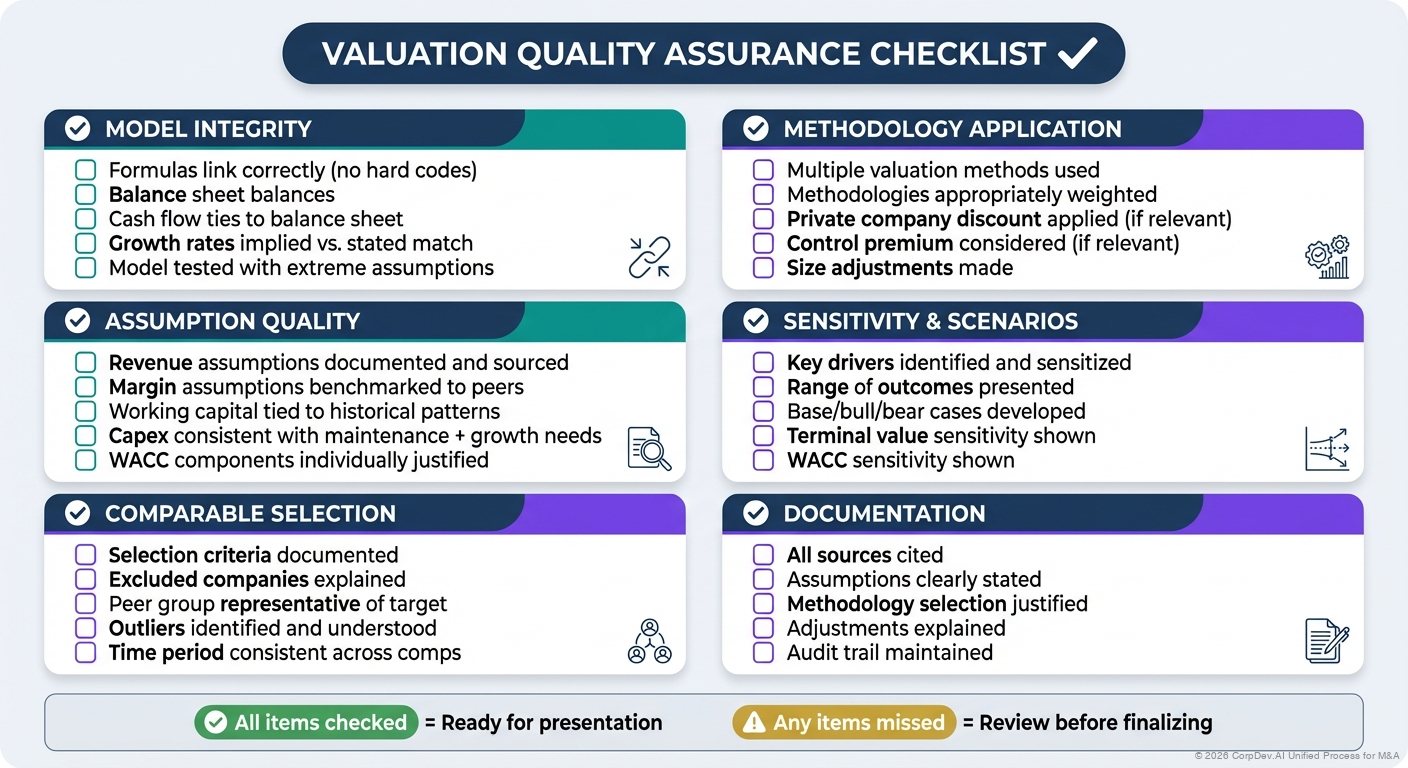

Valuation Best Practices & Pitfalls

Valuation is both art and science. No single method gives the "right" answer. The goal is to establish a defensible range and understand what drives value in your specific situation.

This guide covers advanced valuation techniques, common mistakes to avoid, and professional best practices for M&A valuation.

