M&A Valuation Methods Overview

Valuation is one of the most critical aspects of M&A transactions. Determining the right price requires using multiple methodologies to triangulate a fair value range. This guide covers the primary valuation methods used in M&A.

Why Valuation Matters

Proper valuation serves several critical purposes:

- Price Discovery: Establishing a fair price range for negotiations

- Deal Justification: Supporting the investment thesis to stakeholders

- Risk Assessment: Understanding downside scenarios and sensitivities

- Financing: Determining appropriate debt capacity and returns

- Board Approval: Providing analytical basis for approval

Primary Valuation Methodologies

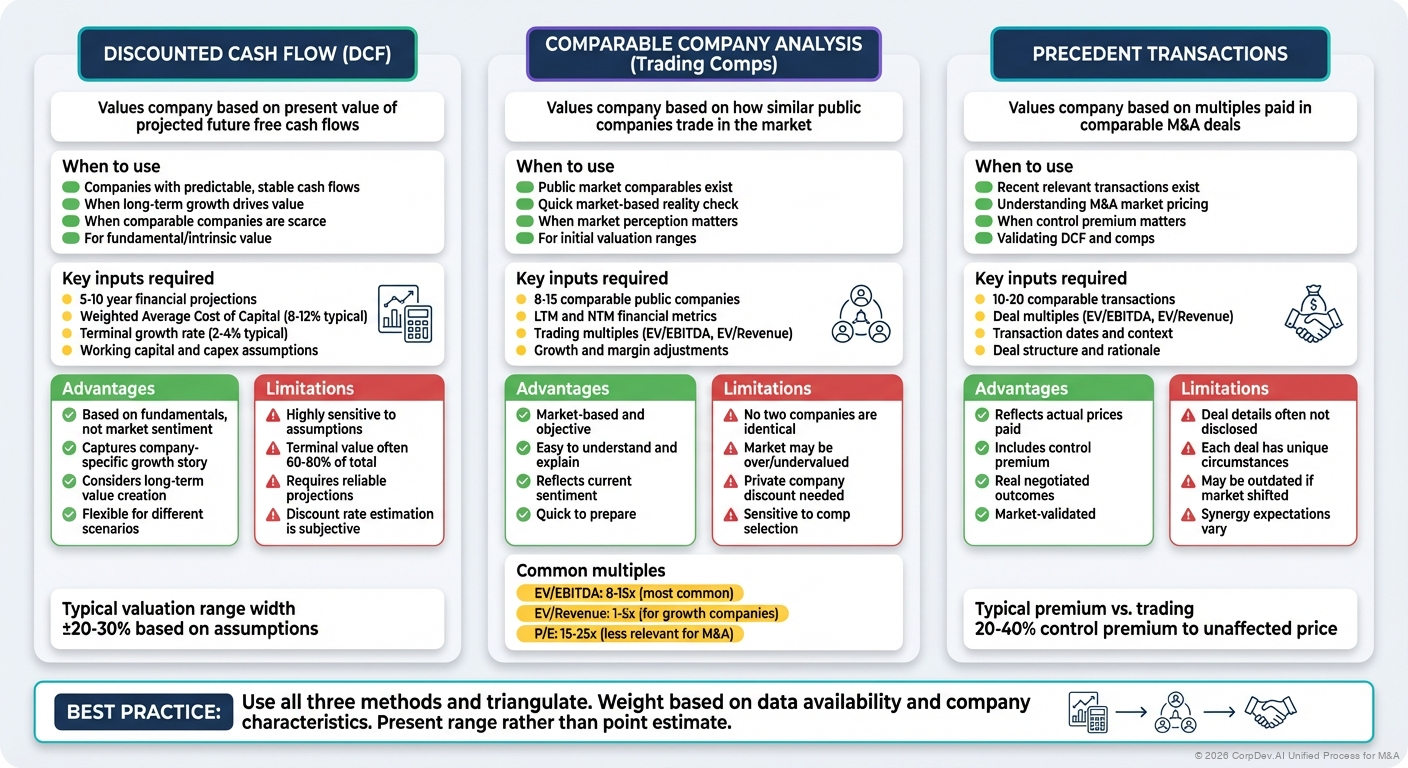

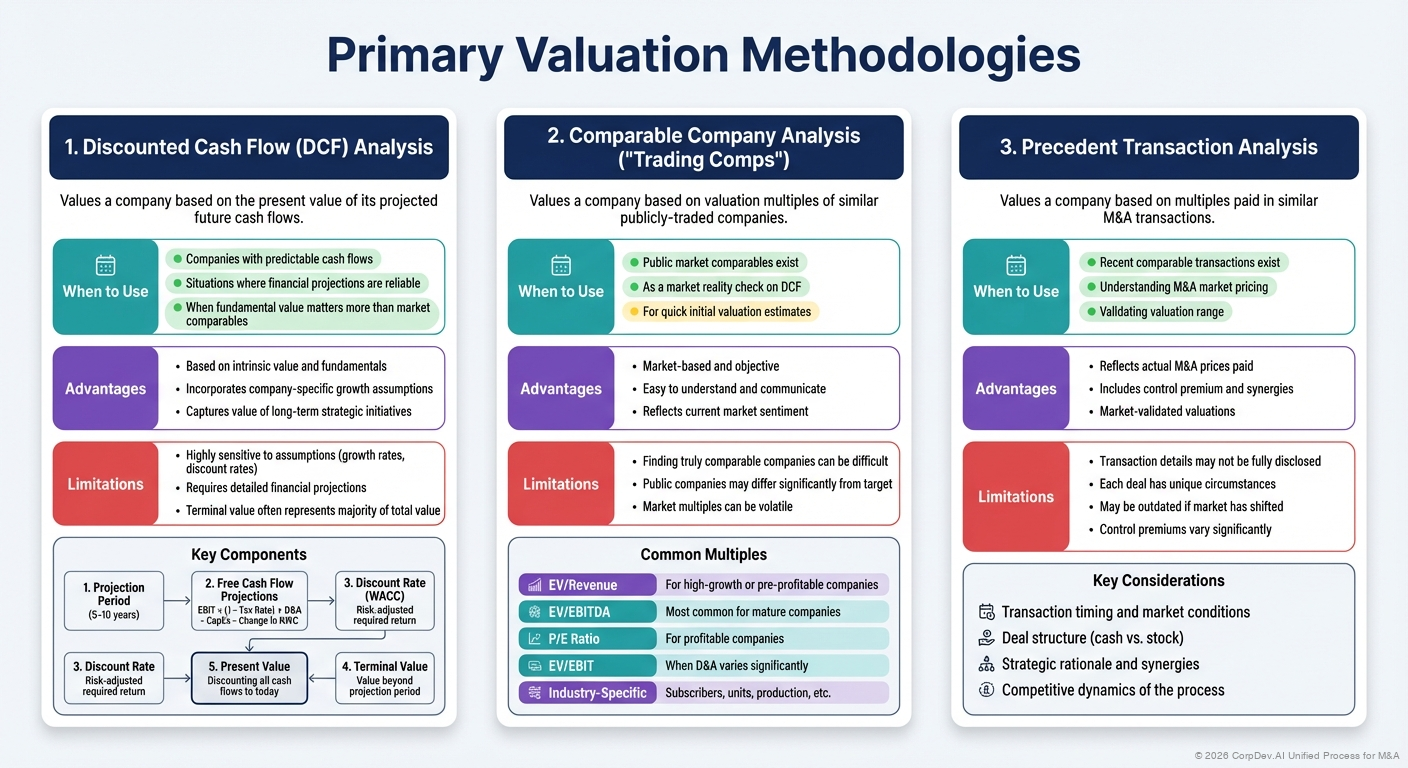

1. Discounted Cash Flow (DCF) Analysis

DCF analysis values a company based on the present value of its projected future cash flows.

When to Use:

- Companies with predictable cash flows

- Situations where financial projections are reliable

- When fundamental value matters more than market comparables

Advantages:

- Based on intrinsic value and fundamentals

- Incorporates company-specific growth assumptions

- Captures value of long-term strategic initiatives

Limitations:

- Highly sensitive to assumptions (growth rates, discount rates)

- Requires detailed financial projections

- Terminal value often represents majority of total value

Key Components:

- Projection Period: Typically 5-10 years

- Free Cash Flow Projections: EBIT × (1 - Tax Rate) + D&A - CapEx - Change in NWC

- Discount Rate (WACC): Risk-adjusted required return

- Terminal Value: Value beyond projection period

- Present Value: Discounting all cash flows to today

2. Comparable Company Analysis ("Trading Comps")

Values a company based on valuation multiples of similar publicly-traded companies.

