Investment Committee Presentations for M&A

The Investment Committee (IC) presentation is your opportunity to secure approval for an M&A transaction. A well-crafted IC deck tells a compelling story, addresses concerns head-on, and demonstrates rigorous analysis.

What is an IC Presentation?

Purpose

An IC presentation (also called Board presentation for larger deals) is a formal pitch to decision-makers requesting approval to:

- Execute a Letter of Intent (LOI)

- Proceed with full due diligence

- Submit binding offer

- Execute definitive agreement

- Close transaction

Typical Audience

- Investment Committee: CFO, CEO, COO, Head of Corp Dev, Business Unit leads

- Board of Directors (deals >$X threshold or strategic importance)

- Private Equity IC (for PE-backed companies or PE buyers)

Decision Criteria

IC evaluates deals on:

- Strategic Fit: Does this serve our strategy?

- Financial Returns: Does this meet hurdle rates?

- Risk: Can we manage downside scenarios?

- Execution: Can we successfully integrate?

- Alternatives: Is this our best use of capital?

Great IC presentations are: (1) Concise - 15-25 slides, (2) Fact-based - data over opinions, (3) Balanced - acknowledge risks, (4) Clear - simple language, strong visuals, (5) Actionable - specific recommendation and ask.

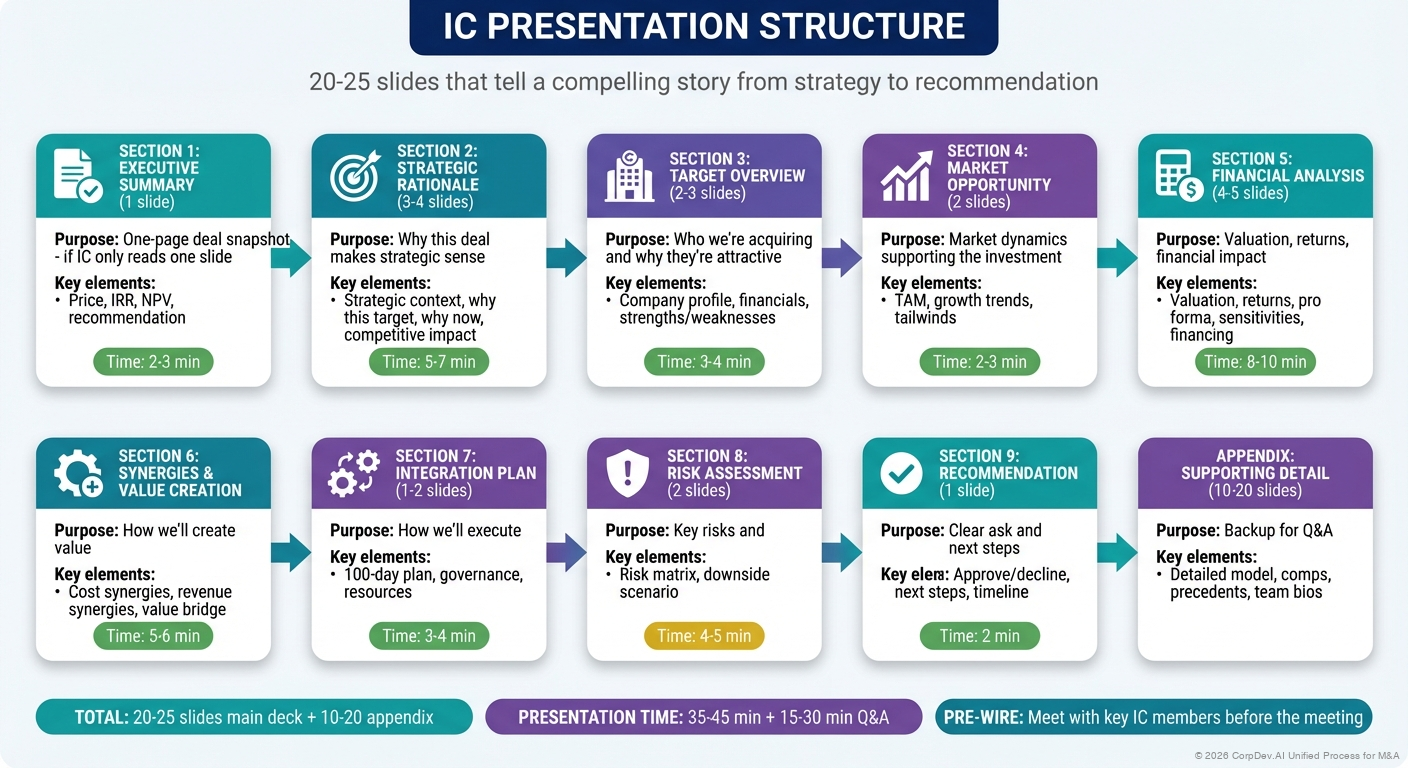

IC Presentation Structure

Recommended Flow (20-25 Slides)

