M&A Negotiation Strategies

Negotiation is a critical skill in M&A, influencing not just the purchase price but also deal structure, risk allocation, and ultimate transaction success. This guide covers proven strategies for negotiating M&A deals effectively.

Principles of M&A Negotiation

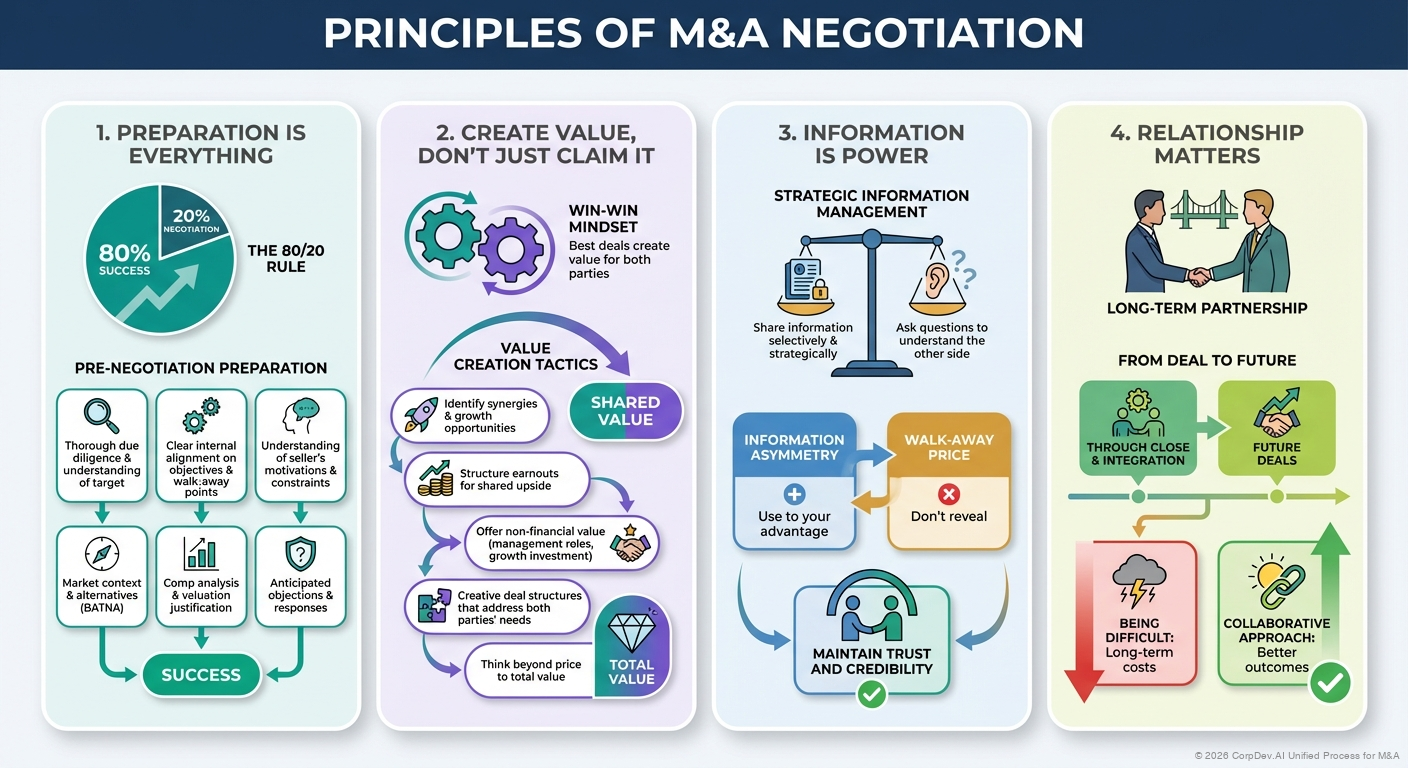

1. Preparation is Everything

The 80/20 Rule: 80% of negotiation success comes from preparation

Pre-Negotiation Preparation:

- Thorough due diligence and understanding of target

- Clear internal alignment on objectives and walk-away points

- Understanding of seller's motivations and constraints

- Market context and alternatives (BATNA - Best Alternative to Negotiated Agreement)

- Comp analysis and valuation justification

- Anticipated objections and responses

2. Create Value, Don't Just Claim It

Win-Win Mindset: Best deals create value for both parties

Value Creation Tactics:

- Identify synergies and growth opportunities

- Structure earnouts for shared upside

- Offer non-financial value (management roles, growth investment)

- Creative deal structures that address both parties' needs

- Think beyond price to total value

3. Information is Power

Strategic Information Management:

- Share information selectively and strategically

- Ask questions to understand the other side

- Don't reveal your walk-away price

- Use information asymmetry to your advantage

- But maintain trust and credibility

4. Relationship Matters

Long-Term Partnership:

- You'll work together through close and integration

- Reputation matters for future deals

- Being difficult has long-term costs

- Collaborative approach yields better outcomes

Buyer Negotiation Strategies

Price Negotiation

Anchor Low (But Credibly):

- First offer sets the anchor

- Make it low but defensible with data

- Use comparable transactions and valuation multiples

- Be prepared to justify with detailed analysis

Use Ranges Strategically:

- Propose range rather than point estimate

- Seller will gravitate to high end

- Your range's low end is your real target

Create Downward Price Pressure:

- Emphasize risks uncovered in diligence

- Highlight integration challenges and costs

- Reference market comp multiples

- Point to required investment needs

- Show alternative uses of capital

Example Approach:

Initial LOI: $40-45M (your target is $42M)

Due Diligence: Identify $3M of issues

Revised Offer: $39-42M

Final: Settle at $41M (below your initial target)

Structural Negotiation

Shift Risk to Seller:

- Asset purchase vs. stock purchase

- Earnouts tied to performance

- Escrow and holdbacks for indemnification

- Seller financing for skin in the game

- Caps and baskets on representations

Use Time Value of Money:

- Deferred consideration vs. cash at close

- Earnouts paid over time

- Retention bonuses vs. purchase price

- Seller note vs. bank financing

Alternative Consideration:

- Stock vs. cash (share risk and upside)

- Consulting agreements (ordinary income vs. cap gains for seller)

- Employment agreements (retention and tax efficiency)

Leverage Competitive Dynamics

In Exclusive Situations:

- Use time pressure (exclusivity expiring)

- Emphasize opportunity cost of delay

- Highlight certainty of close vs. restarting process

In Competitive Situations:

- Demonstrate strategic value beyond price

- Emphasize speed and certainty of execution

- Highlight cultural fit and growth plans

- De-risk with committed financing

Key Employee Retention

Negotiate Strategically:

- Separate employee comp from purchase price

- Structure as retention bonuses vs. purchase price

- Vest over time to ensure retention

- Use non-competes and clawbacks

Create Alignment:

- Equity rollovers for key employees

- Earnouts tied to their performance

- Clear growth path and autonomy

Due Diligence as Negotiation Tool

Use Findings to Re-Trade:

- Material findings justify price reduction

- Customer concentration warrants earnout

- Technology debt requires investment adjustment

- Legal issues need escrow or indemnification

But Don't Over-Use:

- Re-trading destroys trust

- Use sparingly for material issues only

- Maintain credibility for future deals

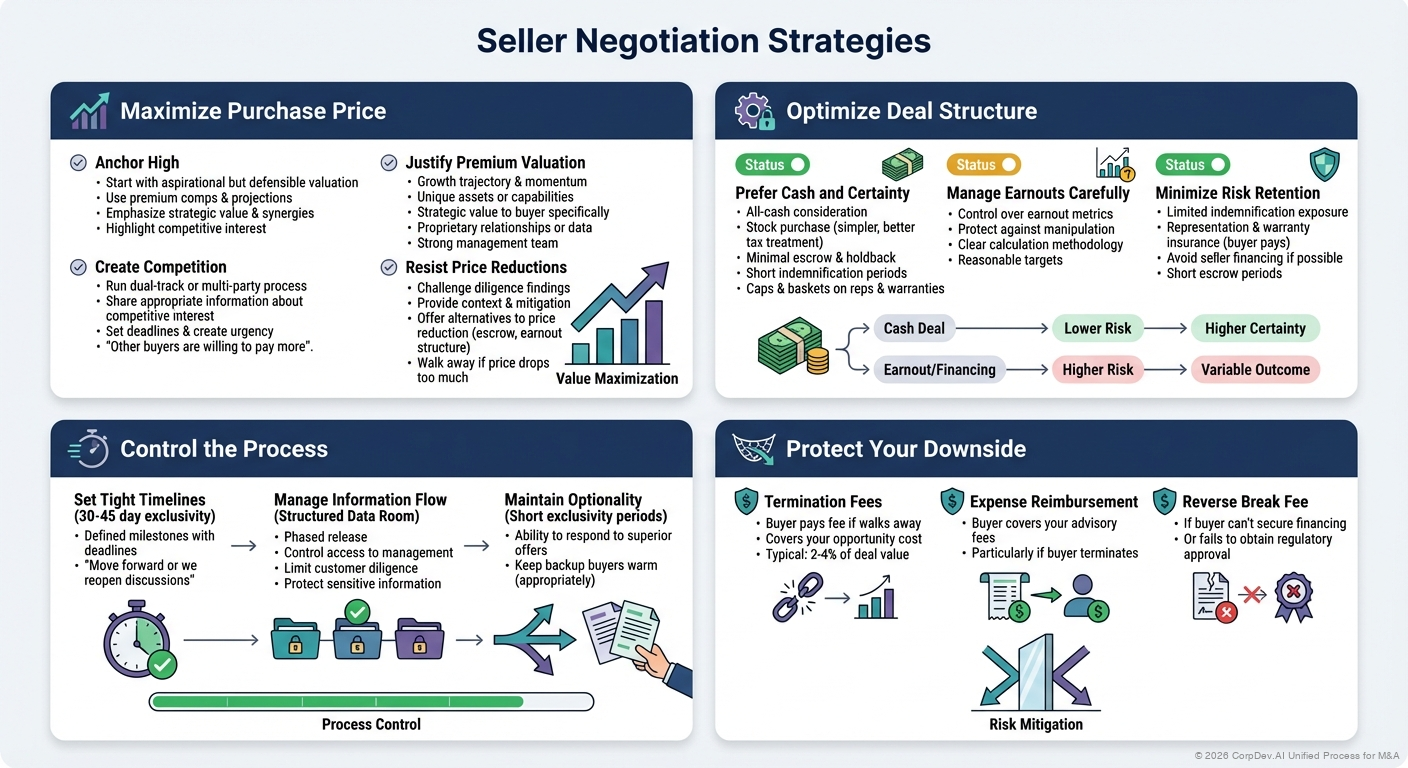

Seller Negotiation Strategies

Maximize Purchase Price

Anchor High:

- Start with aspirational but defensible valuation

- Use premium comps and projections

- Emphasize strategic value and synergies

- Highlight competitive interest

Create Competition:

- Run dual-track or multi-party process

- Share (appropriate) information about competitive interest

- Set deadlines and create urgency

- "Other buyers are willing to pay more"

Justify Premium Valuation:

- Growth trajectory and momentum

- Unique assets or capabilities

- Strategic value to buyer specifically

- Proprietary relationships or data

- Strong management team

Resist Price Reductions:

- Challenge diligence findings

- Provide context and mitigation

- Offer alternatives to price reduction (escrow, earnout structure)

- Walk away if price drops too much

Optimize Deal Structure

Prefer Cash and Certainty:

- All-cash consideration

- Stock purchase (simpler, better tax treatment)

- Minimal escrow and holdback

- Short indemnification periods

- Caps and baskets on reps and warranties

Manage Earnouts Carefully:

- Control over earnout metrics

- Protect against manipulation

- Clear calculation methodology

- Reasonable targets

Minimize Risk Retention:

- Limited indemnification exposure

- Representation & warranty insurance (buyer pays)

- Avoid seller financing if possible

- Short escrow periods

Control the Process

Set Tight Timelines:

- 30-45 day exclusivity

- Defined milestones with deadlines

- "Move forward or we reopen discussions"

Manage Information Flow:

- Structured data room with phased release

- Control access to management

- Limit customer diligence

- Protect sensitive information

Maintain Optionality:

- Short exclusivity periods

- Ability to respond to superior offers

- Keep backup buyers warm (appropriately)

Protect Your Downside

Termination Fees:

- Buyer pays fee if walks away

- Covers your opportunity cost

- Typical: 2-4% of deal value

Expense Reimbursement:

- Buyer covers your advisory fees

- Particularly if buyer terminates

Reverse Break Fee:

- If buyer can't secure financing

- Or fails to obtain regulatory approval

Key Negotiation Points

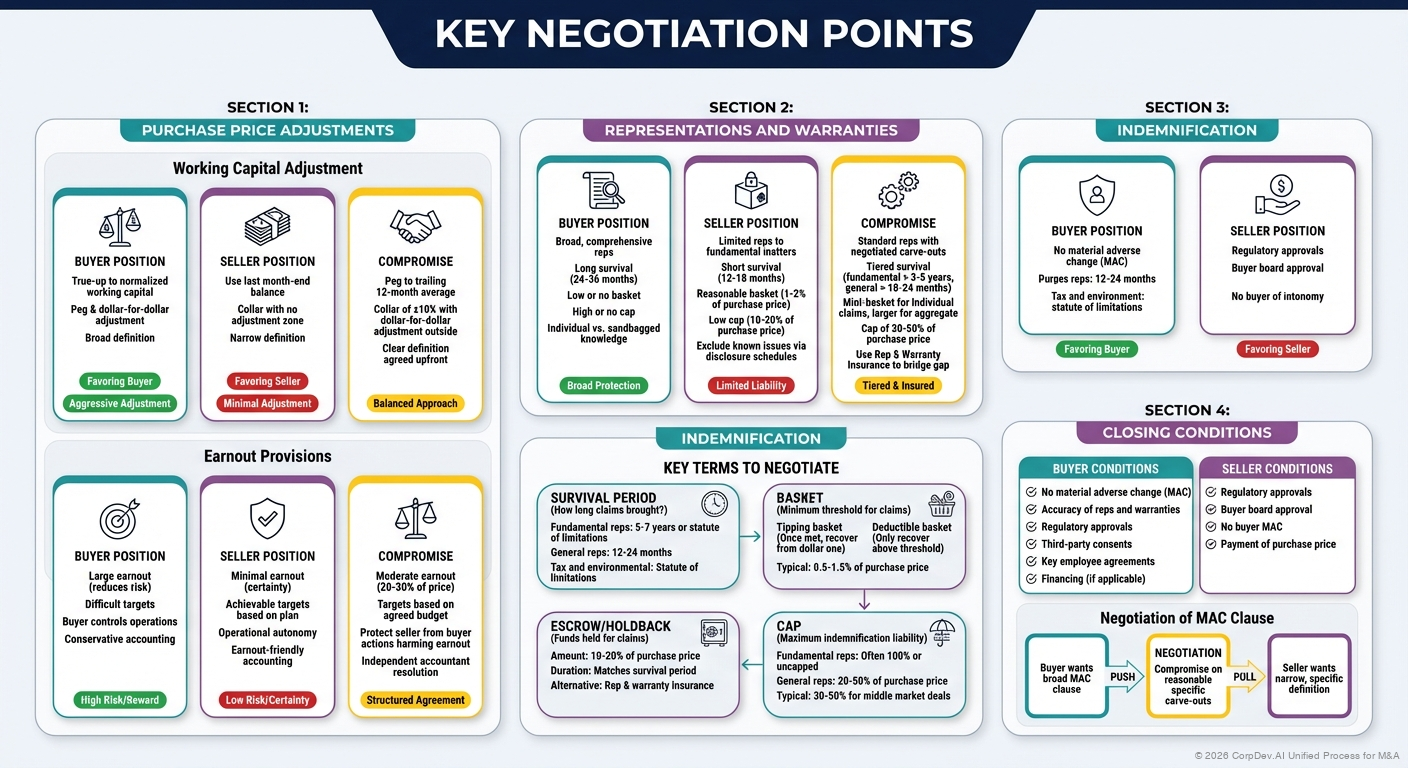

Purchase Price Adjustments

Working Capital Adjustment:

Buyer Position:

- True-up to normalized working capital

- Peg and dollar-for-dollar adjustment

- Broad definition of working capital

Seller Position:

- Use last month-end balance

- Collar with no adjustment zone

- Narrow definition

Compromise:

- Peg to trailing 12-month average

- Collar of ±10% with dollar-for-dollar adjustment outside

- Clear definition agreed upfront

Earnout Provisions:

Buyer Position:

- Large earnout (reduces risk)

- Difficult targets

- Buyer controls operations

- Conservative accounting

Seller Position:

- Minimal earnout (certainty)

- Achievable targets based on plan

- Operational autonomy

- Earnout-friendly accounting

Compromise:

- Moderate earnout (20-30% of price)

- Targets based on agreed budget

- Protect seller from buyer actions harming earnout

- Independent accountant resolution of disputes

Representations and Warranties

Buyer Position:

- Broad, comprehensive reps

- Long survival periods (24-36 months)

- Low or no basket

- High or no cap

- Individual vs. sandbagged knowledge

Seller Position:

- Limited reps to fundamental matters

- Short survival (12-18 months)

- Reasonable basket (1-2% of purchase price)

- Low cap (10-20% of purchase price)

- Exclude known issues via disclosure schedules

Compromise:

- Standard reps with negotiated carve-outs

- Tiered survival (fundamental = 3-5 years, general = 18-24 months)

- Mini-basket for individual claims, larger for aggregate

- Cap of 30-50% of purchase price

- Use Rep & Warranty Insurance to bridge gap

Indemnification

Key Terms to Negotiate:

Survival Period: How long can claims be brought?