When to Use:

- Public market comparables exist

- As a market reality check on DCF

- For quick initial valuation estimates

Advantages:

- Market-based and objective

- Easy to understand and communicate

- Reflects current market sentiment

Limitations:

- Finding truly comparable companies can be difficult

- Public companies may differ significantly from target

- Market multiples can be volatile

Common Multiples:

- EV/Revenue: For high-growth or pre-profitable companies

- EV/EBITDA: Most common for mature companies

- P/E Ratio: For profitable companies

- EV/EBIT: When D&A varies significantly

- Industry-Specific: Subscribers, units, production, etc.

3. Precedent Transaction Analysis

Values a company based on multiples paid in similar M&A transactions.

When to Use:

- Recent comparable transactions exist

- Understanding M&A market pricing

- Validating valuation range

Advantages:

- Reflects actual M&A prices paid

- Includes control premium and synergies

- Market-validated valuations

Limitations:

- Transaction details may not be fully disclosed

- Each deal has unique circumstances

- May be outdated if market has shifted

- Control premiums vary significantly

Key Considerations:

- Transaction timing and market conditions

- Deal structure (cash vs. stock)

- Strategic rationale and synergies

- Competitive dynamics of the process

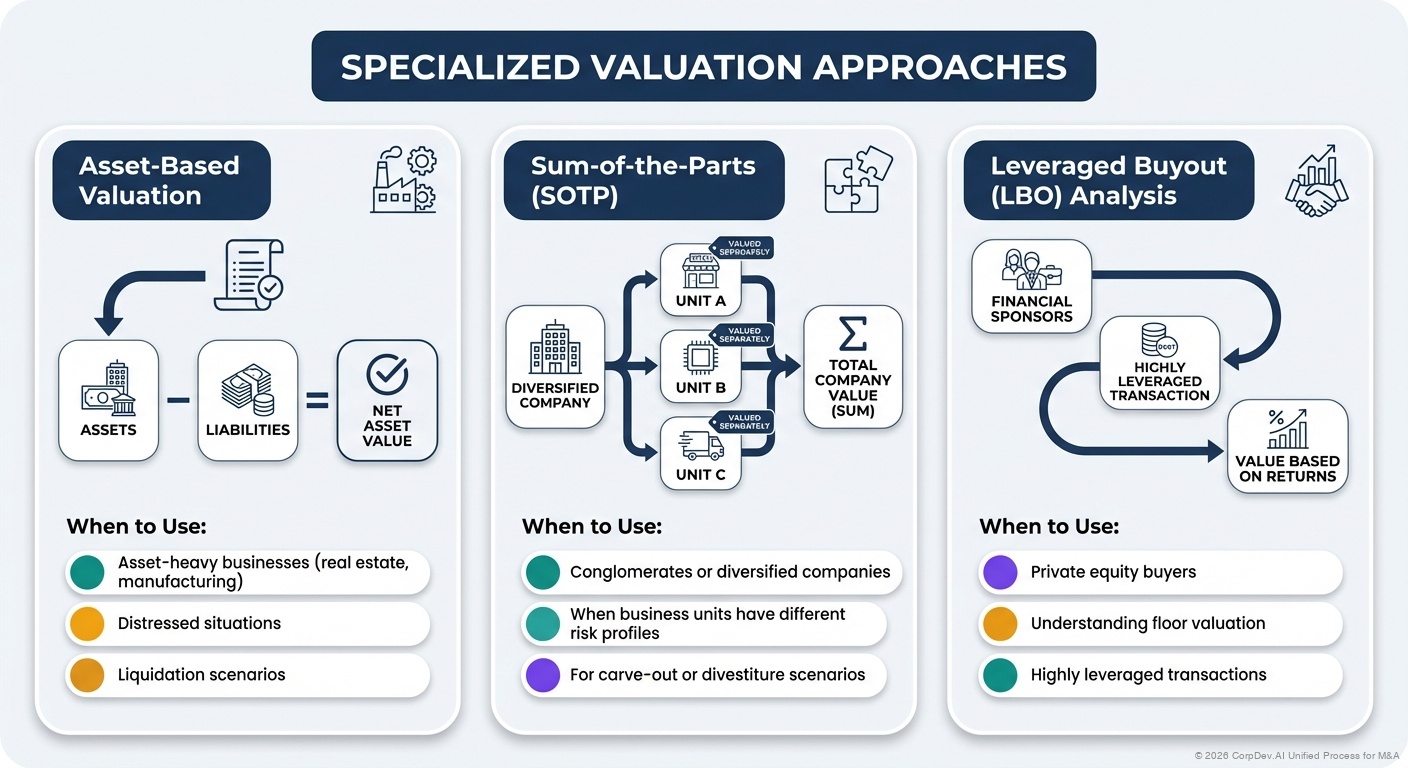

Specialized Valuation Approaches

Asset-Based Valuation

Values company based on net asset value (assets minus liabilities).

