AI & SaaS M&A

The AI and SaaS sectors represent the most active and highest-valuation M&A markets. This guide covers sector-specific strategies, valuation frameworks, and key deal structures with extensive real-world examples.

Market Overview

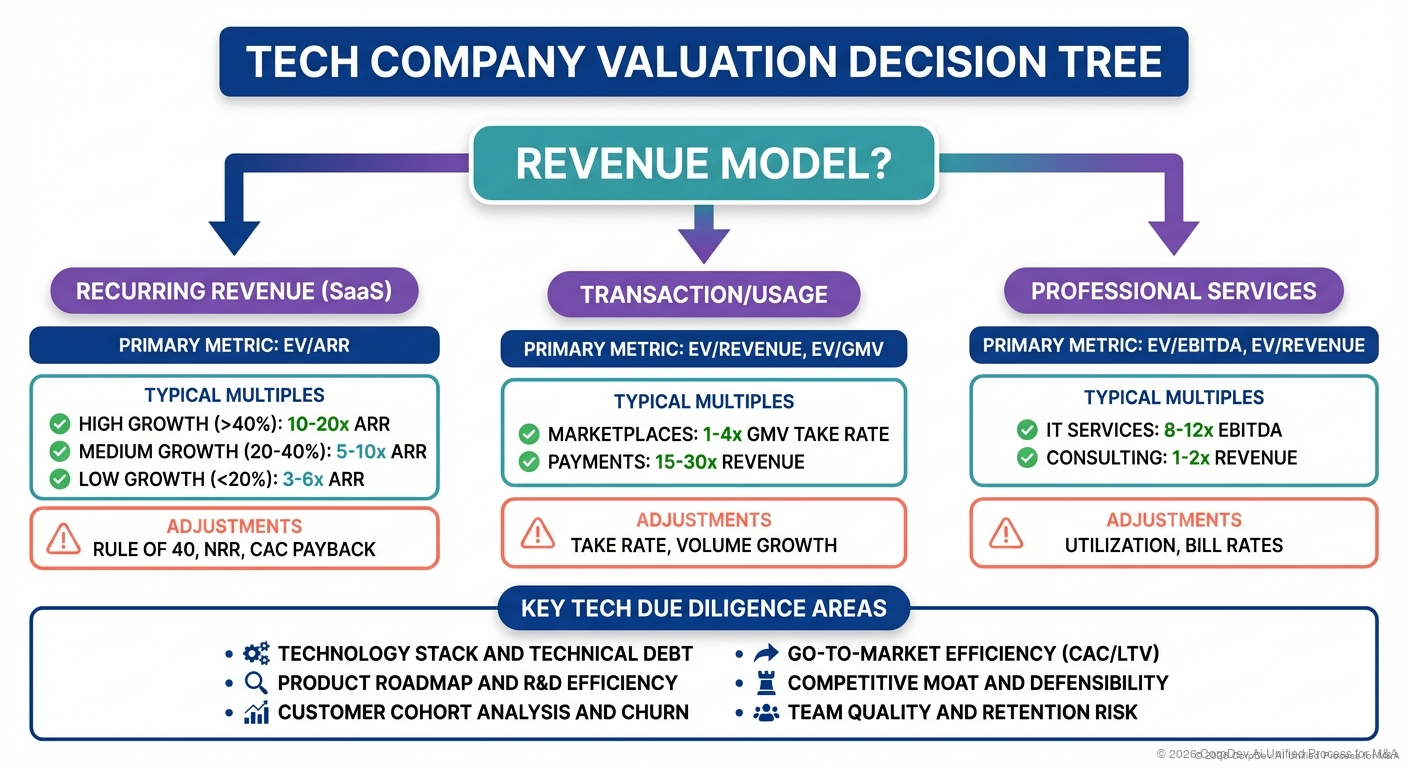

SaaS Valuation Framework

The ARR Multiple Method

Primary Valuation Methodology: Annual Recurring Revenue (ARR) multiples

Base Multiple Determination:

Growth Rate Impact (Primary Driver):

<20% YoY Growth: 2-4x ARR

20-30% YoY: 4-7x ARR

30-50% YoY: 7-12x ARR

50-75% YoY: 12-18x ARR

>75% YoY: 18-30x+ ARR

Profitability Adjustments (Rule of 40):