| Section | Slides | Purpose |

|---|---|---|

| 1. Executive Summary | 1 | One-page deal snapshot |

| 2. Strategic Rationale | 3-4 | Why this deal makes strategic sense |

| 3. Target Overview | 2-3 | Who we're acquiring and why they're attractive |

| 4. Market Opportunity | 2 | Market dynamics supporting the investment |

| 5. Financial Analysis | 4-5 | Valuation, returns, financial impact |

| 6. Synergies & Value Creation | 2-3 | How we'll create value |

| 7. Integration Plan | 1-2 | How we'll execute |

| 8. Risk Assessment | 2 | Key risks and mitigations |

| 9. Recommendation | 1 | Clear ask and next steps |

| Appendix | 10-20 | Supporting detail for Q&A |

Slide-by-Slide Breakdown

Slide 1: Executive Summary

The "If You Only Read One Slide" Page

┌────────────────────────────────────────────────────────┐

│ EXECUTIVE SUMMARY: [Target Name] Acquisition │

├────────────────────────────────────────────────────────┤

│ │

│ TRANSACTION OVERVIEW │

│ • Target: [Name], [description in 1 sentence] │

│ • Purchase Price: $[X]M ([X.X]x Revenue, [X.X]x EBITDA) │

│ • Structure: [Cash/Stock/Mix] │

│ • Expected Close: [Q/Year] │

│ │

│ STRATEGIC RATIONALE │

│ [2-3 bullets summarizing why this deal makes sense] │

│ │

│ FINANCIAL RETURNS (BASE CASE) │

│ • IRR: [X]% (vs. [X]% hurdle) │

│ • NPV: $[X]M │

│ • EPS Impact (Year 2): [X]% accretive │

│ • Payback: [X] years │

│ │

│ KEY RISKS & MITIGATIONS │

│ [Top 2 risks with 1-line mitigation each] │

│ │

│ RECOMMENDATION │

│ [✓ Approve / Approve with conditions / Decline] │

│ │

└────────────────────────────────────────────────────────┘

Best Practices

- This slide should stand alone if it's all IC reads

- Use specific numbers, not ranges or vague language

- Bold the "big number" metrics (IRR, NPV, Price)

- State recommendation clearly (don't bury it)

Slides 2-5: Strategic Rationale

Slide 2: Strategic Context

Show where company is today and strategic gap:

OUR STRATEGIC PRIORITIES TARGET ADDRESSES

┌─────────────────────┐ ┌─────────────────────┐

│ 1. Enter cloud security → Provides market-leading │

│ market cloud security platform│

│ │

│ 2. Expand enterprise → 650 enterprise customers │

│ customer base with $50K+ ACV │

│ │

│ 3. Accelerate SaaS → 85% recurring revenue, │

│ transition cloud-native stack │

└─────────────────────┘ └─────────────────────┘

Slide 3: Why This Deal / Why Now

| Question | Answer |

|---|---|

| Why This Target? | [Unique capabilities, market position, or assets vs. alternatives] |

| Why Not Build? | [Time/risk/cost rationale - e.g., "Would take 3+ years and $100M+ with high execution risk"] |

| Why Now? | [Market timing, competitive dynamics, window of opportunity] |

Slide 4: Strategic Archetype

Clearly state primary strategic driver:

Capability Acquisition - Technology

Acquire market-leading cloud security platform with proprietary AI-powered threat detection, enabling us to compete for enterprise-wide security contracts worth $500M+ annually. This technology would take 3+ years and $100M+ to build organically, with uncertain competitive positioning.

Slide 5: Competitive Positioning

Show how deal strengthens competitive position:

CURRENT STATE POST-ACQUISITION

┌─────────┐ ┌─────────┐

│ Player A│ 30% │ US │ 28%

├─────────┤ ├─────────┤

│ Player B│ 22% │ Player A│ 25%

├─────────┤ → ├─────────┤

│ US │ 15% │ Player B│ 22%

├─────────┤ ├─────────┤

│ Target │ 13% │ Others │ 25%

├─────────┤ └─────────┘

│ Others │ 20%

└─────────┘

RANK: #3 → #1 SHARE: 15% → 28%

Slides 6-8: Target Overview

Slide 6: Target Company Profile

┌────────────────────────────────────────────────────────┐

│ [COMPANY LOGO] │

│ │

│ COMPANY OVERVIEW │

│ • Founded: [Year] │ HQ: [Location] │ Employees: [X] │

│ • [1-sentence description of what company does] │

│ │

│ FINANCIAL HIGHLIGHTS (LTM) │

│ • Revenue: $[X]M (+[X]% YoY) │

│ • EBITDA: $[X]M ([X]% margin) │

│ • ARR: $[X]M ([X]% recurring) │

│ │

│ KEY METRICS │

│ • Customers: [X] ([X]% enterprise, [X]% SMB) │

│ • NRR: [X]% │

│ • CAC Payback: [X] months │

│ • Rule of 40: [X] │

│ │

│ COMPETITIVE POSITION │

│ • Market share: [X]% ([#X] player in $[X]B market) │

│ • Key differentiators: [2-3 bullets] │

│ │

└────────────────────────────────────────────────────────┘

Slide 7: Target Financial Performance

Show historical and projected performance:

REVENUE & GROWTH EBITDA MARGIN

$150M ┃ 30% ┃

┃ ██ ┃ ╱╱

$100M ┃ ██ ██ 20% ┃ ╱╱

┃ ██ ██ ┃ ╱╱

$50M ┃ 10% ┃

┗━━━━━━━━━━━━ ┗━━━━━━━━━━━━

2021 2022 2023 2024E 2021 2022 2023 2024E

+25% +32% +28% +25% 18% 22% 25% 27%

Slide 8: Target Strengths & Weaknesses

| Strengths (Why Attractive) | Weaknesses/Risks (What We Fix) |

|---|---|

| ✓ Market-leading technology | ✗ Limited go-to-market resources |

| ✓ Strong customer retention (95% NRR) | ✗ Geographic concentration (85% US) |

| ✓ Proven management team | ✗ Underinvested in product (opportunity) |

| ✓ Scalable SaaS platform | ✗ Weak international presence |

Slides 9-10: Market Opportunity

Slide 9: Market Size & Growth

TOTAL ADDRESSABLE MARKET (TAM)

$50B ┃

┃ ██

$40B ┃ ██

┃ ██

$30B ┃ ██

┃ ██ ← $42B by 2027

$20B ┃ ██ 15% CAGR

┃ ██

$10B ┃ ██

┃ ██ ← $18B today

┗━━━━━━━━━━━━━━━━━━━━━━━

2023 2024 2025 2026 2027

COMBINED SHARE: 2.8% → Significant runway for growth

Slide 10: Market Trends & Tailwinds

KEY MARKET DRIVERS

1. 📈 Cloud Migration Accelerating

- 70% of enterprises migrating to cloud by 2025

- Security spending growing 2x faster than overall IT

2. 🔒 Regulatory Requirements Increasing

- GDPR, CCPA, SOC2 driving security investment

- Compliance spending up 25% YoY

3. 🎯 Consolidation Preference

- CIOs prefer integrated platforms vs. point solutions

- Average enterprise uses 50+ security tools (reducing to 10-15)

4. 💰 Favorable Pricing Environment

- Willingness to pay for AI-powered security

- Security budgets resilient even in downturn

Slides 11-15: Financial Analysis

Slide 11: Valuation Summary

VALUATION ANALYSIS

Method Implied Value Weight Weighted Value

───────────────────── ────────────── ────── ──────────────

DCF (WACC 10.5%) $450M - $550M 40% $500M

Comparable Companies $420M - $520M 30% $470M

Precedent Transactions $480M - $580M 30% $530M

─────────────

FAIR VALUE RANGE $490M

PURCHASE PRICE: $500M

Valuation Multiples:

• EV/Revenue (LTM): 3.5x (vs. comps median 3.2x)

• EV/EBITDA (LTM): 11.5x (vs. comps median 10.8x)

• EV/ARR: 4.0x (vs. SaaS median 4.2x)

ASSESSMENT: ✓ Fair value, slight premium justified by strategic fit

Slide 12: Returns Analysis

BASE CASE FINANCIAL RETURNS

┌──────────────────┬────────────┬────────────┬────────────┐

│ Metric │ Base Case │ Upside │ Downside │

├──────────────────┼────────────┼────────────┼────────────┤

│ IRR │ 18.5% │ 24.2% │ 12.1% │

│ NPV │ $120M │ $250M │ $40M │

│ Payback Period │ 4.2 yrs │ 3.1 yrs │ 6.5 yrs │

│ ROIC (Year 3) │ 14.2% │ 18.5% │ 9.8% │

│ EPS Accretion Y2 │ 8.5% │ 12.0% │ 3.2% │

└──────────────────┴────────────┴────────────┴────────────┘

Probability Weight: 60% 20% 20%

HURDLE RATE: 15% IRR

BASE CASE: 18.5% IRR → ✓ Clears hurdle with 350bps margin

DOWNSIDE STILL ACCEPTABLE: 12.1% IRR (still positive NPV)

Slide 13: Pro Forma Financial Impact

PRO FORMA P&L (YEAR 2)

($M) Acquirer Target Synergies Pro Forma % Change

─────────────── ──────── ────── ───────── ───────── ────────

Revenue $2,000 $500 $50 $2,550 +27.5%

EBITDA $400 $100 $110 $610 +52.5%

EBITDA Margin 20.0% 20.0% - 23.9% +390bps

BALANCE SHEET IMPACT

Metric Pre-Deal Post-Deal Target Achieved by

────────────────── ──────── ───────── ────── ─────────────

Net Debt/EBITDA 1.3x 2.8x <3.0x Day 1 ✓

EBITDA/Interest 12.0x 8.5x >5.0x Day 1 ✓

Projected Year 3 1.3x 1.8x <2.0x Month 36 ✓

CREDIT RATING: Maintain BBB (per rating agency pre-wire)

Slide 14: Sensitivity Analysis

IRR SENSITIVITY TO KEY ASSUMPTIONS

-20% -10% Base +10% +20%

──────────────── ──────── ──────── ────── ──────── ────────

Revenue Growth 14.2% 16.1% 18.5% 20.7% 23.1%

Synergy Capture 12.8% 15.8% 18.5% 21.0% 23.2%

Exit Multiple 15.1% 16.9% 18.5% 19.8% 21.0%

Integration Costs 19.8% 19.1% 18.5% 17.9% 17.2%

KEY INSIGHTS:

• Most sensitive to revenue growth and synergy capture

• Still >12% IRR even with 20% reduction in key assumptions

• Upside scenario (all +10%) delivers 22%+ IRR

Slide 15: Sources & Uses / Financing

SOURCES & USES OF FUNDS

Sources $M Uses $M

───────────────── ────── ───────────────────── ──────

Cash on Hand $240 Purchase Price $500

New Term Loan $300 Refinance Target Debt $100

Transaction Costs $40

───────────────── ────── ───────────────────── ──────

Total Sources $540 Total Uses $540

FINANCING PLAN

• New 5-year term loan: $300M @ L+275bps

• Pro forma leverage: 2.8x Net Debt/EBITDA

• Committed financing from [Bank Name]

• Deleveraging plan: <2.0x by Year 3 through FCF

• Maintains investment grade rating (BBB)

Slides 16-18: Synergies & Value Creation

Slide 16: Synergy Summary

3-YEAR SYNERGY PLAN

Year 1 Year 2 Year 3 Run-Rate

───────────────────── ─────── ─────── ─────── ─────────

COST SYNERGIES

Headcount Reduction $7M $18M $22M $22M

Procurement Savings $3M $8M $10M $10M

IT Consolidation $1M $2M $3M $3M

Facility Rationalization $0 $3M $5M $5M

────── ─────── ─────── ───────

Total Cost Synergies $11M $31M $40M $40M

REVENUE SYNERGIES

Cross-Sell (Conservative) $3M $8M $15M $15M

────── ─────── ─────── ───────

TOTAL SYNERGIES $14M $39M $55M $55M

PV (3-year, 10% disc): $150M

INTEGRATION COSTS

One-Time Costs $25M $20M $5M $50M

NET VALUE CREATION: $100M NPV

Slide 17: Synergy Detail by Source

| Initiative | Owner | Year 3 Value | Confidence | Key Actions |

|---|---|---|---|---|

| G&A headcount reduction | CFO | $22M | High | Eliminate 150 duplicative roles in Finance, HR, IT, Legal |

| Procurement consolidation | CPO | $10M | High | Renegotiate AWS, Microsoft, Salesforce contracts with combined volume |

| Cross-sell to acquirer customers | CRO | $15M | Medium | Train 500 AEs, bundle pricing, 15% attach rate on 5K customers |

| Office consolidation | CFO | $5M | Medium | Close 3 of 5 target offices, relocate to acquirer facilities |

| IT systems migration | CIO | $3M | High | Migrate target to acquirer AWS, consolidate monitoring/security tools |

Slide 18: Value Creation Bridge

VALUE CREATION WATERFALL

$600M │ ┌─────┐

│ │ │

$500M │ ┌─────┐ │ Pro │

│ │ │ ╱╲ │Forma│

$400M │ ┌─────┐ │Total│ ╱ ╲ │Value│

│ │Stand│ ╱╲ ╱╲ │Value│ ╱Intg.\ │ │

$300M │ │alone│ ╱ ╲╱ ╲ │ │╱Costs ╲ │ │

│ │Value│ ╱Cost Rev.╲│ + │- │ │ │

$200M │ │ │╱Syn Syn. ││Other│ $50M │ │ │

│ │ │ $120 $80 ││ $50M│ │ │ │

$100M │ │$400M│ M M │└─────┘ └────└─────┘

└─────┴─────┴───────────┘

│ │

└──────────────────────────────┘

$200M Value Added

Less: Purchase Price -$500M

═════════════════════════════

NET VALUE CREATION: $100M

Slides 19-20: Integration & Execution

Slide 19: Integration Approach

100-DAY INTEGRATION PLAN

DAY 1-30: STABILIZE

✓ Integration governance launched (Steering Committee, IMO)

✓ Day 1 communications (employees, customers, partners)

✓ Retention packages for 50 critical employees

✓ Quick wins: Procurement contracts, system decommissions

DAY 31-60: EXECUTE CORE SYNERGIES

✓ Headcount decisions communicated

✓ IT migration plan finalized

✓ Office consolidation announced

✓ Sales training on combined portfolio begins

DAY 61-100: SCALE VALUE CAPTURE

✓ Headcount reductions effective

✓ IT migrations Wave 1 complete

✓ Cross-sell pilot launched (20 customers)

✓ Monthly synergy tracking operational

YEAR 1 TARGET: $14M synergies realized, 30% of run-rate

Slide 20: Integration Governance

INTEGRATION ORGANIZATION

┌─────────────────────────────────────────┐

│ Steering Committee │

│ CEO, CFO, COO (Monthly Reviews) │

└─────────────────────────────────────────┘

│

┌─────────────────────────────────────────┐

│ Integration Management Office │

│ VP Integration (Dedicated FTE Year 1) │

│ 5-person IMO team │

└─────────────────────────────────────────┘

│

┌─────────────┴─────────────┬─────────────────┐

│ │ │

┌─────────┐ ┌─────────┐ ┌─────────┐

│Finance &│ │ Sales &│ │IT & Ops │

│ G&A │ │ Revenue │ │ │

│Workstream│ │Workstream│ │Workstream│

└─────────┘ └─────────┘ └─────────┘

DEDICATED RESOURCES: 1 VP + 5 FTE IMO + 15 FTE workstreams

EXTERNAL SUPPORT: [Consulting Firm] for IT migration

Slides 21-22: Risk Assessment

Slide 21: Key Risks & Mitigations

| Risk | Probability | Impact | Mitigation | Residual Risk |

|---|---|---|---|---|

| Customer attrition due to integration uncertainty | Medium | High | • Early customer communications • Retention bonuses for account teams • Executive customer calls |

