Letter of Intent & Term Sheet

The Letter of Intent (LOI) or Term Sheet is a critical milestone that bridges preliminary discussions and formal due diligence. Getting the LOI right sets the foundation for a successful transaction.

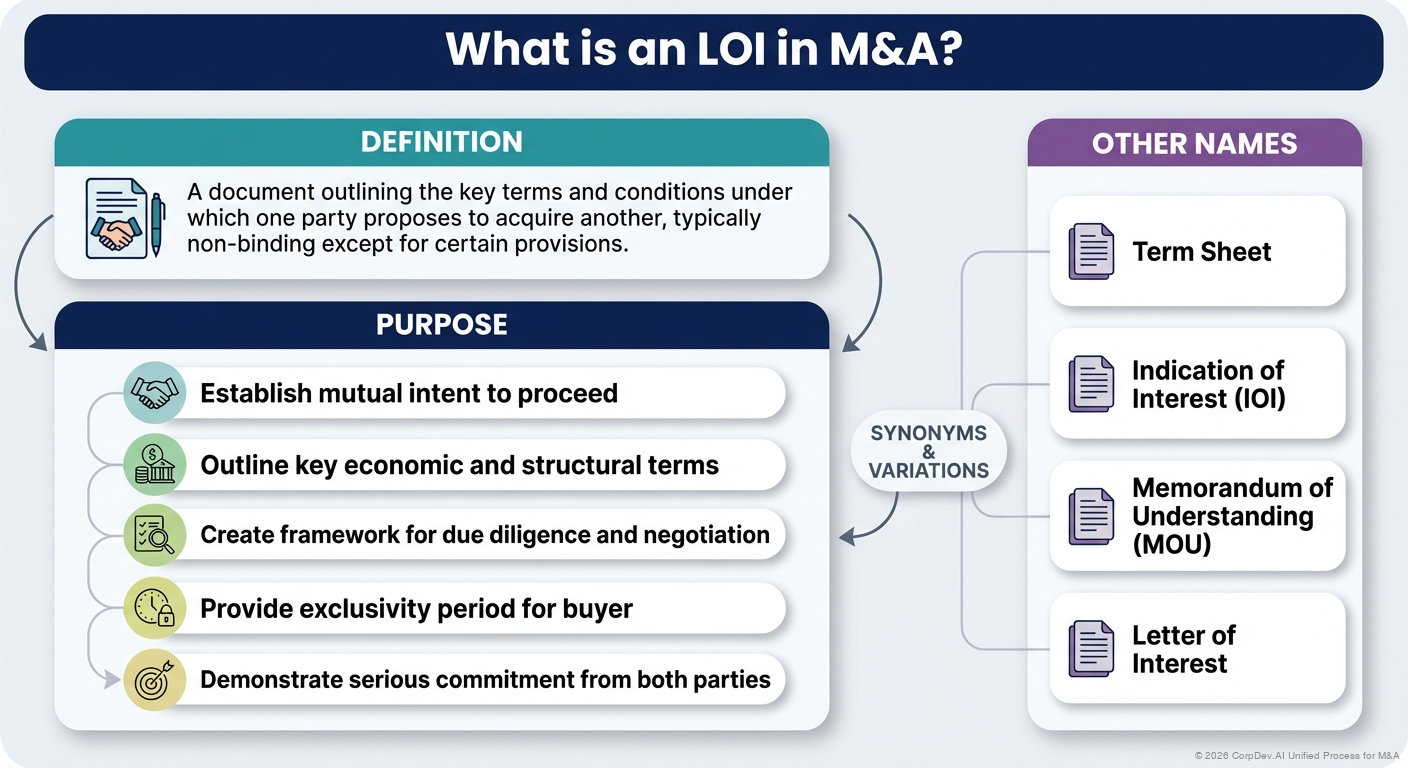

What is an LOI?

Definition: A document outlining the key terms and conditions under which one party proposes to acquire another, typically non-binding except for certain provisions.