The Valuation Triangle

Three Pillars of Valuation

Intrinsic Value

DCF Analysis - What the business is fundamentally worth based on future cash flows

Market Value

Trading & Transaction Comps - What the market says similar assets are worth

Strategic Value

Synergies & Strategic Fit - What the business is worth TO YOU specifically

Best Practice: Use all three approaches and triangulate to a defensible range.

When to Use Each Valuation Method

| Method | Best For | Not Suitable For |

|---|---|---|

| DCF Analysis | Mature businesses, predictable cash flows, long-term holds | Pre-revenue, highly uncertain, turnarounds |

| Trading Comps | Quick valuation, market reality check, negotiation anchor | Truly unique businesses, no good public comps |

| Transaction Comps | M&A negotiations, understanding market appetite, precedent | Unique situations, no recent comparable deals |

| LBO Analysis | PE buyers, mature cash flows, leverage capacity assessment | High-growth unprofitable, strategic acquisitions |

| Asset-Based | Real estate, financial services, liquidation scenarios | IP/intangible-heavy businesses, going concerns |

Valuation by Company Stage

🚀 Early Stage

Pre-revenue or <$5M revenue

Primary Methods:

- Comparable transactions

- Venture capital method

- Cost to replicate

Key Drivers: Team, TAM, traction, technology

📈 Growth Stage

$5-50M revenue, high growth

Primary Methods:

- EV / Revenue multiples

- Trading comps

- Transaction comps

- DCF (with caution)

Key Drivers: Growth rate, unit economics, retention

💼 Mature

$50M+ revenue, profitable, stable

Primary Methods:

- DCF analysis (primary)

- EV / EBITDA multiples

- Transaction comps

- LBO analysis

Key Drivers: Cash flow, margins, market position

The 10 Commandments of Valuation

1. Thou Shalt Not Rely on One Method

Never base a valuation on a single methodology. Always triangulate using multiple approaches.

Why: Each method has biases and limitations. Multiple methods provide confidence and defensibility.

2. Garbage In, Garbage Out

Your valuation is only as good as your assumptions. Spend time getting the inputs right.

Best Practice: Document every assumption, source all data, and pressure-test projections.

3. Don't Fall in Love with the Deal

Valuation should be objective. Don't let desire to do the deal inflate your numbers.

Red Flag: If you find yourself justifying ever-higher valuations to make a deal work, step back.

4. Synergies Are Not Free Money

Be realistic about synergy capture. Most acquirers overestimate synergies and underestimate costs.

Rule of Thumb: Discount projected synergies by 30-40% for realistic case.

5. Understand the Business First

Never start modeling before you understand how the business actually makes money.

Best Practice: Spend days researching before opening Excel.

6. Be Conservative with Terminal Value

Terminal value often represents 60-80% of DCF value. Be conservative on growth assumptions.

Best Practice: Never exceed GDP growth (2-3%). Consider using exit multiple as cross-check.

7. Adjust for Size and Liquidity

Small, private companies should trade at a discount to large, liquid public companies.

Typical Adjustments: 15-30% discount for size, liquidity, and private company factors.

8. Market Multiples Change

Don't use 2021 multiples in a 2024 valuation. Adjust for market conditions.

Best Practice: Track how sector multiples have moved and adjust historical comps.

9. Sensitivity Analysis is Mandatory

Always show how valuation changes with different assumptions.

Why: Demonstrates rigor, identifies key value drivers, supports negotiation strategy.

10. Know Your Walk-Away Price

Establish maximum price before negotiations begin. Have discipline to walk away.

Best Practice: Set walk-away price 10-15% above base case to leave negotiating room.