Rule of 40 = Growth% + FCF Margin%

>60: +3-5x premium

40-60: Market rate

<40: -2-4x discount

Net Revenue Retention (NRR):

>130%: +3-5x premium (best-in-class)

120-130%: +2-3x premium

110-120%: +1-2x premium

100-110%: Base multiple

<100%: -3-5x discount (churning)

Market Position:

Category Leader (>40% share): +2-4x

Strong #2 (#20-40% share): +1-2x

Challenger (<20% share): Base

Declining/Legacy: -3-5x

Complete Example:

Company: Vertical SaaS Platform

ARR: $100M

Growth Rate: 60% YoY

FCF Margin: 5%

Rule of 40: 65

NRR: 125%

Market Position: Category leader (#1, 45% market share)

Gross Margin: 85%

Step-by-Step Valuation:

1. Base Multiple (60% growth): 15x ARR

2. Profitability Adjustment (Rule of 40 = 65): +3x

Adjusted: 18x ARR

3. NRR Premium (125%): +2x

Adjusted: 20x ARR

4. Market Position (#1 leader): +2x

Adjusted: 22x ARR

5. Final Valuation: $100M × 22 = $2.2B

Valuation Range: $2.0B - $2.5B

AI Company Valuation Framework

Different from SaaS: Early revenue, massive TAM potential, talent value

AI Valuation Components:

1. Technology/Model Value:

Factors:

- Model performance vs. benchmarks

- Proprietary training data

- Inference efficiency/cost

- Model architecture advantages

- Patent portfolio

Valuation:

State-of-art model: $50-200M base value

Incremental model: $10-50M base value

Commodity model: $5-10M base value

2. Talent Value (often dominates):

Elite AI Researcher Value: $5-15M per person

Strong Engineer: $2-5M per person

Average Team Member: $500K-1M per person

Example Team Valuation:

5 elite researchers × $10M = $50M

20 strong engineers × $3M = $60M

15 other team members × $750K = $11M

Total Talent Value: $121M

Rule of Thumb: $2-4M per high-quality AI employee

3. Data Assets:

Proprietary Training Data Value:

- Unique dataset: $20-100M+

- Competitive advantage from data

- Difficult/impossible to replicate

- Regulatory moats (healthcare, finance)

Example: Medical imaging AI with 10M labeled scans

- Cost to recreate: $50M+

- Time to recreate: 5+ years

- Regulatory approvals included

- Value: $100M+ for data alone

4. Commercial Traction:

If revenue exists, apply SaaS multiples:

- ARR × growth multiple

- Often 20-50x ARR for high-growth AI

If pre-revenue:

- Pipeline × conversion rate × 10x

- Customer LOIs × 5-10x

- POC value estimation

Complete AI Valuation Example:

Company: Computer Vision AI for Manufacturing

Revenue: $10M ARR (early traction)

Growth: 300% YoY

Team: 40 people (8 PhD researchers, 25 engineers)

Data: Proprietary defect dataset (1M images)

Technology: State-of-art model, 95% accuracy vs 85% competition

Valuation Components:

1. Revenue Multiple: $10M × 25x (300% growth) = $250M

2. Talent Value:

8 PhD researchers × $8M = $64M

25 engineers × $3M = $75M

7 other × $1M = $7M

Total: $146M

3. Data Asset: $50M (proprietary manufacturing defects)

4. Technology Premium: $30M (SOTA model advantage)

Total Value = MAX(Revenue Multiple, Talent+Data+Tech)

= MAX($250M, $226M)

= $250M base

AI Premium (strategic value, platform potential): +$100M

Final Valuation: $350M

Per Person: $8.75M (typical for elite AI company)

Strategic Rationales for SaaS M&A

1. Platform Consolidation (The HubSpot Model)

Strategy: Build comprehensive platform by acquiring point solutions

Real-World Example: HubSpot's Platform Assembly

Vision: All-in-one marketing, sales, and service platform for SMBs

Acquisition Timeline:

2016: Kemvi ($20M est) - Predictive lead scoring (AI)

