Precedent Transaction Analysis

Precedent Transaction Analysis ("Transaction Comps" or "M&A Comps") values a company based on the purchase prices paid in comparable M&A transactions. This guide covers how to identify, analyze, and apply precedent transactions to current valuations.

What is Precedent Transaction Analysis?

Definition: Valuation methodology that analyzes the prices paid for similar companies in past M&A transactions to determine an appropriate valuation range.

Core Principle: If Company X was acquired at 8x revenue, and your target is similar to Company X, it should be valued around 8x revenue.

Key Difference from Trading Comps:

- Trading comps = minority stake, public market value

- Transaction comps = control premium, strategic value included

- Transaction multiples typically 20-40% higher than trading multiples

When to Use:

- Negotiating purchase price

- Justifying valuation to board

- Understanding market appetite

- Competitive bid situations

- Setting walk-away price

Advantages:

- Reflects actual M&A market prices

- Includes control premium

- Shows strategic value buyers will pay

- Reality check on valuation

Limitations:

- Each deal is unique (synergies, timing, buyers)

- Historical data may not reflect current market

- Deal details often limited

- Synergies not disclosed

- Small sample sizes

Step-by-Step Process

Step 1: Identify Relevant Transactions

Selection Criteria:

Industry/Sector (Critical):

- Same or closely related industry

- Similar business model

- Comparable products/services

- Same end markets

Size:

- Revenue within 0.25x - 3x of target

- More lenient than trading comps

- Consider enterprise value too

Timing:

- Last 2-3 years preferred

- Up to 5 years if limited data

- Avoid very old transactions (market changes)

- Consider market conditions at time

Geography:

- Same or similar markets

- Consider cross-border premium/discount

- Regulatory environment

Transaction Type:

- Strategic vs. financial buyer

- Stock vs. cash consideration

- Public vs. private target

- Competitive auction vs. negotiated

Deal Status:

- Completed transactions preferred

- Announced but pending can be included

- Avoid terminated deals

Target Universe: 8-15 transactions (fewer than trading comps)

Example - SaaS Company Target:

Target Profile:

- Vertical SaaS for healthcare providers

- $50M ARR, 40% growth

- 75% gross margin, breaking even on EBITDA

- 1,200 customers, mostly SMB

Selected Precedent Transactions:

- Phreesia acquired HealthCare Software Co ($240M revenue) - 2023

- Oracle acquired Cerner ($5B revenue) - 2022

- Nordic Capital acquired Cority ($150M revenue) - 2023

- Vista Equity acquired Greenway ($520M revenue) - 2023

- Thoma Bravo acquired Qventus ($80M revenue) - 2024

- Providence Equity acquired Definitive Healthcare - 2023

- Blackstone acquired MedHOK ($200M revenue) - 2022

Step 2: Gather Transaction Details

Required Information:

Deal Terms:

- Announcement date

- Close date (if completed)

- Purchase price / enterprise value

- Form of consideration (cash, stock, mix)

- Earnout or contingent consideration

Target Company Financials:

- LTM revenue at time of acquisition

- NTM revenue projections (if available)

- EBITDA (LTM and/or NTM)

- EBIT

- Growth rate (historical)

- Margins

Transaction Context:

- Buyer identity and type (strategic vs. PE)

- Competitive process (auction vs. negotiated)

- Strategic rationale disclosed

- Synergy expectations (if disclosed)

Data Sources:

Public Sources:

- SEC filings (Form S-4, proxy statements)

- Press releases

- Earnings call transcripts

- News articles

Databases:

- Capital IQ M&A Database

- PitchBook

- FactSet M&A

- MergerMarket

- 451 Research (for tech)

- Refinitiv (formerly Thomson Reuters)

Challenges:

- Private company targets = limited disclosure

- Synergies rarely disclosed

- Earnouts often confidential

- Working capital adjustments unknown

Step 3: Calculate Transaction Multiples

Enterprise Value Multiples:

EV / LTM Revenue:

Transaction Enterprise Value / Last Twelve Months Revenue

EV / NTM Revenue:

Transaction Enterprise Value / Next Twelve Months Revenue

EV / LTM EBITDA:

Transaction Enterprise Value / Last Twelve Months EBITDA

Calculating Enterprise Value:

Equity Purchase Price

+ Debt Assumed

- Cash Acquired

+ Transaction Fees and Costs (if included)

+ Earnouts (sometimes included at full value)