Medium |

| Talent loss of critical engineers/PMs | Medium | High | • Retention packages for top 50 employees • Clear career paths • Acquirer equity grants |

Low |

| Revenue synergies take longer than expected | High | Medium | • Base case excludes revenue synergies • Deal justified on cost synergies alone |

Low |

| Integration costs exceed budget | Medium | Medium | • 20% contingency in $50M budget • Phased approach to delay non-critical items |

Low |

| Regulatory delay (if applicable) | Low | Medium | • Pre-filed with FTC • Expect 3-month review, standard clearance |

Low |

Slide 22: Downside Scenario Analysis

STRESS TEST: DOWNSIDE SCENARIO

Assumptions (Pessimistic):

• Revenue: 20% below base case (market downturn, customer losses)

• Synergies: Only 50% realized (execution challenges)

• Integration Costs: 2x budget ($100M vs. $50M)

• Timeline: Delayed by 6 months

Downside Results:

┌──────────────────────┬───────────┬────────────┐

│ Metric │ Base Case │ Downside │

├──────────────────────┼───────────┼────────────┤

│ IRR │ 18.5% │ 12.1% │ ← Still >12%

│ NPV │ $120M │ $40M │ ← Still positive

│ EPS Accretion (Y2) │ 8.5% │ 3.2% │ ← Still accretive

│ Net Debt/EBITDA (Y1) │ 2.8x │ 3.2x │ ← Within covenant

└──────────────────────┴───────────┴────────────┘

✓ DOWNSIDE STILL ACCEPTABLE: Positive NPV, >12% IRR, manageable leverage

Slide 23: Recommendation

The Ask

┌────────────────────────────────────────────────────────┐

│ │

│ RECOMMENDATION │

│ │

│ ✓ APPROVE acquisition of [Target Name] for $500M │

│ │

│ RATIONALE: │

│ 1. Strategically aligned: Provides critical cloud │

│ security capability, 2-3 year time-to-market │

│ advantage vs. organic build │

│ │

│ 2. Financially attractive: 18.5% IRR vs. 15% hurdle, │

│ $120M NPV, 8.5% EPS accretive by Year 2 │

│ │

│ 3. Manageable risk: Downside scenario still delivers │

│ 12.1% IRR and positive NPV │

│ │

│ 4. Executable: Detailed integration plan, proven │

│ team, committed financing │

│ │

│ NEXT STEPS: │

│ • Execute Letter of Intent (Week of [Date]) │

│ • 60-day exclusivity period for confirmatory DD │

│ • Return to IC for binding offer approval │

│ • Target close: [Q/Year] │

│ │

└────────────────────────────────────────────────────────┘

Alternative Format (Traffic Light)

Deal meets all IC approval criteria:

🟢 Strategic Fit: Aligned with cloud security priority

🟢 Financial Returns: 18.5% IRR, clears 15% hurdle

🟢 Risk: Downside manageable, mitigations in place

🟢 Execution: Detailed plan, dedicated resources

🟢 Financing: Committed, maintains IG rating

Recommend proceeding to LOI execution.

Appendix (10-20 Slides)

Essential Backup Slides

Include detailed supporting analysis for Q&A:

- Detailed Financial Model (P&L, BS, CF projections)

- Synergy Detail by Initiative (bottoms-up build)

- Comparable Company Analysis (with metrics table)

- Precedent Transaction Analysis (with multiples)

- Management Team Bios (Target leadership)

- Customer Analysis (top customers, concentration, NRR)

- Product Roadmap (integration plans)

- Technology Stack (compatibility assessment)

- Competitive Landscape (positioning map)

- Market Research (TAM methodology, growth drivers)

- Legal/Regulatory (key contract terms, approval timeline)

- Tax Structure (338(h)(10) vs. stock deal implications)

- Transaction Timeline (key milestones and gates)

- Use of Proceeds (if target has debt or preferred)

- Employee Census (headcount by function, retention risk)

Preparation & Delivery

Pre-Meeting Preparation

2 Weeks Before

- Draft IC deck (complete with appendix)

- Internal review with Corp Dev team

- CFO review of financial analysis

- Legal review of transaction structure

- Identify potential objections

1 Week Before

- Pre-wire with IC members individually

- Incorporate feedback into deck

- Prepare Q&A document (50+ potential questions)

- Practice presentation (30 min main + 30 min Q&A)

- Finalize recommendation and ask

Day Before

- Final deck review and polish

- Send deck to IC 24 hours in advance

- Confirm attendees and logistics

- Prepare backup materials

Pre-Wiring Strategy

Why Pre-Wire?

Pre-wiring = meeting with IC members 1-on-1 before formal presentation to:

- Gauge support and identify concerns

- Incorporate feedback before the meeting

- Build consensus and avoid surprises

- Tailor presentation to address specific concerns

Never go into an IC meeting "cold." Pre-wire with key stakeholders (CFO, CEO, board members) to understand their perspectives and address concerns proactively. Deals with strong pre-wiring support have 3x higher approval rates.