Purpose:

- Establish mutual intent to proceed

- Outline key economic and structural terms

- Create framework for due diligence and negotiation

- Provide exclusivity period for buyer

- Demonstrate serious commitment from both parties

Other Names:

- Term Sheet

- Indication of Interest (IOI)

- Memorandum of Understanding (MOU)

- Letter of Interest

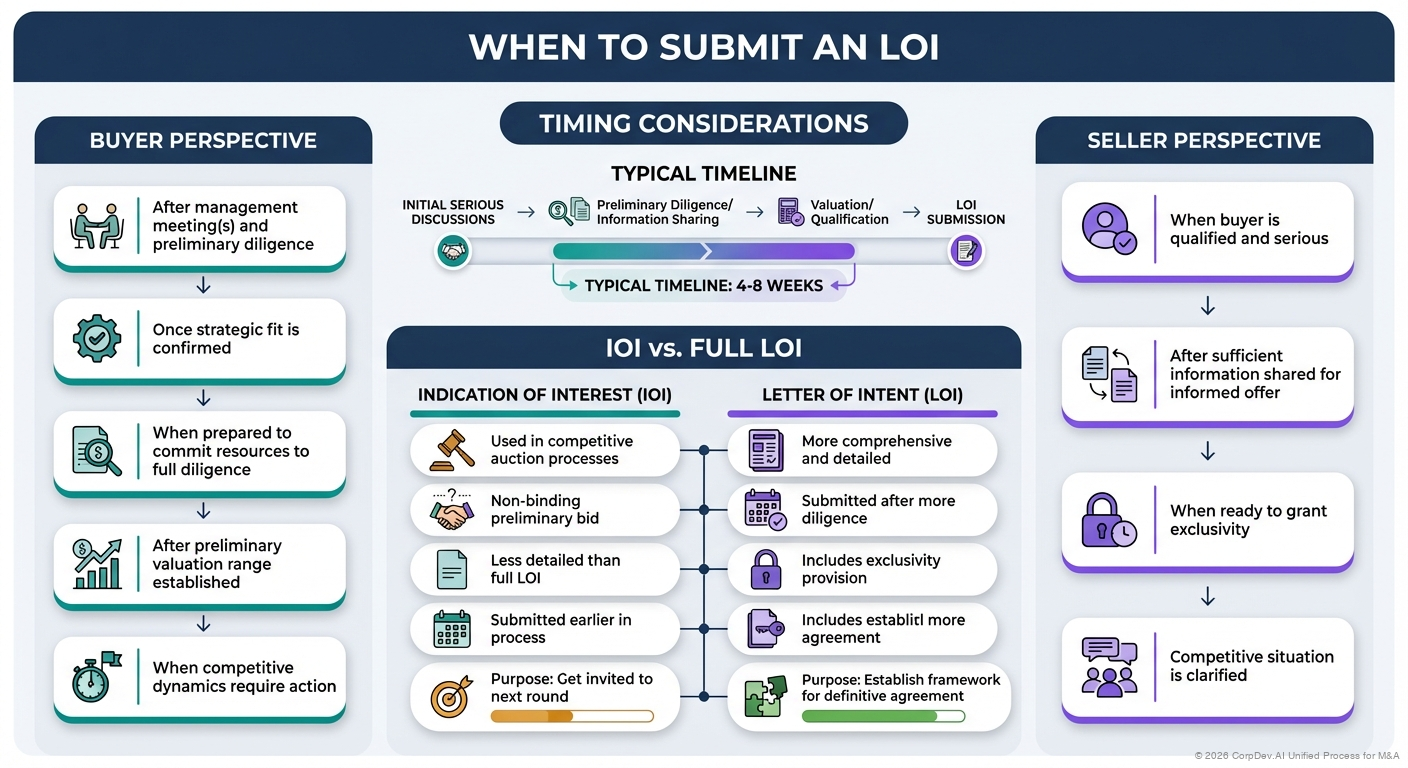

When to Submit an LOI

Timing Considerations

Buyer Perspective:

- After management meeting(s) and preliminary diligence

- Once strategic fit is confirmed

- When prepared to commit resources to full diligence

- After preliminary valuation range established

- When competitive dynamics require action

Typical Timeline: 4-8 weeks after initial serious discussions

Seller Perspective:

- When buyer is qualified and serious

- After sufficient information shared for informed offer

- When ready to grant exclusivity

- Competitive situation is clarified

IOI vs. Full LOI

Indication of Interest (IOI):

- Used in competitive auction processes

- Non-binding preliminary bid

- Less detailed than full LOI

- Submitted earlier in process

- Purpose: Get invited to next round

Letter of Intent (LOI):

- More comprehensive and detailed

- Submitted after more diligence

- Includes exclusivity provision

- Purpose: Establish framework for definitive agreement

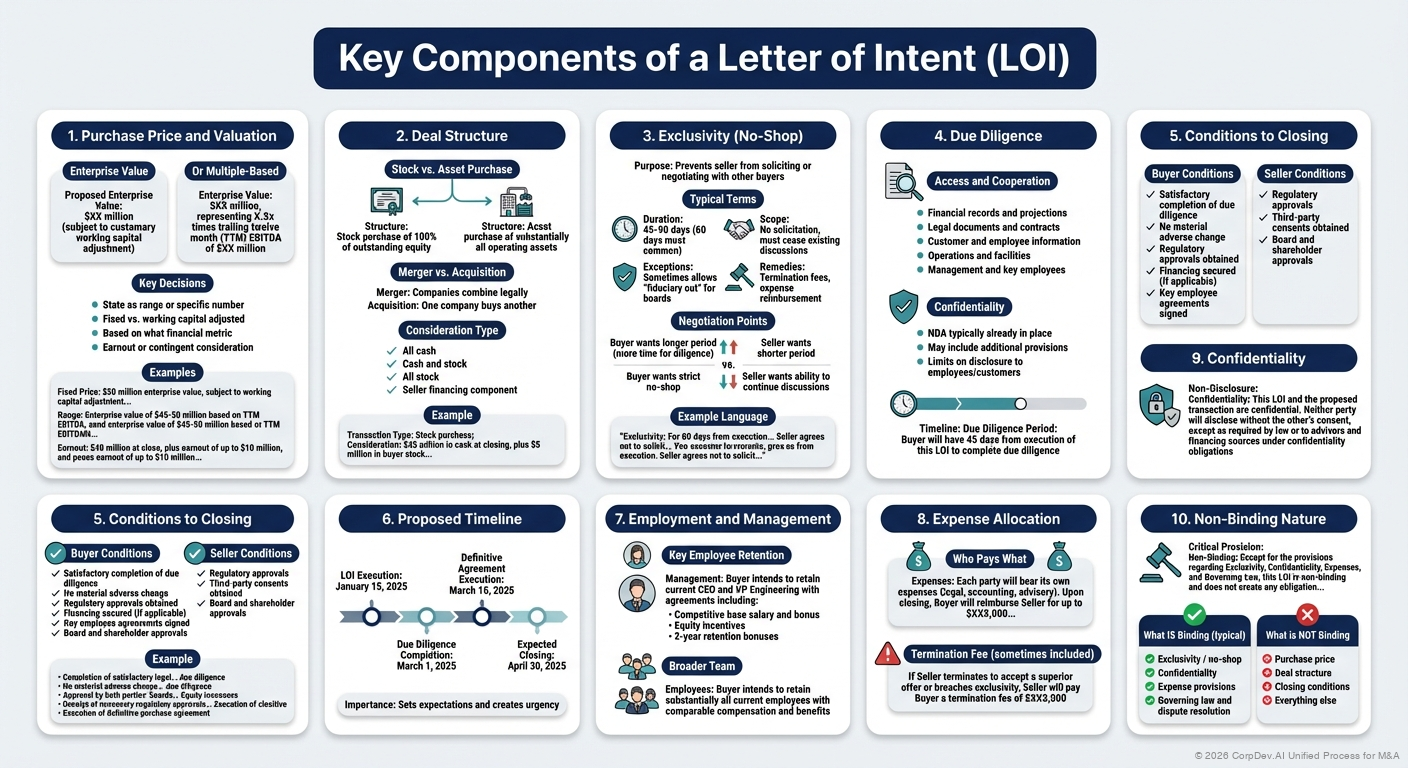

Key Components of an LOI

1. Purchase Price and Valuation

Enterprise Value:

