Comparable Company Analysis

Comparable Company Analysis ("Comps" or "Trading Comps") is a relative valuation method that values a company based on how similar publicly-traded companies are valued by the market. This guide covers how to select, analyze, and apply comparable company multiples in M&A.

What is Comparable Company Analysis?

Definition: Valuation methodology that compares the target company's financial metrics and valuation multiples to similar publicly-traded companies.

Core Principle: Similar companies should trade at similar multiples. If Company A and Company B have similar growth, margins, and risk profiles, they should have similar EV/EBITDA multiples.

When to Use:

- Quick market-based valuation

- Triangulate with DCF analysis

- Understand market perception

- Set initial valuation expectations

- Price negotiation and justification

Advantages:

- Based on real market data

- Relatively quick to perform

- Easy to understand and explain

- Market reality check

Limitations:

- No two companies are truly identical

- Private company adjustments needed

- Market may be under/overvaluing sector

- Can be manipulated through comp selection

Step-by-Step Comps Process

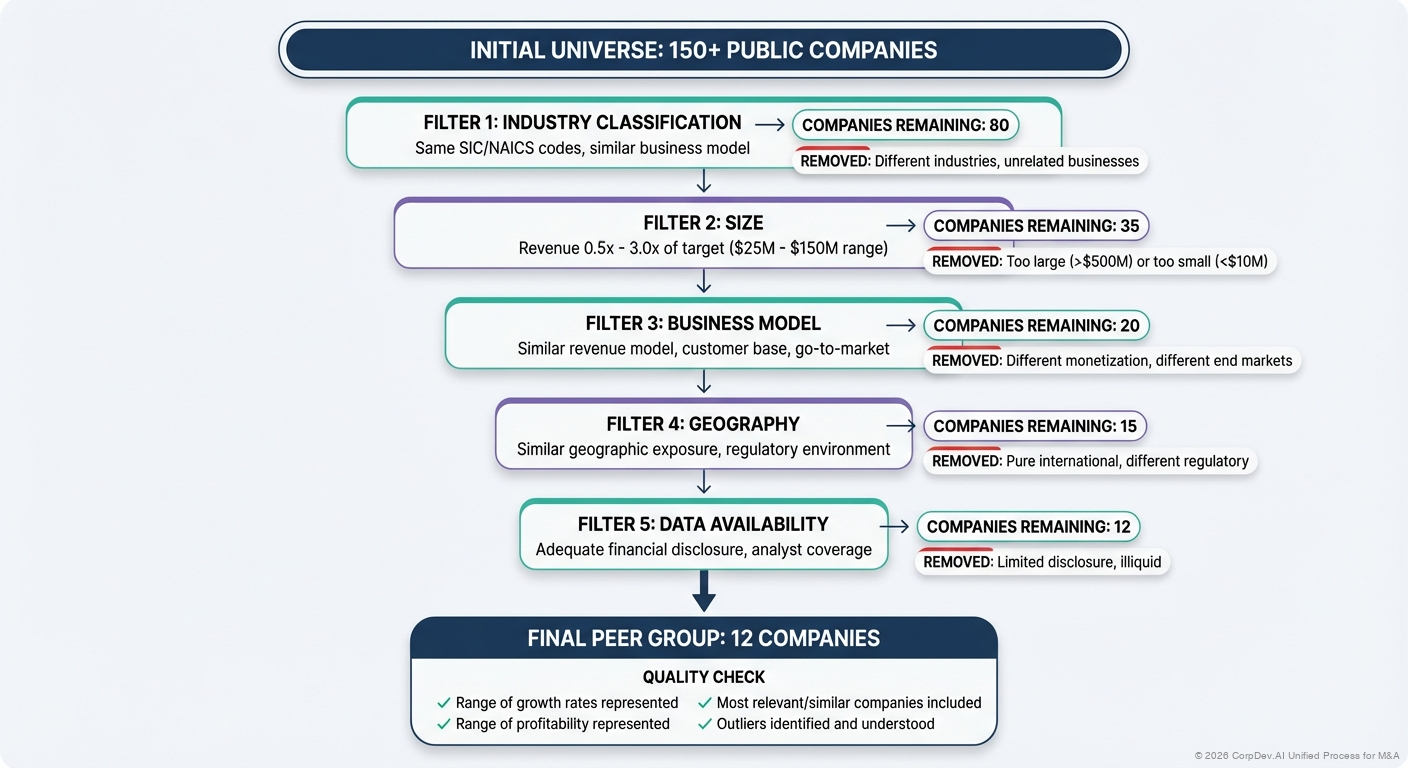

Step 1: Select Comparable Companies

Selection Criteria:

Industry/Sector (Most Important):

- Same primary business

- Similar products/services

- Same end markets

- Comparable business model

Size:

- Revenue within 0.5x - 2x of target

- For small targets, use larger comps (will trade at discount)

- Market cap considerations

Geography:

- Similar geographic footprint

- Same regulatory environment

- Comparable market dynamics

Growth Profile:

- Similar growth rates (±5-10%)

- Comparable maturity stage

- Similar expansion trajectory

Profitability:

- Similar margin structure

- Comparable unit economics

- Similar capital intensity

Other Factors:

- Public float / liquidity

- Capital structure

- Customer concentration

- Technology platform

Ideal Comp Universe: 5-15 companies

Example - SaaS Company Target:

Target Profile:

- $50M ARR, growing 40%

- Vertical SaaS for healthcare

- 75% gross margin, -10% EBITDA margin (investing in growth)

- SMB and Mid-market focus

Selected Comps:

- Veeva Systems (Healthcare vertical SaaS, $2B revenue)

- Phreesia ($250M revenue, similar profile)

- HealthStream ($250M revenue, healthcare learning)

- Certara ($350M revenue, healthcare software)

- Omnicell ($1B revenue, healthcare automation)

- Similar private market acquisitions

Step 2: Gather Financial Data

Required Data Points:

Market Data:

- Current stock price

- Shares outstanding (fully diluted)

- Market capitalization

- Net debt (debt - cash)

- Enterprise value

Income Statement:

- Revenue (current year, NTM, LTM)

- Gross profit and margin

- EBITDA and margin

- EBIT and margin

- Net income

- EPS

Balance Sheet:

- Total debt

- Cash and equivalents

- Book value of equity

Growth Metrics:

- Historical revenue growth (1yr, 3yr, 5yr)

- Projected revenue growth (NTM)

- EBITDA growth

Data Sources:

- Capital IQ, FactSet, Bloomberg (institutional)

- Company filings (10-K, 10-Q)

- Earnings presentations

- Consensus analyst estimates (for NTM)

- PitchBook, Crunchbase (private comps)

Step 3: Calculate Valuation Multiples

Enterprise Value Multiples:

EV / Revenue:

Enterprise Value / LTM Revenue

Enterprise Value / NTM Revenue

Use Cases:

- High-growth companies

- Pre-profitable companies

- SaaS and software

- Quickly screening companies

EV / EBITDA:

Enterprise Value / LTM EBITDA

Enterprise Value / NTM EBITDA

Use Cases:

- Mature, profitable companies

- Most common multiple in M&A

- Manufacturing, services, traditional sectors

- Comparing companies with different capital structures

EV / EBIT:

Enterprise Value / LTM EBIT

Use Cases:

- When D&A differs significantly

- Mature companies

- Less common than EV/EBITDA

Equity Value Multiples:

P/E Ratio:

Price per Share / Earnings per Share

Market Cap / Net Income

Use Cases:

- Comparing public companies

- Less relevant for M&A (focus on EV multiples)

Price / Book:

Market Cap / Book Value of Equity

Use Cases:

- Financial services (banks, insurance)

- Asset-heavy businesses

- Distressed situations

Industry-Specific Multiples:

SaaS / Software:

- EV / ARR (Annual Recurring Revenue)

- EV / Bookings

- Revenue per employee

Subscription Businesses:

- EV / Subscribers

- EV / MRR (Monthly Recurring Revenue)

E-commerce / Marketplaces:

- EV / GMV (Gross Merchandise Value)