Pre-Wire Template

MEETING: 30-45 minutes with [Name]

OBJECTIVES:

1. Get early feedback on strategic rationale

2. Understand financial return expectations

3. Identify concerns or objections

4. Secure support (or know where resistance is)

KEY DISCUSSION POINTS:

• Strategic fit with corporate priorities

• Financial returns (IRR, NPV, EPS impact)

• Key risks and how we're mitigating

• Integration confidence

QUESTIONS TO ASK:

• "What's your initial reaction to this opportunity?"

• "What would make you most confident in approving this?"

• "What concerns should we address in the IC presentation?"

• "Are there specific analyses you'd like to see?"

OUTCOME:

✓ Supporter / ? Neutral / ✗ Skeptic

Key concerns: [list]

Action items: [what to add/change in deck]

Presentation Delivery Tips

Structure Your Talk Track

Slide 1 (Executive Summary): 2-3 min

- "This is a $500M acquisition of [Target], a market-leading cloud security platform."

- "Strategically, this addresses our #1 priority of entering cloud security."

- "Financially, it delivers 18.5% IRR, well above our 15% hurdle."

- "We're recommending approval to proceed to LOI."

Slides 2-5 (Strategic Rationale): 5-7 min

- Tell the strategic story clearly and concisely

- Connect to stated corporate priorities

- Explain why this target and why now

Slides 6-8 (Target Overview): 3-4 min

- Describe what the company does and why it's attractive

- Highlight key metrics and competitive position

Slides 9-10 (Market): 2-3 min

- Set context on market size and growth

- Briefly cover tailwinds supporting the investment

Slides 11-15 (Financials): 8-10 min

- Walk through valuation, returns, and financial impact

- Be prepared for deep-dive questions here

- Show sensitivity and downside scenarios

Slides 16-18 (Synergies): 5-6 min

- Detail how value will be created

- Be specific about sources and timelines

- Address integration complexity head-on

Slides 19-20 (Integration): 3-4 min

- Show you have a detailed plan

- Highlight governance and resources

Slides 21-22 (Risks): 4-5 min

- Don't shy away from risks

- Show thoughtful mitigations

- Demonstrate downside is still acceptable

Slide 23 (Recommendation): 2 min

- Restate the ask clearly

- Summarize key reasons to approve

- Outline next steps

Total Presentation: 35-45 minutes + 15-30 min Q&A

Delivery Best Practices

✓ Start strong: Open with clear recommendation and executive summary

✓ Tell a story: Connect strategic rationale → financial returns → value creation

✓ Use data: Specific numbers, not hand-waving

✓ Be balanced: Acknowledge risks, don't oversell

✓ Show conviction: Clearly state recommendation and stand behind it

✓ Anticipate questions: Have answers ready (practice Q&A)

✓ Respect time: Stay on schedule, use appendix for detail

✓ Visual clarity: Use charts/graphs, minimize text

✗ Avoid:

- Reading slides verbatim

- Too much detail in main deck (use appendix)