Proposed Enterprise Value: $XX million

(subject to customary working capital adjustment)

Or Multiple-Based:

Enterprise Value: $XX million, representing X.Xx times

trailing twelve month (TTM) EBITDA of $XX million

Key Decisions:

- State as range or specific number

- Fixed vs. working capital adjusted

- Based on what financial metric

- Earnout or contingent consideration

Examples:

Fixed Price:

$50 million enterprise value, subject to working capital

adjustment with target of $5 million

Range:

Enterprise value of $45-50 million based on trailing twelve

month EBITDA of $10-11 million, representing 4.5x multiple

Earnout:

$40 million at close, plus earnout of up to $10 million based

on achievement of 2025-2026 revenue milestones

2. Deal Structure

Stock vs. Asset Purchase:

Structure: Stock purchase of 100% of outstanding equity

OR

Structure: Asset purchase of substantially all operating assets

Merger vs. Acquisition:

- Merger: Companies combine legally

- Acquisition: One company buys another

Consideration Type:

- All cash

- Cash and stock

- All stock

- Seller financing component

Example:

Transaction Type: Stock purchase

Consideration: $45 million in cash at closing, plus $5 million

in buyer stock (subject to market adjustment)

3. Exclusivity (No-Shop)

Purpose: Prevents seller from soliciting or negotiating with other buyers

Typical Terms:

- Duration: 45-90 days (60 days most common)

- Scope: No solicitation, must cease existing discussions

- Exceptions: Sometimes allows "fiduciary out" for boards

- Remedies: Termination fees, expense reimbursement

Example Language:

Exclusivity: For 60 days from execution of this LOI, Seller agrees

not to solicit, initiate, or continue discussions with any other

party regarding a sale, merger, or similar transaction. Seller will

immediately cease all existing discussions with other parties.

Negotiation Points:

- Buyer wants longer period (more time for diligence)

- Seller wants shorter period (less time off market)

- Buyer wants strict no-shop (prevents auction)

- Seller wants ability to continue discussions (maintains leverage)

4. Due Diligence

Access and Cooperation:

Due Diligence: Seller will provide Buyer full access to:

- Financial records and projections

- Legal documents and contracts

- Customer and employee information

- Operations and facilities

- Management and key employees

Confidentiality:

- NDA typically already in place

- May include additional provisions

- Limits on disclosure to employees/customers

Timeline:

Due Diligence Period: Buyer will have 45 days from execution

of this LOI to complete due diligence

5. Conditions to Closing

Buyer Conditions:

- Satisfactory completion of due diligence

- No material adverse change

- Regulatory approvals obtained

- Financing secured (if applicable)

- Key employee agreements signed

- Board and shareholder approvals

Seller Conditions:

- Regulatory approvals

- Third-party consents obtained

- Board and shareholder approvals

Example:

Conditions to Closing:

- Completion of satisfactory legal, financial, and operational

due diligence

- No material adverse change in business

- Approval by both parties' boards and shareholders

- Receipt of necessary regulatory approvals (HSR, etc.)