- Fundamental reps: 5-7 years or statute of limitations

- General reps: 12-24 months

- Tax and environmental: Statute of limitations

Basket: Minimum threshold for claims

- Tipping basket: Once threshold met, recover from dollar one

- Deductible basket: Only recover amounts above threshold

- Typical: 0.5-1.5% of purchase price

Cap: Maximum indemnification liability

- Fundamental reps: Often 100% of purchase price or uncapped

- General reps: 20-50% of purchase price

- Typical: 30-50% for middle market deals

Escrow/Holdback: Funds held for indemnification claims

- Amount: 10-20% of purchase price

- Duration: Matches survival period

- Alternative: Rep & warranty insurance

Closing Conditions

Buyer Conditions:

- No material adverse change (MAC)

- Accuracy of reps and warranties

- Regulatory approvals

- Third-party consents

- Key employee agreements

- Financing (if applicable)

Seller Conditions:

- Regulatory approvals

- Buyer board approval

- No buyer MAC

- Payment of purchase price

Negotiation:

- Buyer wants broad MAC clause

- Seller wants narrow, specific definition

- Compromise on reasonable specific carve-outs

Tactical Negotiation Techniques

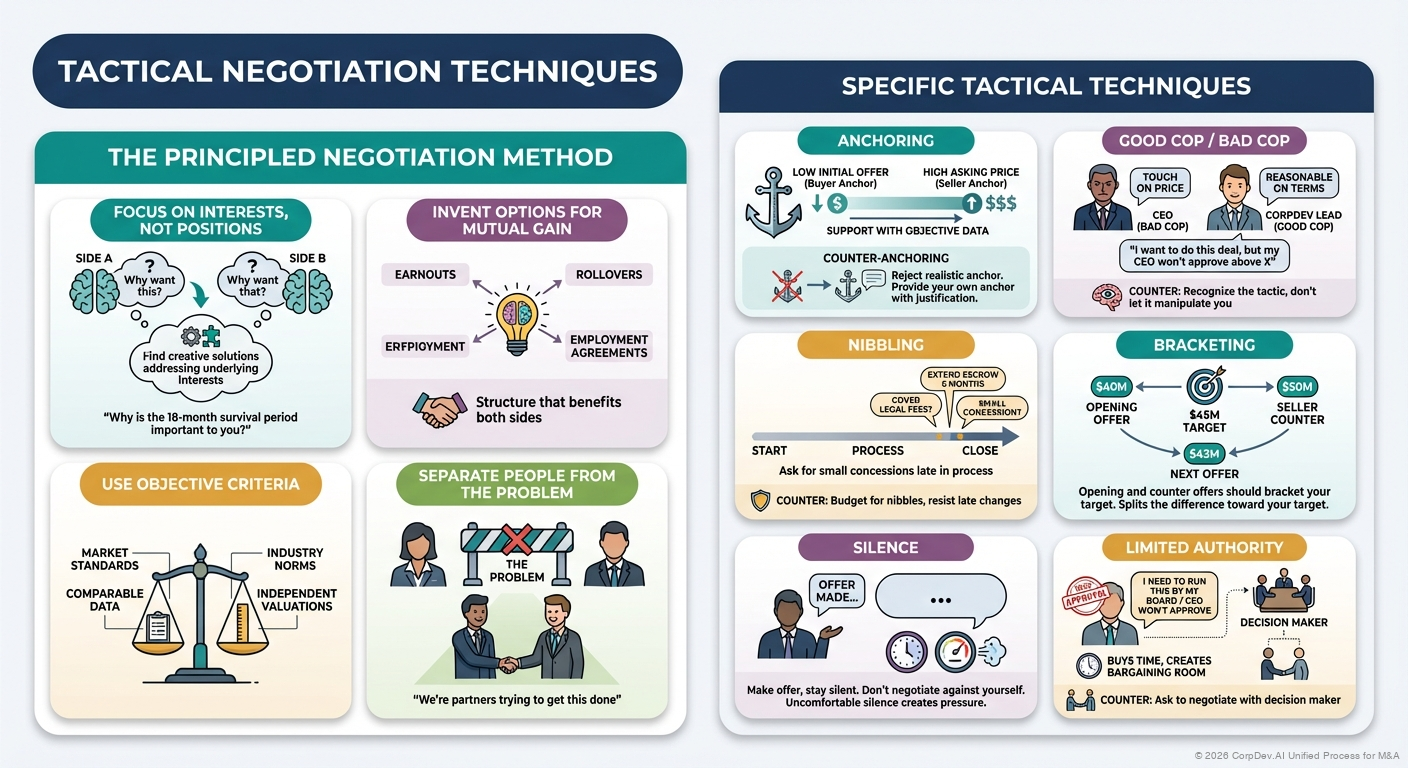

The Principled Negotiation Method

Focus on Interests, Not Positions:

- Understand why each side wants what they want

- Find creative solutions that address underlying interests

- "Why is the 18-month survival period important to you?"