- Take rate (% of GMV)

Media / Advertising:

- EV / Impressions

- EV / Users

- ARPU (Average Revenue Per User)

Healthcare / Biotech:

- EV / Addressable patients

- Pipeline value

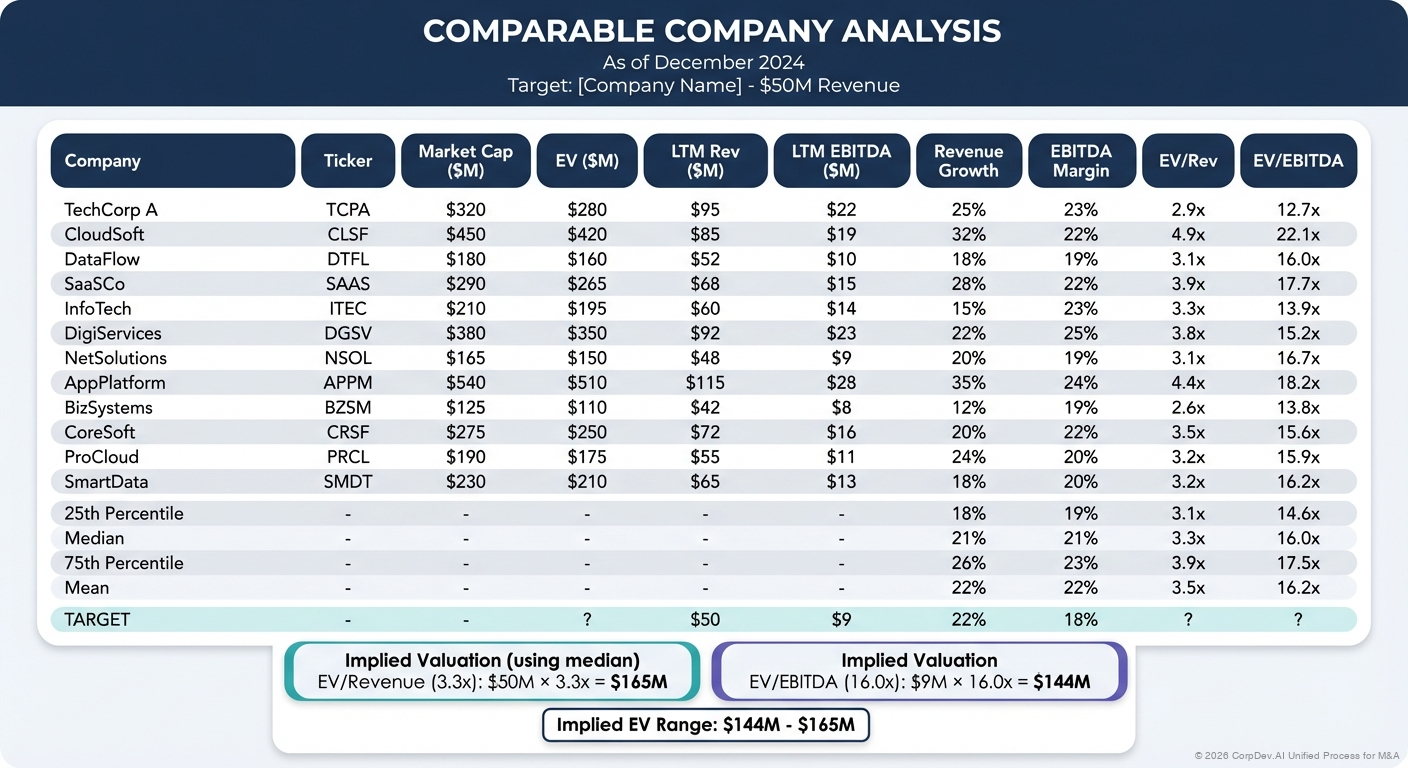

Step 4: Build Comparable Company Table

Example Comps Table (Simplified):

Market EV / EV / Revenue EBITDA

Company Ticker Cap ($M) EV ($M) Rev ($M) EBITDA ($M) Revenue EBITDA Growth Margin