- Added AI capabilities early

- Improved lead qualification

2018: Motion AI ($10M est) - Chatbot platform

- Conversational marketing

- Automated customer engagement

2019: PieSync ($7.5M) - Data synchronization

- App integration platform

- Eliminated data silos

2020: The Hustle ($27M) - Business newsletter

- Content/media acquisition

- Audience building

2021: Clearbit ($150M) - Data enrichment

- B2B data intelligence

- Improved targeting and personalization

2023: Cacheflow ($20M est) - Sales enablement

- Quote-to-cash functionality

Strategic Logic:

Core Platform: Marketing, Sales, Service Hub (built organically)

Acquisitions: Enhance core with AI, data, automation, content

Financial Impact:

Pre-2016: $270M revenue, growing 50%

2024: $2.5B+ revenue, growing 25%

Acquisition Contribution:

- Direct revenue: ~$200M (from acquired products)

- Indirect (improved core platform): ~$500M

- Total contribution: ~$700M (28% of revenue)

Customer Impact:

- ARPU increased 2x ($500/mo → $1,000/mo)

- Products per customer: 1.3 → 2.8

- NRR improved: 98% → 115%

- Churn reduced: 12% → 6%

Key Success Factors:

- Tightly integrated into core platform

- Maintained affordable SMB pricing

- Consistent product experience

- Cross-sell motions built into product

- Free tools drive acquisition funnel

2. The "Land and Expand" Acquisition

Strategy: Acquire companies with high NRR and expansion potential

Example: Twilio's Communication Platform Build

2018: SendGrid ($3B) - Email API

ARR: $150M

NRR: 115%

Growth: 28% YoY

Logic: Add email to communication platform

Integration:

- Maintained brand for 2 years

- Cross-sold to Twilio base

- Integrated into Flex platform

Results (Year 3):

- SendGrid revenue: $250M (+67%)

- Cross-sell penetration: 35% of Twilio customers

- Combined ARPU up 40%

2020: Segment ($3.2B) - Customer data platform

ARR: $175M

NRR: 130% (exceptional)

Growth: 40% YoY

Logic: Data layer for communication

Integration Strategy:

- Keep separate GTM initially

- Integrate product deeply

- Build Twilio Engage on Segment

Expected Results:

- Segment standalone: $300M ARR (projected)

- Twilio Engage (built on Segment): $500M+ ARR potential

- Platform effect: 2x value creation

Strategic Outcome:

- Twilio revenue: $1B (2018) → $4B+ (2024)

- Acquisitions drove 40% of growth

- Transformed from SMS API to customer engagement platform

3. AI Talent Acquisition

Strategy: Acquire AI companies primarily for research teams

Real-World Example: Apple's AI Acqui-Hire Strategy

Strategy: Build AI capabilities through strategic acqui-hires

Acquisition History (2016-2024):

2016: Turi ($200M) - Machine learning platform

Team: 30 people, several PhD researchers

Value: $6.7M per person

Outcome: Became Core ML team

2017: Lattice Data ($200M) - AI for dark data

Team: 20 people

Value: $10M per person

Outcome: Siri intelligence improvements

2018: Silk Labs ($50M est) - On-device AI

Team: 15 people

Value: $3.3M per person

Outcome: Neural Engine development

2019: Xnor.ai ($200M) - Edge AI

Team: 25 people

Value: $8M per person

Outcome: On-device ML improvements

2020: Voysis ($50M est) - Natural language

Team: 30 people, Dublin-based

Value: $1.7M per person

Outcome: Siri improvements

2020: Inductiv ($50-100M est) - Data science automation

Team: Waterloo researchers

Outcome: Siri/ML platform

2023: WaveOne ($50M est) - AI video compression

Team: 10-15 people

Outcome: Video streaming optimization

Total Investment: ~$1B over 7 years

Total Team Members Acquired: ~150 AI specialists

Average Cost per Person: $6.7M

Strategic Impact:

- Built world-class AI team without poaching

- Acquired specific capabilities (on-device, compression, NLP)

- Technology integrated into iOS/Siri/ML platform

- Avoided public recruiting wars with Google/Microsoft

Integration Pattern:

- Shut down acquired products

- Integrate team into Apple AI

- Technology becomes platform features

- Team stays 3-5 years (typical)

4. Vertical SaaS Roll-Up

Strategy: Consolidate fragmented vertical markets

Example: Vista Equity's Blueprint

Model: Acquire vertical SaaS companies, apply operating playbook, roll-up

Typical Deal Profile:

- Vertical: Legal, Healthcare, Government, etc.