- Execution of definitive purchase agreement

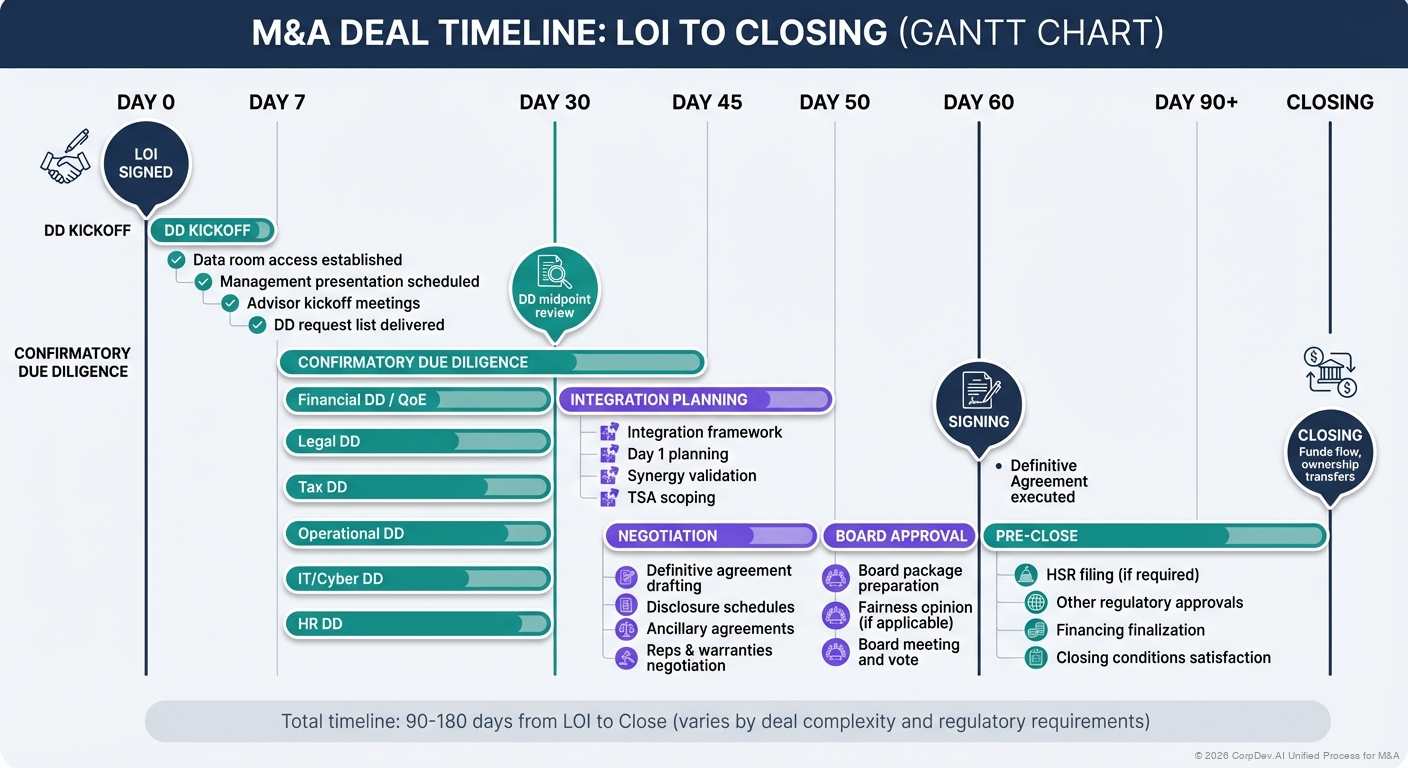

6. Proposed Timeline

Milestones:

Proposed Timeline:

- LOI Execution: January 15, 2025

- Due Diligence Completion: March 1, 2025

- Definitive Agreement Execution: March 15, 2025

- Expected Closing: April 30, 2025

Importance: Sets expectations and creates urgency

7. Employment and Management

Key Employee Retention:

Management: Buyer intends to retain current CEO and VP Engineering

with employment agreements including:

- Competitive base salary and bonus

- Equity incentives

- 2-year retention bonuses

Broader Team:

Employees: Buyer intends to retain substantially all current

employees with comparable compensation and benefits

8. Expense Allocation

Who Pays What:

Expenses: Each party will bear its own expenses (legal, accounting,

advisory). Upon closing, Buyer will reimburse Seller for up to

$XXX,000 of reasonable transaction expenses.