─────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

Veeva Systems VEEV $35,200 $34,100 $2,200 $770 15.5x 44.3x 18% 35%

Phreesia PHR $1,800 $1,700 $250 $5 6.8x 340.0x 30% 2%

HealthStream HSTM $850 $800 $250 $50 3.2x 16.0x 5% 20%

Certara CERT $3,200 $3,500 $350 $105 10.0x 33.3x 25% 30%

Omnicell OMCL $4,500 $4,800 $1,200 $180 4.0x 26.7x 10% 15%

Mean 7.9x 92.1x 18% 20%

Median 6.8x 33.3x 18% 20%

────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

Target Company $50 $5 ? ? 40% -10%

Step 5: Normalize and Adjust Multiples

Adjustments to Consider:

Size Discount/Premium:

- Smaller companies trade at discount (10-30%)

- Liquidity and coverage impact multiples

- Consider applying 15-25% small-cap discount

Growth Adjustment:

- Higher growth deserves higher multiples

- Normalize for growth differences

- Common: Divide EV/Revenue by growth rate = PEG-style ratio

Profitability Adjustment:

- More profitable companies trade higher

- Adjust for EBITDA margin differences

- Rule of thumb: 0.5x EV/Revenue per 10% EBITDA margin

Private Company Discount:

- Private companies lack liquidity

- Typical discount: 20-30% vs. public comps

- Varies by situation and buyer

Control Premium:

- M&A transactions include control premium

- Typical: 20-35% above trading price

- Offsets some of the private discount

Example Adjustment:

Target: 40% growth, -10% EBITDA margin

Comps median: 18% growth, 20% EBITDA margin

Median EV/Revenue: 6.8x

Growth adjustment: +2.0x (22% higher growth)

Profitability adjustment: -1.5x (30% lower margins)

Adjusted multiple: 7.3x

Private company discount (20%): -1.5x

Control premium (25%): +1.4x

Net adjustment: -0.1x

Implied EV/Revenue: 7.2x

Step 6: Apply Multiples to Target

Method 1: Apply Range of Multiples

Target LTM Revenue: $50M

Low Median High

EV/Revenue Multiple 6.0x 7.2x 8.5x

Implied EV $300M $360M $425M

Method 2: Apply Multiple to Projected Financials

Target NTM Revenue: $70M (40% growth)

EV/Revenue Multiple: 7.2x

Implied EV: $504M

Target NTM EBITDA: $7M (10% margin)

EV/EBITDA Multiple: 35x

Implied EV: $245M

Range: $245M - $504M

Midpoint: $375M

Step 7: Calculate Equity Value

Enterprise Value: $360M

+ Cash: $5M

- Debt: ($10M)

- Minority Interest: $0M

- Preferred Stock: $0M

= Equity Value: $355M

Selecting the Right Multiple

By Company Stage:

Pre-Revenue / Early Stage:

- Can't use revenue or EBITDA multiples

- Use industry benchmarks

- Consider cost to replicate

- Precedent transaction analysis more useful

High Growth, Pre-Profitable (most tech):

- EV / Revenue primary metric

- Adjust for growth rate (Rule of 40)

- Consider path to profitability

- LTV/CAC ratio if available

Profitable Growth:

- EV / Revenue and EV / EBITDA

- Weight both multiples

- Consider both current and forward multiples

Mature / Stable:

- EV / EBITDA primary metric

- EV / EBIT if appropriate

- Focus on cash generation

- Consider FCF multiples

By Industry:

SaaS / Software:

- Primary: EV / ARR

- Secondary: EV / Revenue, growth-adjusted

- Rule of 40 (Growth + FCF Margin)

- CAC payback period

Manufacturing / Industrial:

- Primary: EV / EBITDA

- Consider capacity utilization

- Cyclical adjustments

Financial Services:

- P/E and Price/Book

- ROE considerations

- Regulatory capital requirements

Healthcare Services:

- EV / EBITDA

- Per-location or per-patient metrics

- Reimbursement environment

E-commerce / Marketplaces:

- EV / GMV

- Take rate

- Unit economics

The "Rule of 40" for SaaS

Formula:

Rule of 40 = Revenue Growth % + FCF Margin %

Interpretation:

40: Excellent, deserves premium multiple

- 30-40: Good performance

- <30: Needs improvement

Example:

Company A: 50% growth + (-10)% FCF margin = 40 ✓

Company B: 20% growth + 25% FCF margin = 45 ✓✓

Company C: 15% growth + 5% FCF margin = 20 ✗

Impact on Valuation:

Rule of 40 Score Typical EV/Revenue Multiple

50+ 15-25x

40-50 10-15x

30-40 6-10x

20-30 3-6x

<20 1-3x

Creating a Football Field Valuation

Visualize Range of Values:

Valuation Methodology Low Mid High

═══════════════════════════════════════════════════════════

DCF Analysis $300M ████████████████ $400M

Trading Comps $320M ████████████████████ $440M

Precedent Transactions $350M ████████████████████████ $480M

Implied Valuation Range: $320M ████████████████████ $440M

Target: $380M

Common Comparable Company Pitfalls

1. Cherry-Picking Comps

Problem: Selecting only high-multiple comparables

Solution:

- Use objective selection criteria

- Include all reasonable comps

- Show eliminated companies and rationale

- Consider both high and low multiples

2. Ignoring Differences

Problem: Treating all comps as equivalent

Solution:

- Analyze why multiples differ

- Adjust for growth, margins, size

- Weight more similar comps higher

- Explain differences to stakeholders

3. Over-Relying on Outliers

Problem: Using extreme high or low multiples

Solution:

- Use median, not mean

- Consider removing true outliers

- Understand why outliers exist

- Weight toward similar companies

4. Wrong Time Period

Problem: Using mismatched time periods

Solution:

- Consistent LTM vs. NTM across all comps

- Update for latest financials

- Consider forward-looking multiples

- Adjust for seasonality

5. Not Adjusting for Size

Problem: Comparing $50M company to $5B company

Solution:

- Apply size discount (15-30%)

- Focus on closer size comps

- Understand liquidity premium

- Consider scaling factors

6. Ignoring Market Conditions

Problem: Using comps during market extremes

Solution:

- Understand if sector is over/under-valued

- Look at historical trading ranges

- Consider normalizing multiples

- Use multiple timeframes if volatile

7. Capital Structure Confusion

Problem: Mixing EV and equity multiples

Solution:

- Use EV multiples for M&A (EV/Revenue, EV/EBITDA)

- Equity multiples (P/E) less relevant

- Understand leverage impact

- Normalize capital structure if needed

Best Practices

1. Cast a Wide Net Initially

Start with 20-30 potential comps, narrow to 8-12 best

2. Be Transparent

Show all comps, explain exclusions, document rationale

3. Multiple Metrics

Don't rely on single multiple - use 2-3 relevant metrics

4. Sanity Check

Does the implied valuation make sense?

- As % of revenue

- Per employee

- Per customer

- vs. historical transactions

5. Triangulate

Combine with DCF and precedent transactions

6. Update Regularly

Market multiples change - refresh for presentations

7. Understand the Story

Why do certain comps trade at premium/discount?

What drives valuation in this sector?

Advanced Topics

Regression Analysis

Statistical approach to adjusting for differences:

- Dependent variable: EV/Revenue

- Independent variables: Growth rate, EBITDA margin, size

- Generates predicted multiple for target's profile

Example:

Multiple = 2.0 + (0.15 × Growth%) + (0.10 × EBITDA Margin%)

Target: 40% growth, 20% EBITDA margin

Predicted Multiple = 2.0 + (0.15 × 40) + (0.10 × 20)

= 2.0 + 6.0 + 2.0

= 10.0x

Sum-of-the-Parts (SOTP)

For multi-segment companies:

- Value each segment separately

- Apply appropriate comps to each

- Sum segment values

- Add/subtract corporate costs

Precedent Acquisitions as Comparables

Sometimes treat acquired companies as comps:

- Use pre-acquisition trading multiples

- Adjust for time value

- Consider market conditions at acquisition

- Remember acquired cos traded with takeout premium

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)