains financial flexibility

- Benchmarked returns vs. alternatives (buybacks, capex, other deals)

- Validation from finance, strategy, operations teams

- Board-ready presentation with clear recommendation

Common Mistakes

❌ Pitfalls to Avoid

Over-Optimism

- Using management projections without haircuts

- Aggressive revenue synergy assumptions

- Underestimating integration complexity and costs

- Ignoring implementation risks

Poor Modeling

- Errors in formulas or links

- Inconsistent assumptions across scenarios

- Missing key costs (TSAs, IT migration, retention)

- Circular references not properly handled

Weak Analysis

- Only running base case (no upside/downside)

- Limited sensitivity analysis

- Ignoring competitive response

- Not benchmarking against alternatives

Communication Failures

- Too complex - board can't follow logic

- Missing the "so what" - unclear recommendation

- Ignoring elephant in the room (e.g., EPS dilution)

- Lack of ownership - hedging on recommendation

✓ Best Practices

Be Conservative

- Haircut management projections by 10-20%

- Underwrite cost synergies only for approval

- Include realistic integration costs with contingency

- Stress test with downside scenarios

Show Your Work

- Detail all key assumptions

- Source data and benchmarks

- Build sensitivity and scenario analysis

- Model multiple valuation methods

Tell a Story

- Connect financial analysis to strategic rationale

- Explain how value will be created and captured

- Address risks head-on with mitigation plans

- Make a clear recommendation

Get Validation

- Finance team review of model

- Operating teams validate synergies

- External advisor benchmarking

- Board pre-wires and feedback

Templates & Tools

Business Case Executive Summary Template

# Business Case: [Target Name]

## Deal Overview

- **Target**: [Company name and description]

- **Purchase Price**: $[X]M ([X.X]x Revenue, [X.X]x EBITDA)

- **Structure**: [Cash/Stock/Mix]

- **Timing**: Close expected [Q/Year]

## Strategic Rationale

[2-3 sentences - why this deal makes strategic sense]

## Financial Highlights

| Metric | Value |

|--------|-------|

| **Base Case IRR** | [X]% |

| **NPV** | $[X]M |

| **Payback Period** | [X] years |

| **EPS Impact (Y2)** | [X]% |

| **Synergies (PV)** | $[X]M |

## Value Creation

- Total Value Creation: $[X]M

- Sources: $[X]M cost synergies, $[X]M revenue synergies, $[X]M other

- Net Purchase Multiple: [X.X]x EBITDA (vs. [X.X]x gross)

## Key Risks & Mitigations

1. [Risk #1]: [Mitigation]

2. [Risk #2]: [Mitigation]

3. [Risk #3]: [Mitigation]

## Financing

- **Sources**: $[X]M cash, $[X]M debt

- **Pro Forma Leverage**: [X.X]x (target <[X]x)

- **Credit Profile**: Maintains [investment grade/rating]

## Recommendation

✓ **RECOMMEND APPROVAL** at $[X]M purchase price

[1-2 sentences on why this deal creates value and meets hurdle rates]

Synergy Tracker Template

| Synergy Source | Dept Owner | Year 1 | Year 2 | Year 3 | Run-Rate | Confidence | Status |

|---|---|---|---|---|---|---|---|

| Headcount - Sales overlap | CRO | $2M | $4M | $5M | $5M | High | On track |

| Facility consolidation | CFO | $0 | $3M | $5M | $5M | High | Planning |

| Procurement savings | CPO | $1M | $2M | $3M | $3M | Medium | Analyzing |

| IT systems | CIO | $0 | $1M | $2M | $2M | Medium | Not started |

| Total | $3M | $10M | $15M | $15M |

Example: Business Case Summary

Acquisition of CloudSecure Inc.

Deal Overview

- Purchase Price: $500M ($425M EV + $75M net debt)

- Multiples: 3.5x Revenue, 11.5x EBITDA

- Structure: All cash, financed with $300M debt + $200M cash

Strategic Rationale

Acquire market-leading cloud security platform to complete our cybersecurity suite, enabling us to compete for $500M+ enterprise contracts and accelerate cloud transition.

Financial Returns (Base Case)

- IRR: 18.5% (vs. 15% hurdle)

- NPV: $120M

- Cash ROIC (Year 3): 14.2%

- Payback: 4.2 years

- EPS: 3% dilutive Year 1, 8% accretive Year 2

Value Creation

- Synergies (PV): $150M ($120M cost, $30M revenue)

- Net Purchase Multiple: 8.0x EBITDA (vs. 11.5x gross)

- Total Value Created: $100M NPV

Key Risks

- Customer overlap (15% revenue at risk) - Mitigated by retention plan

- Integration complexity - Mitigated by phased approach, expert advisors

- Debt covenant compliance - Mitigated by committed EBITDA growth, deleveraging plan

Financing

- $300M new term loan (5-year, L+275, investment grade terms)

- Pro forma leverage: 2.8x (delever to 1.8x by Year 3)

- Maintain BBB rating per rating agency pre-wire

Recommendation

✓ APPROVE acquisition at $500M. Deal delivers 18.5% IRR, creates $100M NPV, and accelerates our cloud security strategy by 2-3 years.

Key Takeaways

- Business case = financial proof that deal creates shareholder value

- Conservative assumptions are critical - boards value credibility over optimism

- Synergies must be detailed - source-by-source with ownership and timelines

- Scenario analysis is required - show upside, base, downside with probabilities

- Returns matter - IRR, NPV, ROIC must clear hurdle rates with margin of safety

- Integration costs are real - budget 10-15% of deal value for transformational deals

- Risk assessment matters - identify, quantify, and mitigate key financial risks

- Clear recommendation - don't hedge, make a call supported by analysis

The business case must stand on its own financially. Even with compelling strategic rationale, if the deal doesn't generate acceptable financial returns in a realistic base case scenario, it should not proceed. Strategic value should enhance returns, not justify inadequate returns.

Related Resources

- Deal Thesis Overview - Complete deal thesis framework

- Strategic Rationale - Building strategic justification

- Value Creation Planning - Synergy identification and capture

- DCF Analysis - Intrinsic valuation methodology

- Merger Model - Complete merger model template

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Thu Oct 30 2025 20:00:00 GMT-0400 (Eastern Daylight Time)