Termination Fee (sometimes included):

If Seller terminates to accept a superior offer or breaches

exclusivity, Seller will pay Buyer a termination fee of $XXX,000

9. Confidentiality

Non-Disclosure:

Confidentiality: This LOI and the proposed transaction are

confidential. Neither party will disclose without the other's

consent, except as required by law or to advisors and financing

sources under confidentiality obligations

10. Non-Binding Nature

Critical Provision:

Non-Binding: Except for the provisions regarding Exclusivity,

Confidentiality, Expenses, and Governing Law, this LOI is

non-binding and does not create any obligation to complete

the proposed transaction

What IS Binding (typical):

- Exclusivity / no-shop

- Confidentiality

- Expense provisions

- Governing law and dispute resolution

What is NOT Binding:

- Purchase price

- Deal structure

- Closing conditions

- Everything else

LOI Negotiation Strategies

Buyer Strategies

1. Manage Expectations with Ranges

- Propose valuation range rather than fixed price

- Allows room for adjustment post-diligence

- "Enterprise value of $45-50M subject to completion of diligence"

2. Build in Adjustment Mechanisms

- Working capital adjustment

- Earnout provisions

- Holdback or escrow

3. Secure Strong Exclusivity

- 60-90 day period

- Strict no-shop language

- Termination fee if broken

4. Preserve Flexibility

- Broad due diligence rights

- Material adverse change provision

- Condition on board approval

5. Position for Partnership

- Emphasize cultural fit

- Highlight growth plans for business

- Stress employee retention commitment

Seller Strategies

1. Create Competition

- Submit IOI vs. LOI to maintain flexibility

- Shorter exclusivity periods (30-45 days)