Invent Options for Mutual Gain:

- Brainstorm creative solutions

- Earnouts, rollovers, employment agreements

- Structure that benefits both sides

Use Objective Criteria:

- Market standards and benchmarks

- Comparable transaction data

- Industry norms

- Independent valuations

Separate People from the Problem:

- Attack the problem, not the person

- Build working relationship

- "We're partners trying to get this done"

Anchoring

Concept: First number sets the anchor for negotiation

Application:

- Buyer: Anchor low with initial offer

- Seller: Anchor high with asking price

- Support anchor with objective data

- Don't make first move feel insulting

Counter-Anchoring:

- Reject anchor as unrealistic

- Provide your own anchor with justification

- Refocus on objective criteria

Good Cop / Bad Cop

Setup: One negotiator is tough, another is reasonable

Application:

- CEO plays bad cop on price

- CorpDev lead plays good cop on terms

- "I want to do this deal, but my CEO won't approve above X"

Counter: Recognize the tactic, don't let it manipulate you

Nibbling

Concept: Ask for small concessions late in process

Application:

- "We're agreed on everything except can you cover our legal fees?"

- "Just need you to extend the escrow period by 6 months"

- Leverage momentum and desire to close

Counter: Budget for nibbles, resist late changes

Bracketing

Concept: Your opening and counter offers should bracket your target

Example:

Your target: $45M

Opening offer: $40M

If seller counters at $50M, your next offer: $43M

(Splits the difference toward your target)

Silence

Power of Silence:

- Make offer, then stay silent

- Don't negotiate against yourself

- Force other side to respond

- Uncomfortable silence creates pressure

Limited Authority

Technique: Claim you need approval from higher authority

Application:

- "I need to run this by my board"

- "My CEO won't approve above this price"