Common Valuation Pitfalls

❌ Hockey Stick Projections

Problem: Flat historical growth, then sudden acceleration

Fix: Justify with specific initiatives, benchmark against peers, stress test downside

❌ Ignoring Working Capital

Problem: Forgetting that growth consumes cash

Fix: Model WC as % of revenue, understand cash conversion cycle

❌ Circular WACC References

Problem: WACC depends on value, value depends on WACC

Fix: Use industry capital structure or iterate to convergence

❌ Cherry-Picking Comps

Problem: Selecting only high-multiple comparables

Fix: Use objective criteria, show full comp set, use median

❌ Overstating Synergies

Problem: Aggressive synergy assumptions to justify price

Fix: Bottom-up synergy build, risk-adjust, deduct integration costs

❌ No Sensitivity Analysis

Problem: Presenting single-point valuation

Fix: Always show range, sensitize key assumptions, scenario analysis

Valuation Red Flags

🚨 Warning Signs Your Valuation May Be Wrong

Terminal Value > 80% of Total Value

- Indicates over-reliance on far-future assumptions

- Consider extending projection period or reducing terminal growth

Implied Multiples Way Above/Below Comps

- DCF implies 15x revenue, comps trade at 6x

- Either your assumptions are aggressive or market is wrong (probably former)

Synergies Required to Hit Return Threshold

- If you need synergies to justify price, you're paying for synergies

- Consider standalone value ceiling

"New Paradigm" Arguments

- "This time is different" is usually wrong

- Historical valuation relationships exist for a reason

Model Shows Value Regardless of Assumptions

- If every scenario shows great value, model may be flawed

- Test with truly conservative assumptions

Professional Valuation Process

1. Preparation Phase (Week 1)

Research & Due Diligence:

- Industry dynamics and trends

- Competitive landscape

- Company's position and differentiation

- Financial statement analysis

- Management discussions

- Customer and partner feedback

Data Collection:

- Historical financials (3-5 years)

- Management projections

- Comparable companies

- Precedent transactions

- Industry benchmarks

2. Modeling Phase (Week 2-3)

Build Models:

- DCF model with detailed assumptions

- Comparable company analysis

- Precedent transaction analysis

- Additional methods as appropriate

Sensitivity Analysis:

- Key variable sensitivities

- Scenario analysis (base, upside, downside)

- Monte Carlo if appropriate

3. Synthesis Phase (Week 3-4)

Triangulate:

- Compare results across methodologies

- Identify and reconcile differences

- Weight methods appropriately

- Establish defensible range

Strategic Considerations:

- Synergy potential (quantified)

- Strategic value to acquirer

- Competitive dynamics

- Alternative uses of capital

4. Presentation Phase (Week 4)

Deliver Recommendation:

- Executive summary with range

- Detailed methodology walkthrough

- Key assumptions and sensitivities

- Strategic rationale

- Risk factors

- Negotiation strategy

Valuation Presentation Best Practices

The Perfect Valuation Book Structure

■ Executive Summary

- Recommended valuation range

- Key findings and drivers

- Strategic rationale

■ Company Overview

- Business model and operations

- Financial performance

- Market position

■ DCF Analysis

- Assumptions and projections

- WACC calculation

- Sensitivity analysis

■ Comparable Company Analysis

- Comp selection and screens

- Multiple analysis

- Adjustments and implications

■ Precedent Transaction Analysis

- Transaction selection

- Multiple analysis

- Market context

■ Football Field Summary

- Visual range comparison

- Recommended range

- Bridge to offer price

■ Appendix

- Detailed financials

- Comparable company profiles

- Transaction details

- Source documentation

Quick Reference: Valuation Ranges by Industry

| Industry | EV/Revenue | EV/EBITDA | Key Drivers |

|---|---|---|---|

| SaaS (High Growth) | 8-15x | 30-50x | ARR growth, NDR, Rule of 40 |

| SaaS (Mature) | 4-8x | 15-25x | FCF margin, customer concentration |

| Healthcare Services | 1-3x | 8-14x | Reimbursement, same-store growth |

| Manufacturing | 0.5-2x | 6-12x | Margins, capacity utilization |

| E-commerce | 0.5-2x | 8-15x | CAC/LTV, repeat rates, logistics |

| Marketplaces | 3-8x | 15-30x | GMV growth, take rate, network effects |

| Business Services | 1-3x | 8-14x | Retention, margins, scalability |

Final Thoughts

Remember: Valuation is a Range, Not a Number

Anyone who gives you a single-point valuation is either naive or misleading you. Professional valuations always present a defensible range with clear assumptions and sensitivities.

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)