- Limited scope of no-shop

2. Maximize Price Certainty

- Push for specific price, not range

- Limit adjustment mechanisms

- Minimize conditions and outs

3. Protect Downside

- Termination fee for buyer

- Expense reimbursement

- Ability to restart process if buyer walks

4. Accelerate Timeline

- Shorter due diligence period

- Aggressive closing timeline

- Create urgency

5. Ensure Employee Treatment

- Specific commitments on retention

- Comp and benefits protection

- Management role clarity

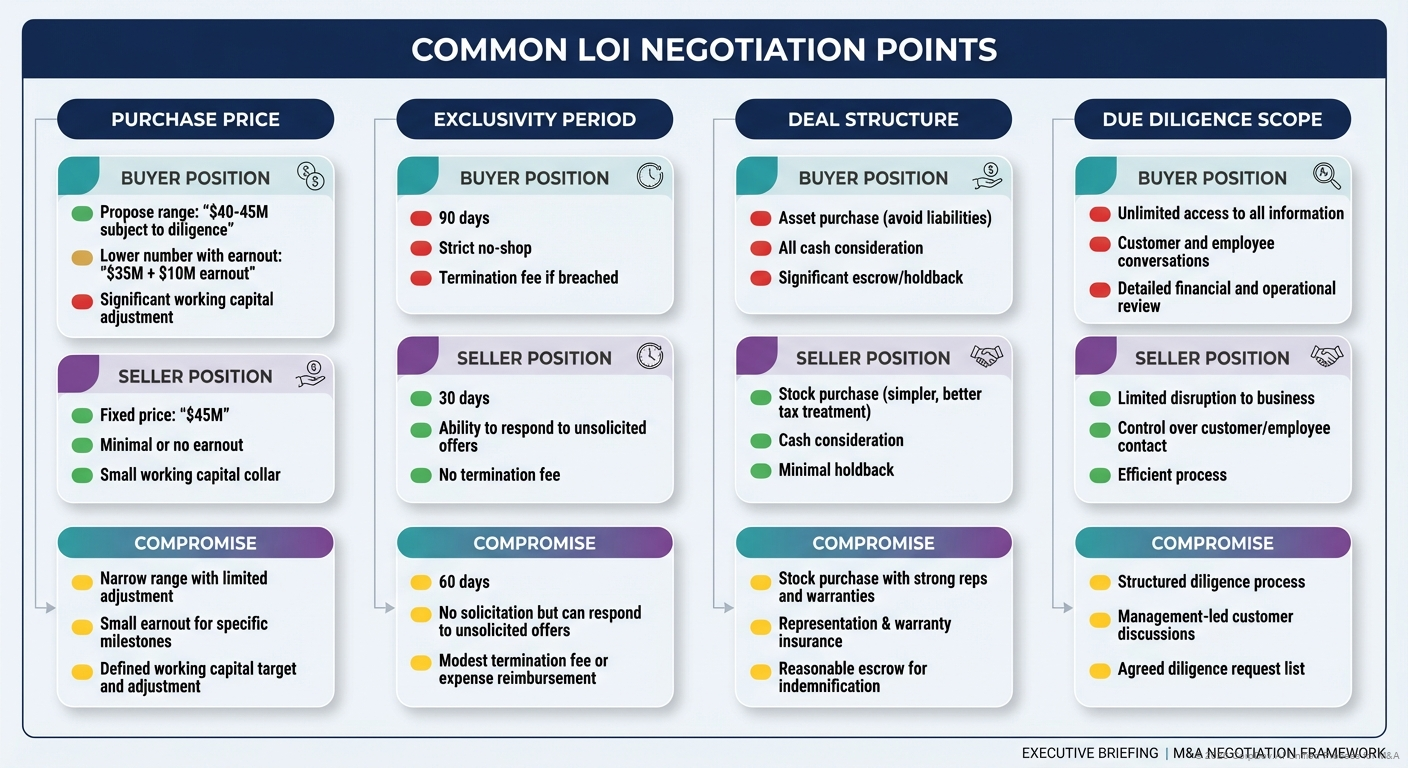

Common LOI Negotiation Points

Purchase Price

Buyer Position:

- Propose range: "$40-45M subject to diligence"

- Lower number with earnout: "$35M + $10M earnout"

- Significant working capital adjustment

Seller Position:

- Fixed price: "$45M"

- Minimal or no earnout

- Small working capital collar

Compromise:

- Narrow range with limited adjustment

- Small earnout for specific milestones

- Defined working capital target and adjustment

Exclusivity Period

Buyer Position:

- 90 days

- Strict no-shop

- Termination fee if breached

Seller Position:

- 30 days

- Ability to respond to unsolicited offers

- No termination fee

Compromise:

- 60 days

- No solicitation but can respond to unsolicited offers

- Modest termination fee or expense reimbursement

Deal Structure

Buyer Position:

- Asset purchase (avoid liabilities)

- All cash consideration

- Significant escrow/holdback

Seller Position:

- Stock purchase (simpler, better tax treatment)

- Cash consideration

- Minimal holdback

Compromise:

- Stock purchase with strong reps and warranties

- Representation & warranty insurance

- Reasonable escrow for indemnification

Due Diligence Scope

Buyer Position:

- Unlimited access to all information

- Customer and employee conversations

- Detailed financial and operational review

Seller Position:

- Limited disruption to business

- Control over customer/employee contact

- Efficient process

Compromise:

- Structured diligence process

- Management-led customer discussions

- Agreed diligence request list

Sample LOI Outline

LETTER OF INTENT

Date: January 15, 2025

To: [Seller Company Name]

From: [Buyer Company Name]

Re: Proposed Acquisition

Dear [Seller Representative]:

This letter outlines the principal terms upon which [Buyer]

("Buyer") would be willing to acquire [Seller] ("Seller" or

"Company"):

1. TRANSACTION STRUCTURE

- Stock purchase of 100% of outstanding equity

- All cash transaction

2. PURCHASE PRICE

- Enterprise Value: $45-50 million

- Subject to customary working capital adjustment

- Based on TTM EBITDA of $10-11 million (4.5x multiple)