- Buys time and creates bargaining room

Counter: Ask to negotiate with decision maker

Managing Difficult Negotiations

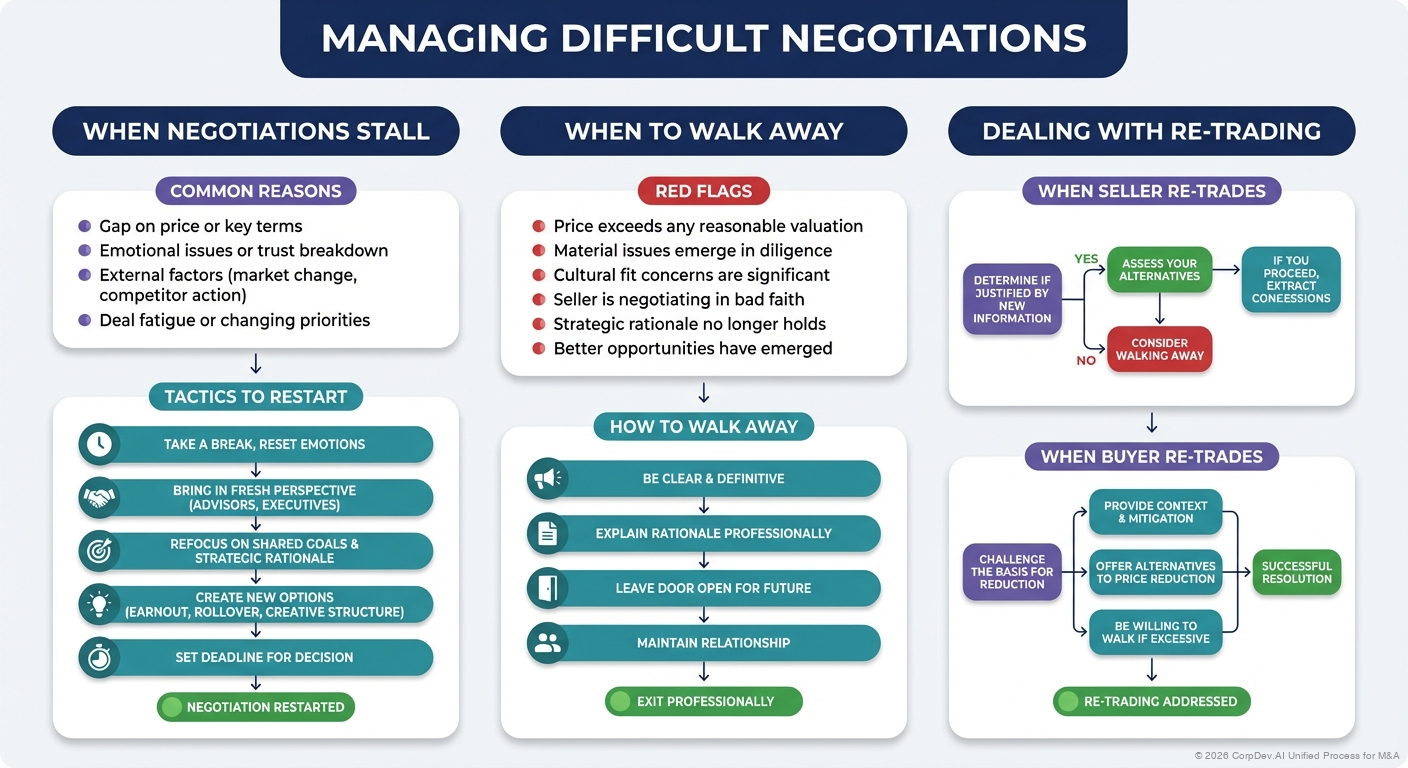

When Negotiations Stall

Common Reasons:

- Gap on price or key terms

- Emotional issues or trust breakdown

- External factors (market change, competitor action)

- Deal fatigue or changing priorities

Tactics to Restart:

- Take a break, reset emotions

- Bring in fresh perspective (advisors, executives)

- Refocus on shared goals and strategic rationale

- Create new options (earnout, rollover, creative structure)

- Set deadline for decision

When to Walk Away

Red Flags:

- Price exceeds any reasonable valuation

- Material issues emerge in diligence

- Cultural fit concerns are significant

- Seller is negotiating in bad faith

- Strategic rationale no longer holds

- Better opportunities have emerged

How to Walk Away:

- Be clear and definitive

- Explain rationale professionally

- Leave door open for future

- Maintain relationship

Dealing with Re-Trading

When Seller Re-Trades:

- Determine if justified by new information

- Assess your alternatives

- Consider walking away

- If you proceed, extract concessions

When Buyer Re-Trades:

- Challenge the basis for reduction

- Provide context and mitigation

- Offer alternatives to price reduction

- Be willing to walk if excessive

Cultural Considerations

Private Equity Sellers

Characteristics:

- Professional, process-driven

- Multiple parties involved (fund, management, advisors)

- Focus on price maximization

- Less emotional attachment

Strategies:

- Emphasize certainty and speed

- Demonstrate financing capability

- Professional, efficient process

- Focus on price and terms, less on vision

Founder/Owner Sellers

Characteristics:

- Emotional attachment to business

- Concerned about legacy and employees

- May be first-time sellers

- Looking for right partner, not just price

Strategies:

- Emphasize shared values and vision

- Highlight employee retention plans

- Respect their legacy

- Build personal relationship

- Balance price with intangibles

Corporate Sellers (Divestitures)

Characteristics:

- Multiple stakeholders and approval layers

- Regulatory and compliance complexity

- May include stranded costs or TSAs

- Less emotional, more process-oriented

Strategies:

- Understand corporate approval process

- Address transition services needs

- Navigate complexity patiently

- Build support across organization

Common Negotiation Mistakes

1. Falling in Love with the Deal

Problem: Losing objectivity, willing to overpay

Solution: Maintain discipline, stick to walk-away price

2. Negotiating Against Yourself

Problem: Making concessions without getting anything back

Solution: Every give requires a get

3. Ignoring Relationship

Problem: Winning negotiation but losing partnership

Solution: Balance firmness with respect and collaboration

4. Poor Preparation

Problem: Walking into negotiation without clear strategy

Solution: Invest time in preparation and planning

5. Revealing Your Hand

Problem: Disclosing walk-away price or timeline pressure

Solution: Strategic information management

6. Letting Ego Drive Decisions

Problem: Personal pride overrides business judgment

Solution: Stay focused on business rationale and value

7. Death by a Thousand Cuts

Problem: Conceding too many small points

Solution: Track all concessions, push back on nibbles

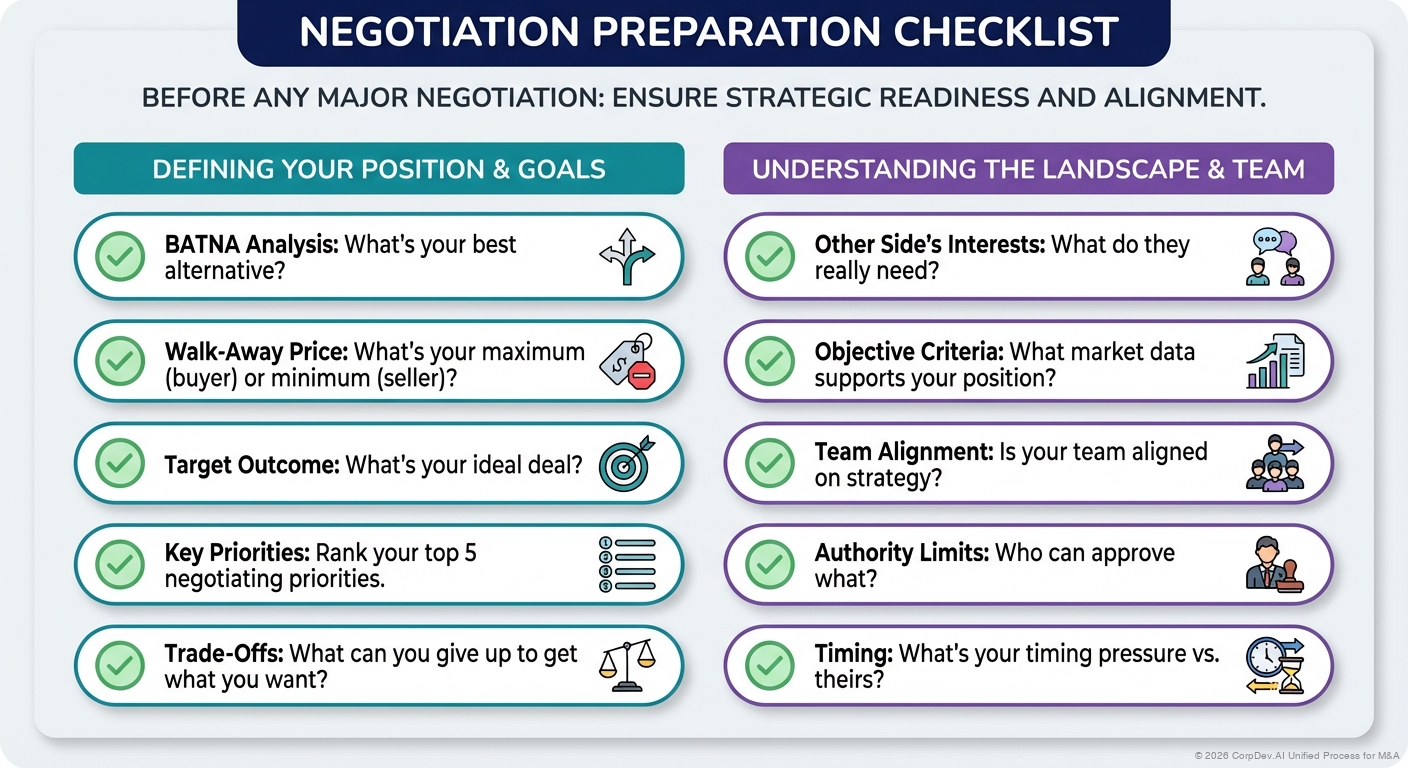

Negotiation Preparation Checklist

Before Any Major Negotiation:

- BATNA Analysis: What's your best alternative?

- Walk-Away Price: What's your maximum (buyer) or minimum (seller)?

- Target Outcome: What's your ideal deal?

- Key Priorities: Rank your top 5 negotiating priorities

- Trade-Offs: What can you give up to get what you want?

- Other Side's Interests: What do they really need?

- Objective Criteria: What market data supports your position?

- Team Alignment: Is your team aligned on strategy?

- Authority Limits: Who can approve what?

- Timing: What's your timing pressure vs. theirs?

Best Practices

For Buyers

- Know Your Walk-Away Price: And stick to it

- Create Competition: Or the perception of alternatives

- Use Diligence Strategically: But don't over-rely on re-trading

- Structure Creatively: Find win-win solutions

- Build Relationship: You'll be partners post-close

- Move with Urgency: Don't drag out unnecessarily

- Maintain Credibility: Your reputation matters

For Sellers

- Create Competitive Tension: Multiple buyers improve outcomes

- Know Your Number: Don't accept less than your walk-away

- Control the Process: Set timelines and milestones

- Justify Your Price: With data and strategic value

- Protect Your Downside: Termination fees and expense coverage

- Be Willing to Walk: Your best leverage

For Both Parties

- Prepare Thoroughly: 80% of success is preparation

- Focus on Interests: Not just positions

- Create Value: Don't just divide the pie

- Maintain Professionalism: Even when frustrated

- Use Advisors Wisely: But don't hide behind them

- Document Everything: Written confirmation of agreements

- Think Long-Term: Relationship matters beyond close

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)