= Transaction Enterprise Value

Example Calculation:

Purchase Price: $300M (80% cash, 20% stock)

+ Debt Assumed: $15M

- Cash Acquired: ($25M)

+ Earnout (full value): $50M

Transaction EV: $340M

Target LTM Revenue: $60M

Target LTM EBITDA: $8M

EV / Revenue: 5.7x

EV / EBITDA: 42.5x

Step 4: Build Transaction Comparable Table

Example Transaction Comps Table:

EV / EV / Target Target

Target Acquirer Date EV ($M) Revenue ($M) EBITDA ($M) Revenue EBITDA Growth Margin

──────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

HealthCare SW Co Phreesia Q1 2023 $1,800 $240 $48 7.5x 37.5x 35% 20%

Cerner Oracle Q2 2022 $28,300 $5,500 $1,375 5.1x 20.6x 6% 25%

Cority Nordic Cap Q3 2023 $1,200 $150 $30 8.0x 40.0x 28% 20%

Greenway Vista Equity Q1 2023 $1,560 $520 $104 3.0x 15.0x 8% 20%

Qventus Thoma Bravo Q2 2024 $720 $80 $5 9.0x 144.0x 45% 6%

Definitive HC Providence Q4 2023 $4,200 $350 $105 12.0x 40.0x 25% 30%

MedHOK Blackstone Q3 2022 $1,600 $200 $40 8.0x 40.0x 22% 20%

25th Percentile 5.1x 20.6x

Median 7.5x 40.0x

75th Percentile 8.5x 41.3x

Mean 7.5x 48.2x

──────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

Your Target $50 $5 ? ? 40% 10%

Step 5: Analyze and Adjust Multiples

Factors Impacting Transaction Multiples:

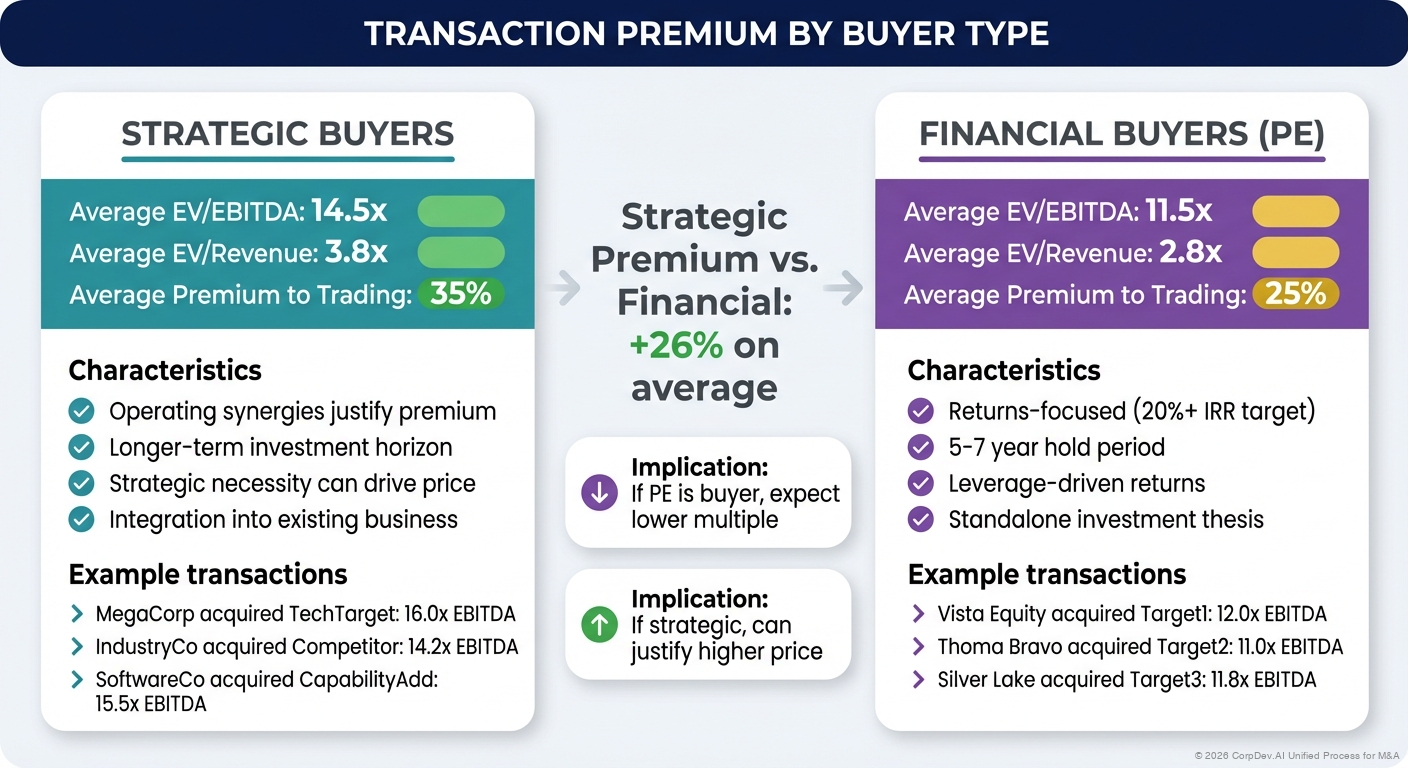

Buyer Type:

- Strategic buyers: Pay more (synergies), 20-40% premium

- Financial buyers (PE): More disciplined, return-focused

- Corporate PE: Hybrid approach

Deal Process:

- Competitive auction: Higher multiples (10-30% premium)

- Negotiated sale: Lower multiples, but may get better terms

- Pre-emptive bid: Premium to avoid auction

Market Conditions:

- Bull market: Higher multiples

- Bear market: Lower multiples

- Low interest rates: Higher multiples (cheaper financing)

- Hot sector: Premium multiples

Target Characteristics:

- Growth rate: Higher growth = higher multiple

- Profitability: Better margins = higher multiple

- Customer quality: Stickier customers = premium

- Market position: Leaders command premium

- Management team: Strong team adds value

Urgency/Motivation:

- Distressed sale: Discounted price

- Strategic necessity: Premium price

- Founder liquidity event: May accept lower price

- Competitive threat: Premium to secure deal

Size:

- Larger deals often at lower multiples

- Smaller deals may have scarcity premium

- Adjust for size differences

Consideration Type:

- All cash: Typically values higher

- Stock consideration: Subject to market risk, may discount

- Earnouts: Discounted value (risk of non-payment)

Step 6: Apply Adjusted Multiples to Target

Method 1: Simple Range Application

Target LTM Revenue: $50M

Transaction Multiples:

- 25th Percentile: 5.1x

- Median: 7.5x

- 75th Percentile: 8.5x

Implied EV Range:

- Low (25th %ile): $255M

- Mid (Median): $375M

- High (75th %ile): $425M

Method 2: Adjust for Target Characteristics

Median Transaction Multiple: 7.5x EV/Revenue

Adjustments:

+ Higher growth (40% vs 25% median): +1.0x

- Lower profitability (10% vs 20% median margins): -0.8x

+ Competitive auction expected: +0.5x

- Smaller size: -0.5x

Adjusted Multiple: 7.7x

Target Revenue: $50M

Implied EV: $385M

Method 3: Regression-Based

Run regression: Transaction Multiple = f(Growth, Margin, Size, Year)

Predict multiple based on target's characteristics

Step 7: Compare to Trading Comps

Implied Control Premium:

Transaction Multiple - Trading Multiple = Control Premium

Example:

Transaction EV/Revenue: 7.5x

Trading Comp EV/Revenue: 5.8x

Implied Premium: 29%

Typical Range: 20-35%

Triangulate Value:

Low Mid High

Trading Comps (Minority) $280M $320M $360M

Control Premium (25%) $70M $80M $90M

Transaction Comps $320M $375M $425M

Key Considerations

Transaction Synergies

Problem: Disclosed multiples may include buyer-specific synergies

Analysis:

- Try to identify synergy potential from deal rationale

- Adjust multiples downward if massive synergies expected

- Consider your company's synergy potential

Example:

Announced Deal: $400M (10x revenue)

Disclosed synergies: $100M PV

Standalone value: ~$300M (7.5x revenue)

Your synergies: $60M PV

Justified price: ~$360M (9x revenue)