3. EXCLUSIVITY

- 60-day period from execution

- Seller will not solicit or engage with other buyers

- Immediate cessation of existing discussions

4. DUE DILIGENCE

- 45-day diligence period

- Full access to records, management, facilities

- Buyer to conduct at own expense

5. TIMELINE

- LOI Execution: January 15

- Diligence Complete: March 1

- Definitive Agreement: March 15

- Expected Closing: April 30

6. CONDITIONS

- Satisfactory completion of due diligence

- No material adverse change

- Regulatory approvals

- Definitive documentation

- Board and shareholder approvals

7. EMPLOYEES

- Retain substantially all employees

- Employment agreements for CEO and CTO

- Comparable compensation and benefits

8. CONFIDENTIALITY

- Terms of this LOI and transaction are confidential

- Disclosure only as legally required or to advisors

9. EXPENSES

- Each party bears own expenses

- Upon closing, Buyer reimburses up to $100K of

Seller's transaction expenses

10. NON-BINDING

- This LOI is non-binding except for sections 3

(Exclusivity), 8 (Confidentiality), 9 (Expenses),

and 11 (Governing Law)

11. GOVERNING LAW

- Governed by laws of [State]

Please indicate your acceptance by signing below.

Sincerely,

[Buyer Signature]

[Name, Title]

ACCEPTED AND AGREED:

[Seller Signature]

[Name, Title]

[Date]

After LOI Execution

Buyer Next Steps

Immediate (Week 1):

- Assemble due diligence team

- Prepare detailed diligence request list

- Schedule management presentations

- Access virtual data room

- Engage legal counsel for definitive agreement

Ongoing (Weeks 2-6):

- Execute comprehensive due diligence

- Regular updates to senior management

- Build detailed financial model

- Refine valuation

- Identify integration priorities

Final (Weeks 7-8):

- Complete diligence reports

- Make go/no-go decision

- Finalize valuation and negotiate price adjustments

- Move to definitive agreement negotiation

Seller Next Steps

Immediate (Week 1):

- Prepare and organize data room

- Brief management team on process and confidentiality

- Engage legal counsel

- Plan for business continuity during diligence

Ongoing (Weeks 2-6):

- Respond to diligence requests

- Conduct management presentations

- Maintain business operations

- Address buyer questions and concerns

Final (Weeks 7-8):

- Negotiate any price adjustments

- Review definitive agreement drafts

- Prepare for board and shareholder approvals

Common LOI Mistakes

1. Too Vague or Too Specific

Problem: Either lacks critical terms or locks in details prematurely

Solution: Hit the right level of detail—key terms without overcommitting

2. Unrealistic Timeline

Problem: Aggressive timeline that can't be met

Solution: Build in buffer, be realistic about regulatory timing

3. Weak Exclusivity

Problem: Loopholes allow seller to shop the deal

Solution: Clear, enforceable no-shop with appropriate remedies

4. Overconfident on Price

Problem: Specific price without adequate diligence

Solution: Use range or clearly condition on diligence findings

5. Ignoring Tax/Legal Structure

Problem: Proposed structure has significant tax or legal issues

Solution: Consult advisors before proposing structure

6. No Expense Protection

Problem: Significant diligence costs with no recourse if seller walks

Solution: Expense reimbursement or termination fee for bad faith

7. Forgetting Employee Commitments

Problem: No clarity on employee treatment

Solution: Specific commitments on key employee retention

Best Practices

For Buyers

- Do Sufficient Diligence First: Don't submit LOI too early

- Preserve Flexibility: Use ranges and conditions appropriately

- Secure Strong Exclusivity: This is your most important provision

- Be Realistic: Don't over-promise or propose unrealistic terms

- Move Quickly: Submit LOI when ready, then execute efficiently

For Sellers

- Create Competition: Multiple LOIs give leverage

- Read Carefully: Understand all provisions, especially what's binding

- Protect Downside: Ensure you can restart process if deal fails

- Maintain Leverage: Shorter exclusivity, ability to respond to offers

- Get it in Writing: All important commitments should be in LOI

For Both Parties

- Align on Process: Clear timeline and expectations

- Build Relationship: LOI is start of partnership, not adversarial

- Involve Advisors: Legal and financial counsel review

- Communicate Clearly: Address concerns and questions openly

- Set the Tone: Professional, collaborative approach

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)