- Hedging on recommendation

- Defensive tone when discussing risks

- Ignoring feedback or questions

- Going over time limit

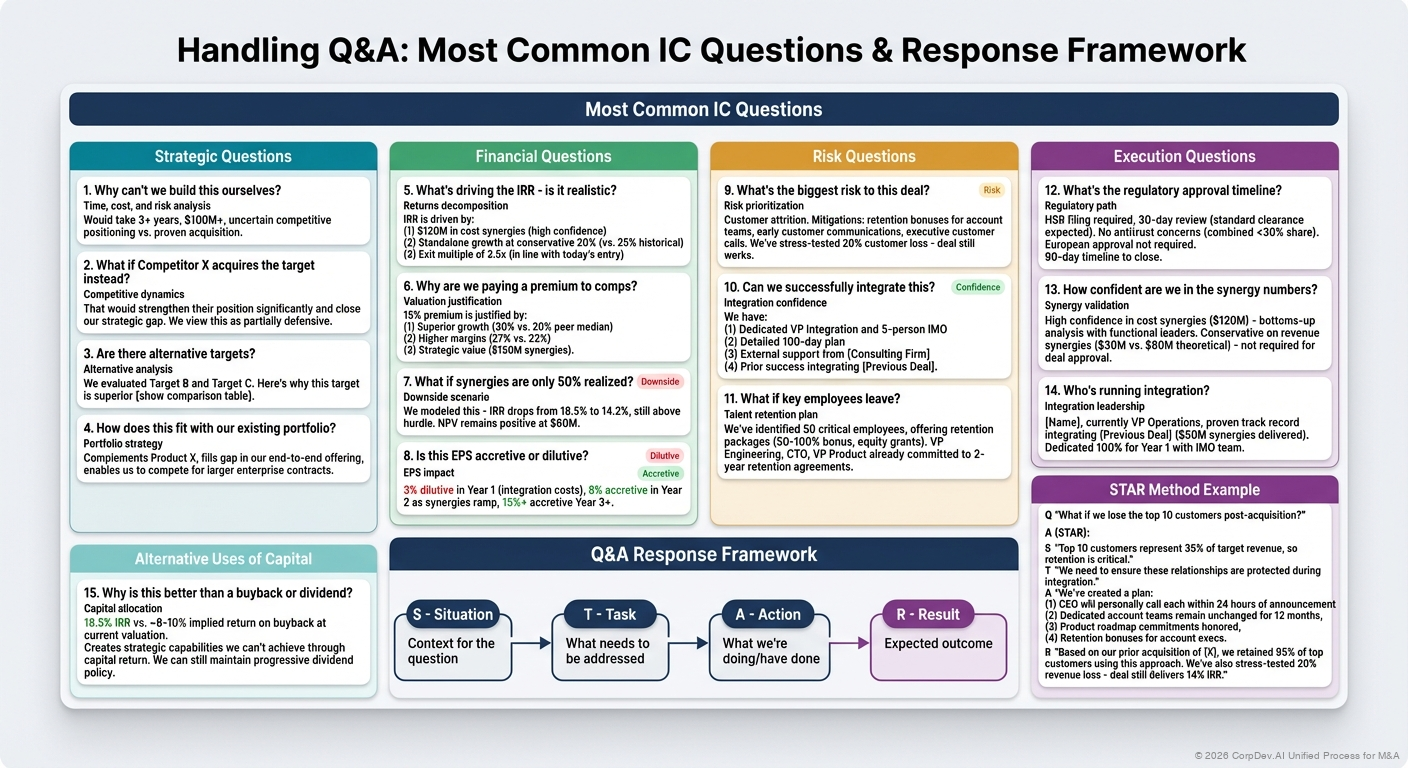

Handling Q&A

Most Common IC Questions

Strategic Questions

"Why can't we build this ourselves?"

- Answer: Time, cost, and risk analysis. "Would take 3+ years, $100M+, uncertain competitive positioning vs. proven acquisition."

"What if Competitor X acquires the target instead?"

- Answer: Competitive dynamics. "That would strengthen their position significantly and close our strategic gap. We view this as partially defensive."

"Are there alternative targets?"

- Answer: Alternative analysis. "We evaluated Target B and Target C. Here's why this target is superior [show comparison table]."

"How does this fit with our existing portfolio?"

- Answer: Portfolio strategy. "Complements Product X, fills gap in our end-to-end offering, enables us to compete for larger enterprise contracts."

Financial Questions

"What's driving the IRR - is it realistic?"

- Answer: Returns decomposition. "IRR is driven by: (1) $120M in cost synergies (high confidence), (2) Standalone growth at conservative 20% (vs. 25% historical), (3) Exit multiple of 3.5x (in line with today's entry)."

"Why are we paying a premium to comps?"

- Answer: Valuation justification. "15% premium is justified by: (1) Superior growth (30% vs. 20% peer median), (2) Higher margins (27% vs. 22%), (3) Strategic value ($150M synergies)."

"What if synergies are only 50% realized?"

- Answer: Downside scenario. "We modeled this - IRR drops from 18.5% to 14.2%, still above hurdle. NPV remains positive at $60M."

"Is this EPS accretive or dilutive?"

- Answer: EPS impact. "3% dilutive in Year 1 (integration costs), 8% accretive in Year 2 as synergies ramp, 15%+ accretive Year 3+."

Risk Questions

"What's the biggest risk to this deal?"

- Answer: Risk prioritization. "Customer attrition. Mitigations: retention bonuses for account teams, early customer communications, executive customer calls. We've stress-tested 20% customer loss - deal still works."

"Can we successfully integrate this?"

- Answer: Integration confidence. "We have: (1) Dedicated VP Integration and 5-person IMO, (2) Detailed 100-day plan, (3) External support from [Consulting Firm], (4) Prior success integrating [Previous Deal]."

"What if key employees leave?"

- Answer: Talent retention plan. "We've identified 50 critical employees, offering retention packages (50-100% bonus, equity grants). VP Engineering, CTO, VP Product already committed to 2-year retention agreements."

Execution Questions

"What's the regulatory approval timeline?"

- Answer: Regulatory path. "HSR filing required, 30-day review (standard clearance expected). No antitrust concerns (combined <30% share). European approval not required. 90-day timeline to close."

"How confident are we in the synergy numbers?"

- Answer: Synergy validation. "High confidence in cost synergies ($120M) - bottoms-up analysis with functional leaders. Conservative on revenue synergies ($30M vs. $80M theoretical) - not required for deal approval."

"Who's running integration?"

- Answer: Integration leadership. "[Name], currently VP Operations, proven track record integrating [Previous Deal] ($50M synergies delivered). Dedicated 100% for Year 1 with IMO team."

Alternative Uses of Capital

- "Why is this better than a buyback or dividend?"

- Answer: Capital allocation. "18.5% IRR vs. ~8-10% implied return on buyback at current valuation. Creates strategic capabilities we can't achieve through capital return. We can still maintain progressive dividend policy."

Q&A Response Framework

STAR Method

- Situation: Context for the question

- Task: What needs to be addressed

- Action: What we're doing/have done

- Result: Expected outcome

Example:

Q: "What if we lose the top 10 customers post-acquisition?"

A (STAR):

- Situation: "Top 10 customers represent 35% of target revenue, so retention is critical."

- Task: "We need to ensure these relationships are protected during integration."

- Action: "We've created a plan: (1) CEO will personally call each within 24 hours of announcement, (2) Dedicated account teams remain unchanged for 12 months, (3) Product roadmap commitments honored, (4) Retention bonuses for account execs."

- Result: "Based on our prior acquisition of [X], we retained 95% of top customers using this approach. We've also stress-tested 20% revenue loss - deal still delivers 14% IRR."