- ARR: $20-100M

- Growth: 15-30%

- Purchase Multiple: 5-8x ARR

- Hold: 4-7 years

- Exit Multiple: 10-15x ARR

Value Creation Levers:

1. Pricing Optimization: +10-20% revenue

2. Sales Efficiency: +15-25% productivity

3. Product Development: Focused roadmap

4. Operating Leverage: +800-1200bps EBITDA margin

Example Portfolio Company Path:

Entry:

- $50M ARR

- 20% growth

- 15% EBITDA margin

- Purchase: $350M (7x ARR)

Vista Operating System Applied:

Year 1: Pricing +15%, margins +5pts

Year 2: Sales efficiency +20%, growth +5pts

Year 3: Operating leverage, margins +10pts total

Exit (Year 5):

- $120M ARR (19% CAGR)

- 25% growth (improved)

- 30% EBITDA margin (+15pts)

- Exit: $1.4B (12x ARR)

- Return: 4x MOIC, 32% IRR

Actual Examples:

- Marketo: $1.8B entry → $4.75B exit (2.6x in 2 years)

- Finastra: Rolled up 5 financial software companies

- Greenway Health: Healthcare vertical consolidation

Landmark AI M&A Deals

1. Microsoft + Nuance Communications ($19.7B, 2021)

Deal Structure:

Target: Nuance Communications

Purchase Price: $19.7B ($56/share, 23% premium)

Revenue: $1.5B

ARR Growth: 8%

Multiple: 13x revenue

Rationale: Healthcare AI + cloud

Strategic Logic:

Why Microsoft Paid Premium for Slow-Growth Company:

1. Healthcare Cloud Strategy:

- Healthcare is $1T+ cloud opportunity

- Nuance has 10,000+ healthcare customers

- 77% of US hospitals use Nuance

- Entry point into healthcare vertical

2. AI/Voice Technology:

- 30+ years of voice/NLP IP

- Medical transcription AI (90% market share)

- Virtual assistant technology

- Training data from billions of medical conversations

3. Strategic Defense:

- Prevent Amazon/Google acquisition

- Healthcare is strategic priority for all clouds

- First-mover advantage in healthcare AI

4. Platform Value:

- Sell Azure to Nuance customers

- Build healthcare-specific AI models

- Combine with Teams for healthcare communication

- Data for training healthcare AI

Financial Justification:

Standalone Value: $10B (based on slow growth)

Strategic Value to Azure Cloud: +$5B

Defensive Value (blocking competition): +$3B

Healthcare AI Platform Value: +$2B

Total Value: $20B

Outcome (Year 3):

- Integrated into Microsoft Cloud for Healthcare

- Azure adoption among Nuance customers: 60%+

- Healthcare cloud revenue: $2B+ (including Nuance)

- Strategic value realized

2. Salesforce + Slack ($27.7B, 2020)

Deal Structure:

Target: Slack Technologies

Purchase Price: $27.7B

Revenue: $900M ARR

Growth: 40% YoY

Multiple: 31x revenue (54% premium)

Structure: $27.7B cash + stock

Strategic Logic:

Why Salesforce Overpaid (Apparently):

Standalone Analysis:

Slack Revenue: $900M

Fair Multiple (40% growth): 15-20x

Fair Value: $13.5-18B

Price Paid: $27.7B

Premium: $10-14B "overpayment"

Strategic Justification:

1. Defensive (Microsoft Teams Threat):

- Microsoft bundling Teams with Office 365

- Slack losing enterprise deals to Teams

- Threat to Salesforce's enterprise presence

- Defensive value: $5B+

2. Collaboration Platform Play:

- Salesforce needed workplace collaboration

- Build vs Buy: 5+ years to build, might fail

- Time value of speed: $3B+

3. Platform Effects:

- App integration layer (Slack Connect)