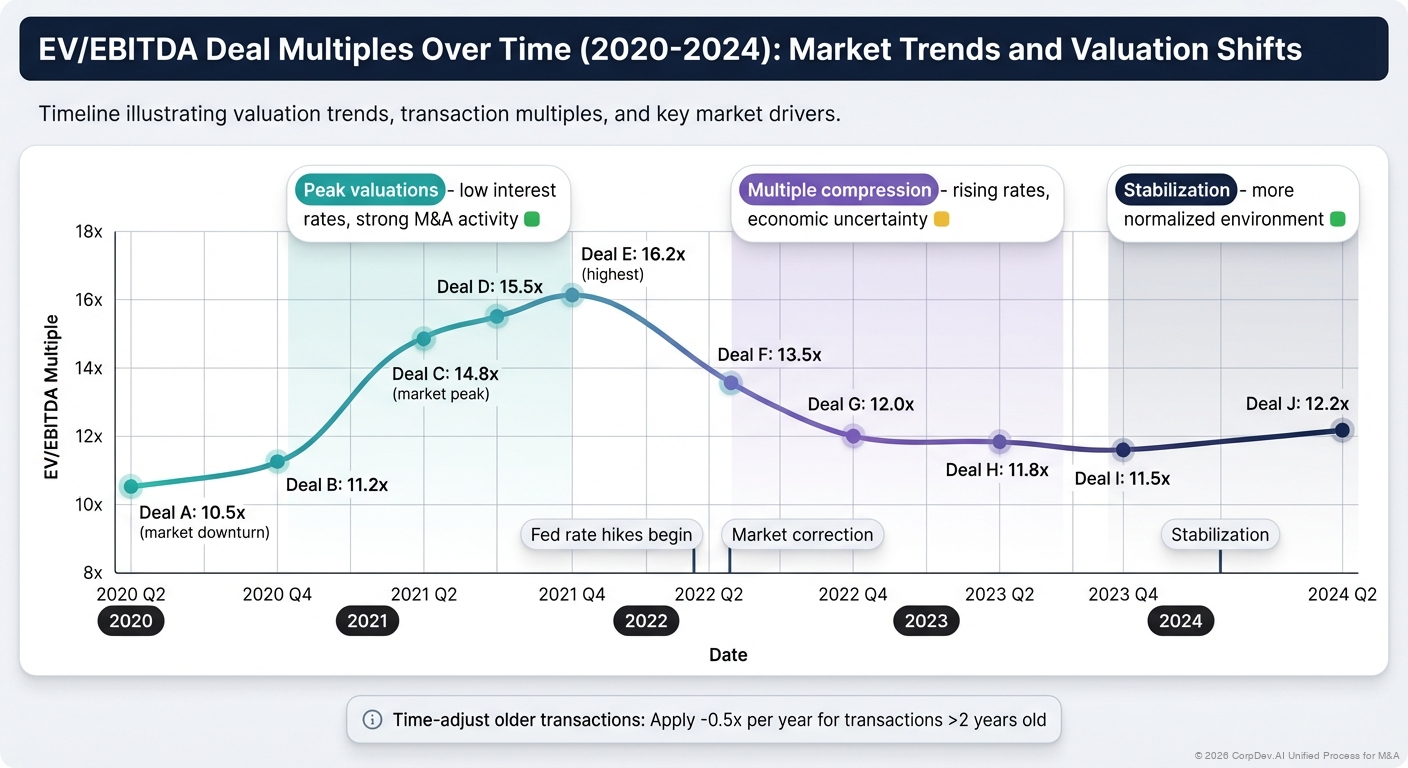

Market Timing Adjustments

Older Transactions:

- Adjust for market multiple expansion/contraction

- Use public market indices as reference

Example:

Transaction from 2021: 12x EV/Revenue

SaaS index was at 15x then, now at 8x

Adjusted multiple: 12x × (8x / 15x) = 6.4x

Earnout Considerations

Treatment:

- Sometimes earnouts included at full value in reported EV

- Sometimes excluded

- Risk-adjust earnouts (typically 50-70% of max value)

Example:

Reported Deal Value: $100M

Base: $70M

Earnout (max): $30M

Realistic earnout value: $20M (67% of max)

Effective EV: $90M

Use $90M for multiple calculations

Limited Data Quality

Private Target Limitations:

- Financials often not disclosed

- May only know purchase price

- Estimates from industry sources

- Triangulate with known data points

Strategies:

- Use deals with disclosed financials

- Apply industry benchmarks for missing data

- Focus on deals with better disclosure

- Be transparent about data quality

Putting It All Together: Football Field

Visual Valuation Range:

Methodology Low ├─────────────┤ High

DCF Analysis $300M ████████████████████ $420M

Trading Comps $280M ██████████████████ $360M

+ Control Premium (25%) ██████████████████████ $450M

= Implied Transaction $350M ████████████████████████ $450M

Precedent Transactions $320M ████████████████████████ $425M

────────────────────────────────────────────────────────

Valuation Range $320M ████████████████████████ $425M

Recommended: $375M - $400M

Common Pitfalls

1. Ignoring Market Conditions

Problem: Using 2021 multiples in 2024 downturn

Solution: Adjust for market changes, consider macro environment

2. Mixing Buyer Types

Problem: Comparing strategic deal to financial buyer deal

Solution: Segment by buyer type, understand buyer's motivation

3. Not Accounting for Deal Structure

Problem: Treating all-cash deal same as stock deal

Solution: Adjust for consideration type, earnout risk

4. Overlooking Synergies

Problem: Assuming precedent multiple is standalone value

Solution: Try to identify synergy component, adjust accordingly

5. Small Sample Size

Problem: Only 2-3 relevant transactions

Solution: Expand criteria carefully, supplement with trading comps

6. Cherry-Picking High Multiples

Problem: Only citing the highest multiple transactions

Solution: Show full range, use median, explain outliers

7. Ignoring Failed Deals

Problem: Only looking at completed deals

Solution: Consider why some deals didn't close, understand limits

Best Practices

1. Recent and Relevant

Prioritize transactions from last 2 years in same sector

2. Understand the Why

Research deal rationale - synergies, strategic fit, competitive dynamics

3. Multiple Perspectives

Look at both EV/Revenue and EV/EBITDA if applicable

4. Document Everything

Track sources, assumptions, adjustments transparently

5. Triangulate

Never rely solely on transaction comps - use with DCF and trading comps

6. Sensitivity Analysis

Show how valuation changes with different multiple selections

7. Tell the Story

Explain to stakeholders how transactions relate to your situation

Advanced Analysis

Deal Wave Analysis

Track multiples over time in your sector:

Period Median EV/Revenue # of Deals

2019 6.5x 45

2020 7.2x 38

2021 10.5x 67

2022 8.1x 41

2023 6.8x 35

2024 YTD 7.0x 28

Current environment: 7.0x (below 5-year average of 7.8x)

Strategic vs. Financial Buyer Analysis

Buyer Type Avg Multiple Premium vs. Financial

Strategic 8.5x +25%

Financial (PE) 6.8x baseline

Corporate PE 7.5x +10%

Size-Adjusted Analysis

Deal Size Avg EV/Revenue Multiple

< $100M 9.5x

$100-500M 7.2x

$500M - $1B 6.5x

> $1B 5.8x

Competitive Process Impact

Process Type Avg Premium

Broad Auction Base

Targeted Auction -8%

Negotiated Sale -15%

Pre-emptive Offer +12%

Precedent Transactions Checklist

Before finalizing analysis, verify:

- Selected transactions are truly comparable

- Financials are from same time period (all LTM or all NTM)

- Enterprise values calculated consistently

- Synergies considered and adjusted for

- Market timing differences accounted for

- Deal structure differences noted

- Control premium vs. trading comps makes sense

- Sample size is adequate (ideally 8-12 deals)

- Outliers identified and explained

- Data sources documented

- Results triangulated with other methods

Example: Complete Analysis

Target: Healthcare IT SaaS company, $50M revenue, 40% growth

Selected Transactions (7 deals, past 2 years)

Multiple Analysis:

EV / Revenue Multiples:

- Low: 5.1x

- 25th Percentile: 6.8x

- Median: 7.5x

- 75th Percentile: 8.5x

- High: 12.0x (outlier - strategic necessity deal)

Excluding outlier:

- Adjusted Median: 7.5x

- Mean: 7.3x

Adjustments:

Base (Median): 7.5x

+ Higher growth (+1.0x)

- Smaller size (-0.5x)

+ Competitive buyer interest (+0.5x)

= Adjusted: 8.5x

Valuation:

EV/Revenue Multiple: 7.5x - 8.5x

Target Revenue: $50M

Implied EV: $375M - $425M

Midpoint: $400M

Compare to Trading Comps:

Trading Comp EV/Revenue: 6.0x

Implied EV: $300M

Control Premium: 33% ($100M)

Supports transaction comp range

Recommendation:

Valuation Range: $375M - $425M

Target Price: $400M

Walk-Away Price: $450M

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)