IC Presentation Checklist

Content Checklist

- Executive summary clearly states recommendation and key metrics

- Strategic rationale connects to corporate priorities

- Why this target articulated vs. alternatives

- Market opportunity sized and validated

- Financial returns show IRR, NPV, payback, and EPS impact

- Valuation benchmarked against multiple methodologies

- Sensitivity analysis shows range of outcomes

- Downside scenario demonstrates acceptable risk

- Synergies detailed by source with ownership

- Integration plan outlines 100-day plan and governance

- Risk assessment identifies top risks with mitigations

- Financing plan includes sources/uses and credit impact

- Recommendation is clear and actionable

- Appendix has detailed backup for all analyses

Preparation Checklist

- Pre-wired with CFO, CEO, and key IC members

- Incorporated feedback from pre-wires into deck

- Prepared Q&A document with 50+ questions

- Practiced presentation (timed, under 45 min)

- Identified potential objections and prepared responses

- Financial model reviewed by CFO and finance team

- Legal review of transaction structure complete

- Deck sent to IC 24+ hours in advance

- Backup materials ready (detailed model, comps, etc.)

- Attendee list confirmed

Delivery Checklist

- Start with clear recommendation

- Tell compelling strategic story

- Use visuals effectively (charts, not walls of text)

- Stay on time (respect the agenda)

- Acknowledge risks honestly

- Demonstrate conviction in recommendation

- Answer questions directly and confidently

- Use appendix for detailed answers

- Summarize next steps if approved

- Follow up with action items and timeline

Example IC Presentation Outline

Acquisition of CloudSecure Inc.

EXECUTIVE SUMMARY

- Target: CloudSecure, market-leading cloud security platform

- Price: $500M (3.5x Revenue, 11.5x EBITDA)

- Returns: 18.5% IRR, $120M NPV, 8.5% EPS accretive Year 2

- Strategic: Addresses #1 priority (cloud security capability)

- Recommendation: ✓ APPROVE

STRATEGIC RATIONALE (4 slides)

- Our strategic priorities → How this deal addresses them

- Why this target (vs. build or alternatives)

- Why now (market timing, competitive dynamics)

- Post-deal competitive positioning (#3 → #1 player)

TARGET OVERVIEW (3 slides)

- Company profile: $140M revenue, 85% SaaS, 650 enterprise customers

- Financial performance: 28% growth, 27% EBITDA margin, 95% NRR

- Strengths & weaknesses matrix

MARKET OPPORTUNITY (2 slides)

- TAM: $18B → $42B by 2027 (15% CAGR)

- Tailwinds: Cloud migration, regulatory requirements, consolidation preference

FINANCIAL ANALYSIS (5 slides)

- Valuation: $500M fair value (DCF, comps, precedents)

- Returns: 18.5% IRR base (24% upside, 12% downside)

- Pro forma impact: 27% revenue growth, 390bps EBITDA margin expansion

- Sensitivity: Revenue growth and synergy capture most impactful

- Financing: $240M cash + $300M debt, 2.8x leverage, maintains BBB rating

SYNERGIES & VALUE CREATION (3 slides)

- Synergy summary: $150M PV ($120M cost, $30M revenue)

- Initiative detail: Headcount, procurement, cross-sell, IT, facilities

- Value bridge: $100M NPV after $500M purchase price

INTEGRATION (2 slides)

- 100-day plan: Stabilize → Execute → Scale

- Governance: Steering Committee, dedicated VP Integration + IMO

RISKS (2 slides)

- Key risks: Customer attrition, talent loss, revenue synergy timing

- Downside scenario: Still delivers 12.1% IRR, positive NPV, manageable leverage

RECOMMENDATION (1 slide)

- ✓ APPROVE - strategically aligned, financially attractive, executable

- Next steps: Execute LOI, 60-day exclusivity, return for binding offer approval

APPENDIX (15 slides)

- Detailed financial model, synergy bottoms-up, comps analysis, precedents, management bios, customer analysis, tech stack, competitive landscape, etc.

Key Takeaways

- IC presentation is a story, not just data - connect strategic rationale to financial returns to value creation

- Executive summary is critical - must stand alone as one-page deal overview

- Pre-wiring matters - never present cold, build consensus before formal meeting

- Be balanced - acknowledge risks honestly, show you've thought through mitigations

- Downside must be acceptable - show even pessimistic scenario delivers acceptable returns

- Synergies need detail - source-by-source build-up with ownership and timelines

- Clear recommendation - don't hedge, state what you're asking for and why

- Prepare for Q&A - anticipate 50+ questions, practice responses

- Use appendix - keep main deck concise, use backup for detail

- Visual > text - charts and graphs, not walls of bullets

The IC presentation is your opportunity to secure approval for a transaction you believe creates value. Prepare thoroughly, pre-wire key stakeholders, tell a compelling story with data, acknowledge risks honestly, and make a clear recommendation. A great IC presentation demonstrates strategic thinking, financial rigor, and execution confidence.

Related Resources

- Deal Thesis Overview - Building the complete deal thesis

- Strategic Rationale - Articulating strategic logic

- Business Case Development - Financial justification and ROI

- Value Creation Planning - Synergy identification and capture

- M&A Negotiation Strategies - Getting to agreed terms

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Thu Oct 30 2025 20:00:00 GMT-0400 (Eastern Daylight Time)