- Customer communication channel

- Internal collaboration for Salesforce apps

- Platform value: $5B+

4. Customer Retention:

- Stickier platform with collaboration

- Increased switching costs

- Higher Net Revenue Retention

- Retention value: $2B+

Total Strategic Value: $15B

Premium "Overpayment": $10-14B

Strategic Value: $15B

Net: Justified (barely)

Outcome (Year 3):

- Integration ongoing

- Slack integrated into Salesforce workflows

- Cross-sell: 30% of Salesforce customers using Slack

- Microsoft still winning enterprise deals

- Verdict: TBD, likely overpaid but strategic rationale sound

3. Adobe + Figma ($20B, 2022 - BLOCKED)

Deal Structure:

Target: Figma

Proposed Price: $20B

Revenue: $400M ARR

Growth: 100%+ YoY

Implied Multiple: 50x revenue

Status: Blocked by regulators (2023)

Why $20B for $400M ARR Company?

Financial Analysis:

Figma ARR: $400M

Growth: 100%+ YoY

5-Year Revenue Projection: $6B+ ARR

Multiple at Scale: 10-15x

Future Value: $60-90B

DCF to 2027:

Year 1: $800M (100% growth)

Year 2: $1.4B (75% growth)

Year 3: $2.2B (55% growth)

Year 4: $3.2B (45% growth)

Year 5: $4.5B (40% growth)

Terminal Value (10x multiple): $45B

Discount Rate: 12%

PV of Future Cash Flows: $27B

Adobe's Valuation: $20B = 25% discount to intrinsic value

Strategic Logic:

1. Existential Threat:

- Figma disrupting Adobe's creative cloud

- Designers switching from Adobe XD to Figma

- Multiplayer/collaborative design = future

- Threat to $15B+ creative cloud business

2. Network Effects:

- 4M users (vs Adobe's 26M)

- But growing 2x faster

- Viral adoption in design teams

- Intercepting next generation of designers

3. Platform Shift:

- Cloud-native collaborative design

- Adobe late to this shift

- Faster to acquire than rebuild

- Time value: 3-5 years

Defensive Value Analysis:

If Figma continues growing:

- 2027 Figma standalone value: $60B+

- Adobe Creative Cloud cannibalization: -$5B value

- Total cost of not acquiring: $65B+

Therefore $20B acquisition price = 70% discount to cost of not acquiring

Outcome:

- Acquisition blocked by regulators (anti-trust)

- Adobe paid $1B breakup fee

- Figma continuing independent growth

- Adobe building competitive products

- Lesson: Defensive acquisitions face regulatory scrutiny

SaaS-Specific Due Diligence

Financial Metrics Deep Dive

Critical SaaS Metrics to Validate:

1. Annual Recurring Revenue (ARR) Quality:

Components to Verify:

- New ARR (new customers)

- Expansion ARR (upsells)

- Contraction ARR (downgrades)

- Churn ARR (lost customers)

Red Flags:

- High % of ARR from single customer (>10%)

- Non-recurring revenue masked as ARR

- Professional services revenue included

- Contract guarantees not actual usage

- Multi-year contracts front-loaded

Validation:

- Review top 20 customer contracts

- Verify payment history

- Check auto-renewal rates

- Confirm usage vs. contracted amounts

2. Net Revenue Retention (NRR):

Formula:

NRR = (Starting ARR + Expansion - Contraction - Churn) / Starting ARR

Cohort Analysis (Critical):

Must analyze by customer cohort:

- Year 1: Typically 85-95% (deployment phase)

- Year 2: 100-120% (expansion begins)

- Year 3+: 120-140% (mature, expanding)

**Red Flags:**

* [ ] NRR declining quarter-over-quarter

* [ ] Expansion masking high churn

* [ ] Few customers reaching Year 3+

* [ ] Expansion concentrated in few accounts

**Best Practice:**

* [ ] Request 3-year cohort retention analysis

* [ ] Plot NRR by vintage

* [ ] Understand expansion motions

**3. Customer Acquisition Cost (CAC) and Payback:**

CAC = (Sales + Marketing Costs) / New Customers Acquired

CAC Payback Period = CAC / (ACV × Gross Margin)

Benchmarks:

<12 months: Excellent

12-18 months: Good

18-24 months: Acceptable

24 months: Concerning

Deep Dive Required:

- CAC by channel (inbound, outbound, partner)

- CAC by segment (SMB, Mid-Market, Enterprise)

- CAC trend (improving or worsening?)