When to Use:

- Asset-heavy businesses (real estate, manufacturing)

- Distressed situations

- Liquidation scenarios

Sum-of-the-Parts (SOTP)

Values different business units separately and sums them.

When to Use:

- Conglomerates or diversified companies

- When business units have different risk profiles

- For carve-out or divestiture scenarios

Leveraged Buyout (LBO) Analysis

Determines value based on returns to financial sponsors.

When to Use:

- Private equity buyers

- Understanding floor valuation

- Highly leveraged transactions

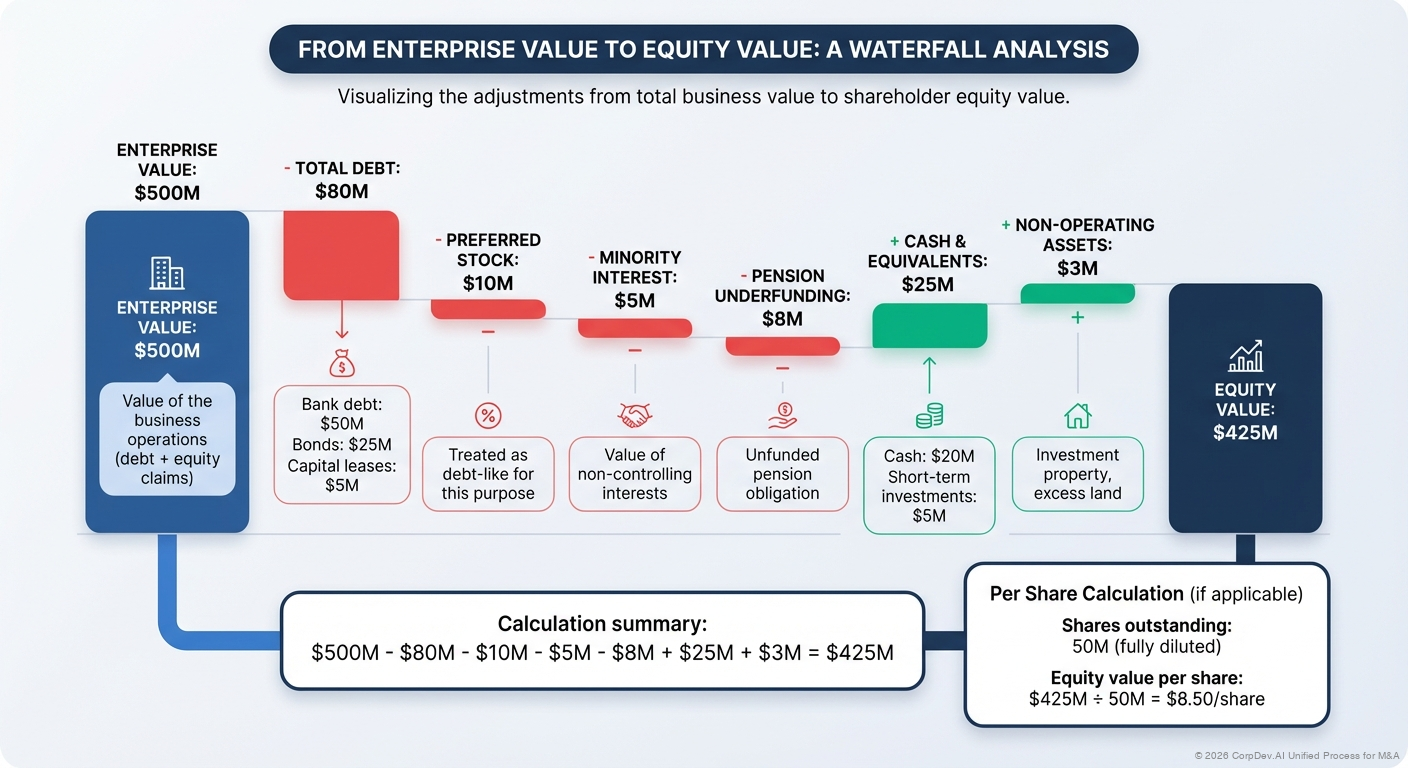

Valuation Adjustments

Several adjustments may be necessary to reach enterprise value and equity value:

From Equity Value to Enterprise Value

Enterprise Value = Equity Value + Debt + Preferred Stock + Minority Interest - Cash

Common Adjustments

- Excess Cash: Cash beyond operational requirements

- Non-Operating Assets: Real estate, investments

- Non-Recurring Items: One-time charges or gains

- Management Add-backs: Owner compensation normalization

- Run-Rate Adjustments: Recent initiatives not yet in financials

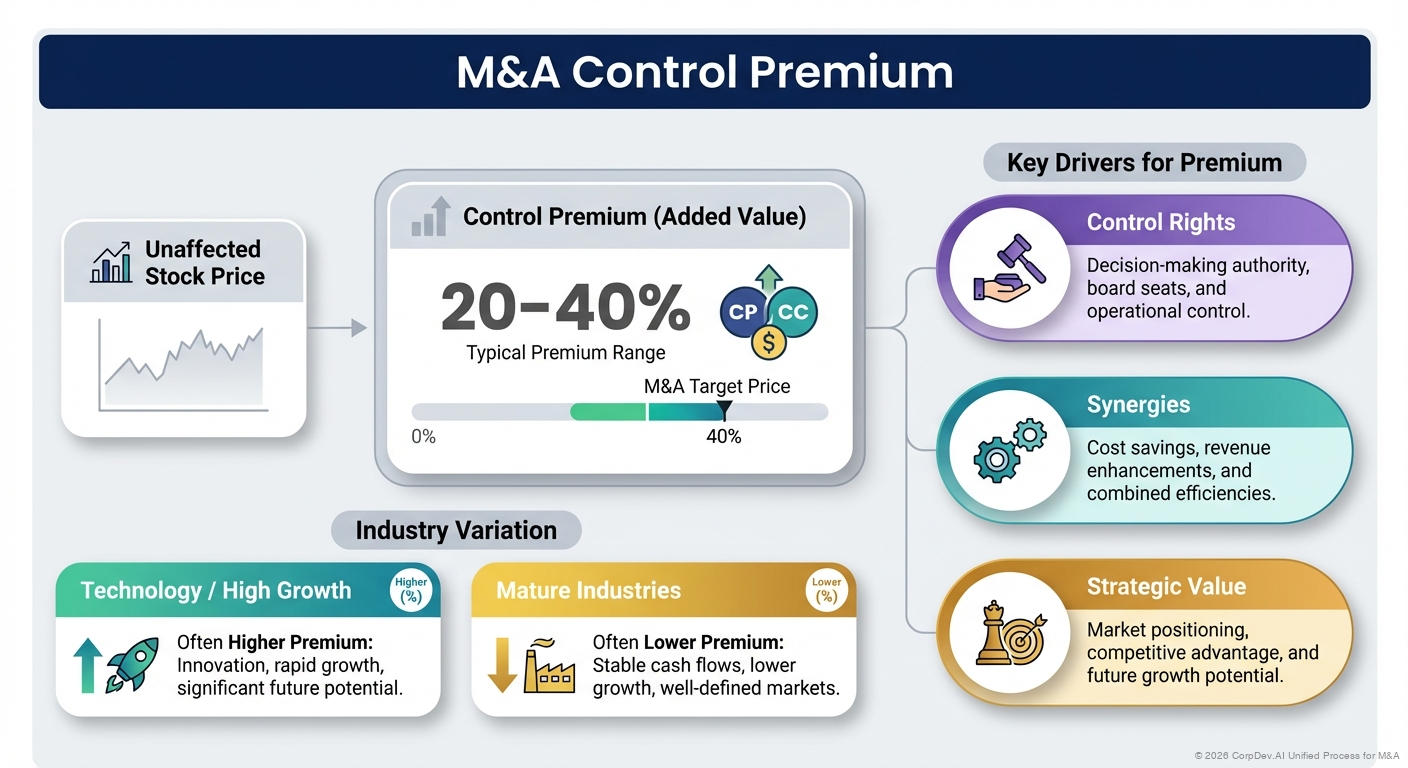

Control Premium

M&A transactions typically include a premium over public market prices:

- Typical Range: 20-40% premium to unaffected stock price

- Drivers: Control rights, synergies, strategic value

- Industry Variation: Technology often higher, mature industries lower

Synergies and Their Impact on Valuation

Synergies can significantly impact valuation:

Revenue Synergies

- Cross-selling opportunities

- Expanded market reach

- Enhanced product offerings

Cost Synergies

- Elimination of duplicate functions

- Economies of scale

- Process improvements

- Procurement savings

Typical Approach:

- Identify and quantify specific synergies

- Apply probability weighting

- Discount to present value

- Determine how much to pay for synergies (typically 50-75%)

Putting It All Together

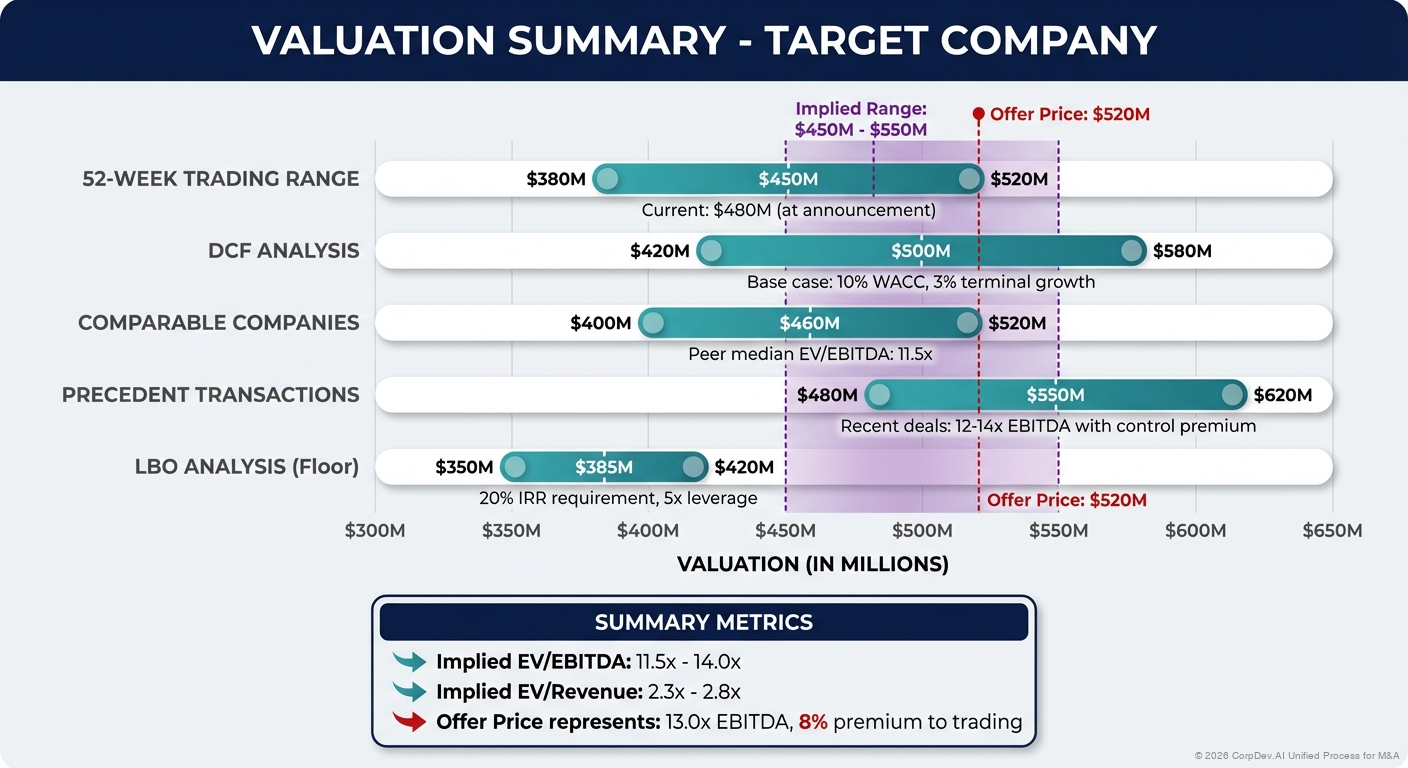

Best practice is to use multiple methodologies and triangulate a value range:

- Build DCF Model: Establishes intrinsic value

- Analyze Comparable Companies: Provides market context

- Review Precedent Transactions: Shows M&A pricing

- Consider Special Factors: Synergies, strategic value, competitive dynamics

- Establish Range: Typically 15-25% range from low to high

- Determine Walk-Away Price: Maximum price regardless of competition

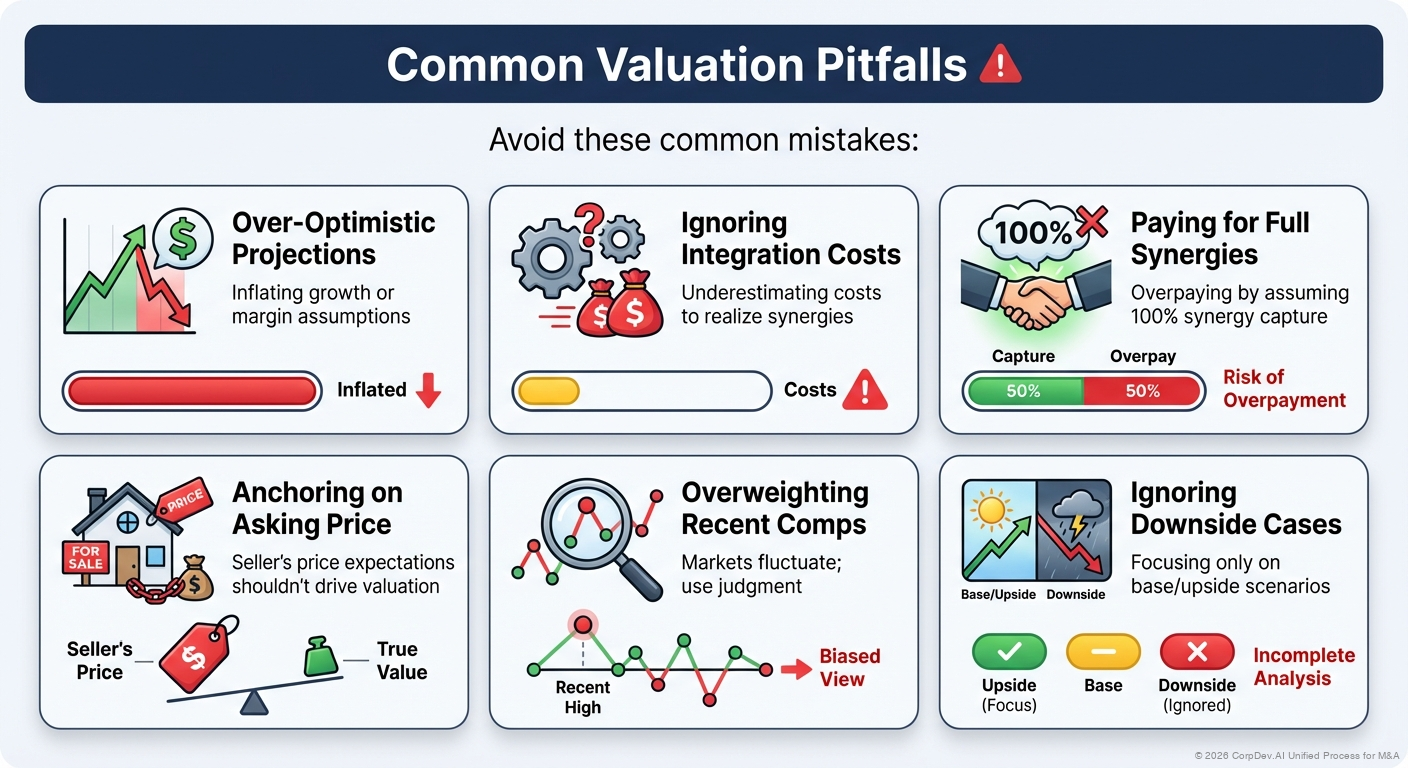

Common Valuation Pitfalls

Avoid these common mistakes:

- Over-Optimistic Projections: Inflating growth or margin assumptions

- Ignoring Integration Costs: Underestimating costs to realize synergies

- Paying for Full Synergies: Overpaying by assuming 100% synergy capture

- Anchoring on Asking Price: Seller's price expectations shouldn't drive valuation

- Overweighting Recent Comps: Markets fluctuate; use judgment

- Ignoring Downside Cases: Focusing only on base/upside scenarios

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)