- Payback by cohort

Red Flags:

- CAC increasing faster than ACV

- Payback period extending

- Heavy discounting to acquire

- High churn in early cohorts (bad CAC:LTV)

4. Logo Retention vs. Dollar Retention:

Logo Retention: % of customers that renew

Dollar Retention (NRR): % of ARR retained + expanded

Example Scenario:

Logo Retention: 85%

NRR: 115%

What this means:

- Losing 15% of customers (concerning)

- But expanding remaining 85% by 35%

- Expansion masking churn

Ideal:

Logo Retention: >90%

NRR: >110%

**Red Flags:**

* [ ] Logo retention <80%

* [ ] Gap between logo and dollar retention >20pts

* [ ] Indicates product/market fit issues

</div>

### Technology Due Diligence for AI Companies

**1. Model Performance Validation:**

* [x] Benchmark against SOTA (state-of-art)

* [x] Test on held-out datasets

* [x] Validate accuracy claims

* [x] Check inference latency/cost

* [x] Evaluate edge cases and failures

**2. Data Quality and Rights:**

* [x] Training data sources and licensing

* [x] Data labeling quality

* [x] Bias testing and mitigation

* [x] Data refresh cadence

* [x] Proprietary vs. public data

**3. Infrastructure and Scalability:**

* [x] Training infrastructure costs

* [x] Inference costs at scale

* [x] Model serving architecture

* [x] Scaling characteristics

* [x] Cloud dependencies and costs

**4. IP and Competitive Moats:**

* [x] Patent portfolio

* [x] Proprietary algorithms

* [x] Data moats

* [x] Model architecture advantages

* [x] Regulatory barriers (FDA, etc.)

**5. Team and Retention:**

* [x] Publication history (top conferences?)

* [x] GitHub contributions

* [x] PhD credentials and advisors

* [x] Previous company experience

* [x] Retention packages and golden handcuffs

## Integration Playbooks

### SaaS Platform Integration (6-12 Months)

**Phase 1: Months 1-3 (Stabilize)**

**Week 1-2: Day 1 Priorities**

* [ ] Customer communication (joint email)

* [ ] Support continuity plan

* [ ] Product roadmap clarity

* [ ] Sales compensation clarity

* [ ] Employee retention packages

**Week 3-4: Quick Wins**

* [ ] SSO integration (if not done)

* [ ] Cross-sell training for sales

* [ ] Joint customer success playbook

* [ ] Marketing integration (website, content)

**Month 2: Technical Planning**

* [ ] API integration design

* [ ] Data sharing architecture

* [ ] Product roadmap integration

* [ ] Sunset/migration planning

**Month 3: Organization Design**

* [ ] Combined team structure

* [ ] Role clarity and redundancy elimination

* [ ] Compensation alignment

* [ ] Office consolidation planning

**Phase 2: Months 4-6 (Integrate)**

**Product Integration:**

* [ ] API connections live

* [ ] Data flowing between products

* [ ] Single sign-on complete

* [ ] Unified billing (if applicable)

**Go-to-Market Integration:**

* [ ] Combined sales pitch

* [ ] Cross-sell quotas and comp

* [ ] Channel partner training

* [ ] Joint marketing campaigns

**Operations Integration:**

* [ ] Finance systems combined

* [ ] HR systems integrated

* [ ] IT infrastructure consolidated

* [ ] Procurement combined

**Phase 3: Months 7-12 (Optimize)**

**Deep Integration:**

* [ ] Product UI/UX consistency

* [ ] Shared services (auth, payments, etc.)

* [ ] Data warehouse integration

* [ ] ML/analytics integration

**Value Capture:**

* [ ] Aggressive cross-sell to both bases

* [ ] Pricing and packaging optimization

* [ ] Upsell and expansion motions

* [ ] Cost synergies (headcount, infrastructure)

**Metrics to Track:**

* [ ] Cross-sell penetration (target: 30-50% by Month 12)

* [ ] ARPU improvement (target: 25-40% increase)

* [ ] NRR improvement (target: +5-10 points)

* [ ] Churn impact (keep flat or improve)

## Common Pitfalls

### 1. Overpaying Based on Growth Alone

**Problem**: High growth without understanding CAC:LTV and unit economics

Example: "Hyper-Growth" SaaS Company

Surface Metrics (Attractive):

- ARR: $50M

- Growth: 150% YoY

- Valuation: $50M × 20x = $1B

Due Diligence Reveals:

- CAC: $50,000

- ACV: $25,000

- CAC Payback: 24 months

- Churn: 30% annually

- LTV:CAC ratio: 1.5:1 (should be >3:1)

Reality:

- Company burning cash to grow

- Unit economics don't work

- Growth unsustainable without subsidy

- True value: $200-300M, not $1B

Lesson: Validate unit economics, not just growth

### 2. Ignoring Integration Complexity

**Problem**: "We'll figure out integration later"

Example: Salesforce + Mulesoft ($6.5B, 2018)

Expectation:

- 6-month integration

- Immediate cross-sell to Salesforce base

- Synergies in Year 1

Reality:

- Integration took 18+ months

- Complex developer product

- Sales reps struggled to position

- Synergies delayed 12+ months

Impact:

- Stock declined post-acquisition

- Lower-than-expected synergies in Years 1-2

- Eventually successful, but rocky start

Lesson: Developer tools and infrastructure products harder to integrate than application software

### 3. Talent Attrition in AI Acquisitions

**Problem**: Key AI talent leaves post-acquisition

Typical Pattern:

Month 1-6: 95%+ retention (honeymoon)

Month 7-12: 85% retention (vesting cliff)

Month 13-24: 70% retention (competition recruiting)

Month 25+: 50% retention (core team leaves)

Example: Google's AI Acqui-Hires

- Many acquired teams have 50%+ attrition by Year 3

- Researchers return to academia or start new companies

- Technology often survives, but momentum lost

Mitigation Strategies:

- 4-year vesting with 1-year cliff minimum

- Retention bonuses at 2 and 3 years

- Research freedom and publication rights

- Competitive compensation (refreshers)

- Interesting problems and resources

- Clear career paths

Best Practice:

Budget for 30-50% attrition and have replacement plan

## Best Practices

<div class="key-takeaways" style="margin: 2rem 0; padding: 1.5rem; background: linear-gradient(135deg, rgba(124, 58, 237, 0.1), rgba(99, 102, 241, 0.1)); border-left: 4px solid #7c3aed; border-radius: 8px;">

### The 10 Commandments of SaaS/AI M&A

1. **Validate Unit Economics**: CAC:LTV must work - growth alone is insufficient

2. **Cohort Analysis is King**: Understand customer retention by vintage, not just aggregate

3. **NRR > Logo Retention**: Dollar retention matters more than customer count

4. **Talent is the Asset**: In AI, pay for team quality - technology is secondary

5. **Integration Complexity**: Developer tools and infrastructure 2-3x harder than apps

6. **Cross-Sell Assumptions**: Validate cross-sell potential with customer interviews

7. **Platform Thinking**: Value how acquisition strengthens overall platform

8. **Retention Packages**: Golden handcuffs essential for AI talent and founders

9. **Speed to Value**: SaaS moves fast - slow integration = missed opportunity

10. **Rule of 40 Matters**: Growth + Profitability = Sustainable business model

</div>

## References

1. [SaaS Valuation Framework - SaaS Capital](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

2. [Bessemer Cloud Index - BVP](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

3. [AI M&A Trends - CB Insights](https://www.mckinsey.com/capabilities/mckinsey-digital/mckinsey-technology/overview/cybersecurity)

4. [Salesforce M&A Strategy - TechCrunch](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

5. [Vista Equity Playbook - Financial Times](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

6. [Adobe Figma Analysis - Stratechery](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

7. [Microsoft Nuance Deal - GeekWire](https://www.investmentbanking.deloitte.com/en/services/esop-corporate-finance/perspectives/tmt-update.html)

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Thu Jan 30 2025 19:00:00 GMT-0500 (Eastern Standard Time)