Divestitures & Carve-Outs Overview

While M&A often focuses on acquisitions, divestitures—the sale or spin-off of business units—are equally strategic and complex. Well-executed divestitures unlock shareholder value, improve focus, and provide capital for reinvestment in core businesses.

Market Overview

$800B+

Annual global divestiture volume

30-35%

Share of total M&A activity

25%

Average stock price increase post-announcement

18-24mo

Typical timeline for complex carve-out

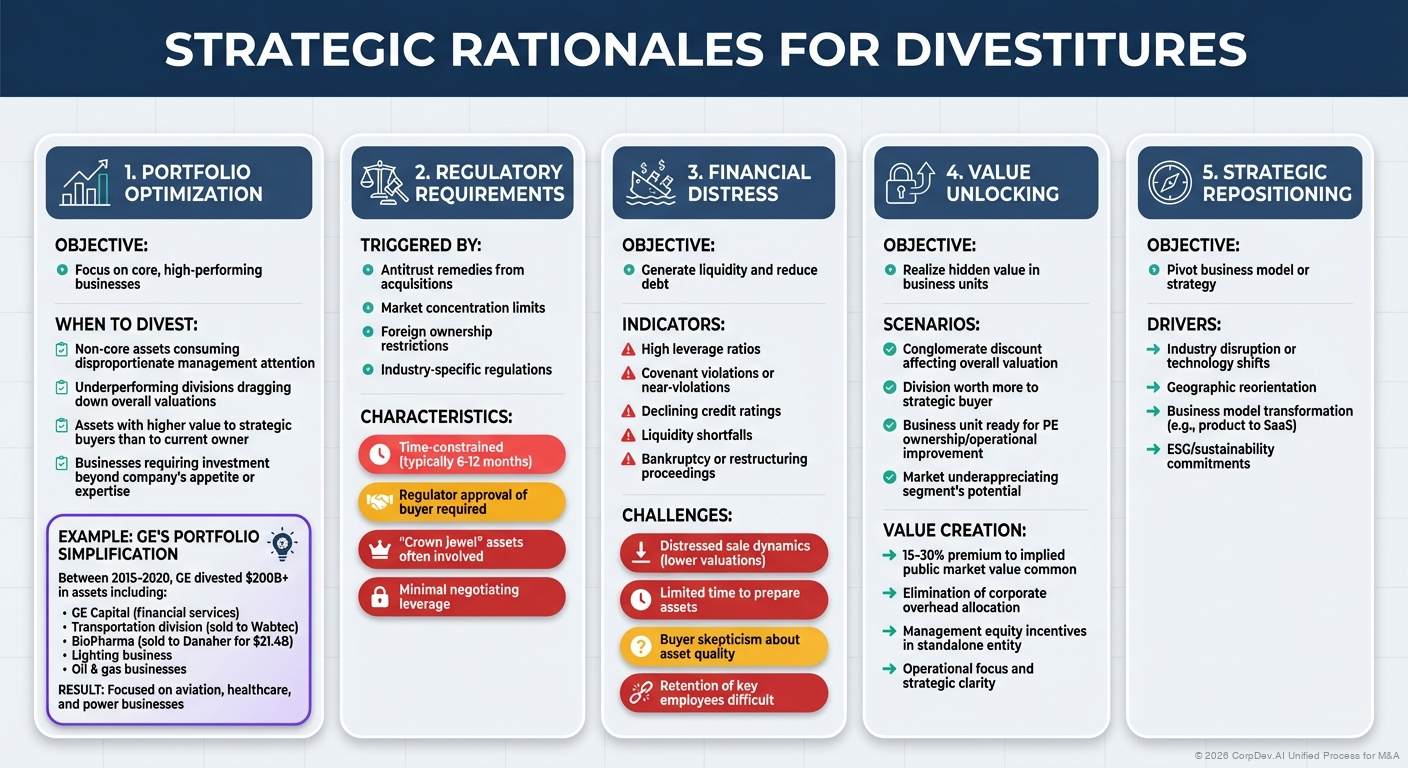

Strategic Rationales for Divestitures

1. Portfolio Optimization

Objective: Focus on core, high-performing businesses

When to Divest:

- Non-core assets consuming disproportionate management attention

- Underperforming divisions dragging down overall valuations

- Assets with higher value to strategic buyers than to current owner

- Businesses requiring investment beyond company's appetite or expertise

Example: GE's Portfolio Simplification

Between 2015-2020, GE divested $200B+ in assets including:

- GE Capital (financial services)

- Transportation division (sold to Wabtec)

- BioPharma (sold to Danaher for $21.4B)

- Lighting business

- Oil & gas businesses

Result: Focused on aviation, healthcare, and power businesses

2. Regulatory Requirements

Triggered By:

- Antitrust remedies from acquisitions

- Market concentration limits

- Foreign ownership restrictions

- Industry-specific regulations

Characteristics:

- Time-constrained (typically 6-12 months)

- Regulator approval of buyer required

- "Crown jewel" assets often involved

- Minimal negotiating leverage

3. Financial Distress

Objective: Generate liquidity and reduce debt

Indicators:

- High leverage ratios

- Covenant violations or near-violations

- Declining credit ratings

- Liquidity shortfalls

- Bankruptcy or restructuring proceedings

Challenges:

- Distressed sale dynamics (lower valuations)

- Limited time to prepare assets

- Buyer skepticism about asset quality

- Retention of key employees difficult

4. Value Unlocking

Objective: Realize hidden value in business units

Scenarios:

- Conglomerate discount affecting overall valuation

- Division worth more to strategic buyer

- Business unit ready for PE ownership/operational improvement

- Market underappreciating segment's potential

Value Creation:

- 15-30% premium to implied public market value common

- Elimination of corporate overhead allocation

- Management equity incentives in standalone entity

- Operational focus and strategic clarity

5. Strategic Repositioning

Objective: Pivot business model or strategy

Drivers:

- Industry disruption or technology shifts

- Geographic reorientation

- Business model transformation (e.g., product to SaaS)

- ESG/sustainability commitments

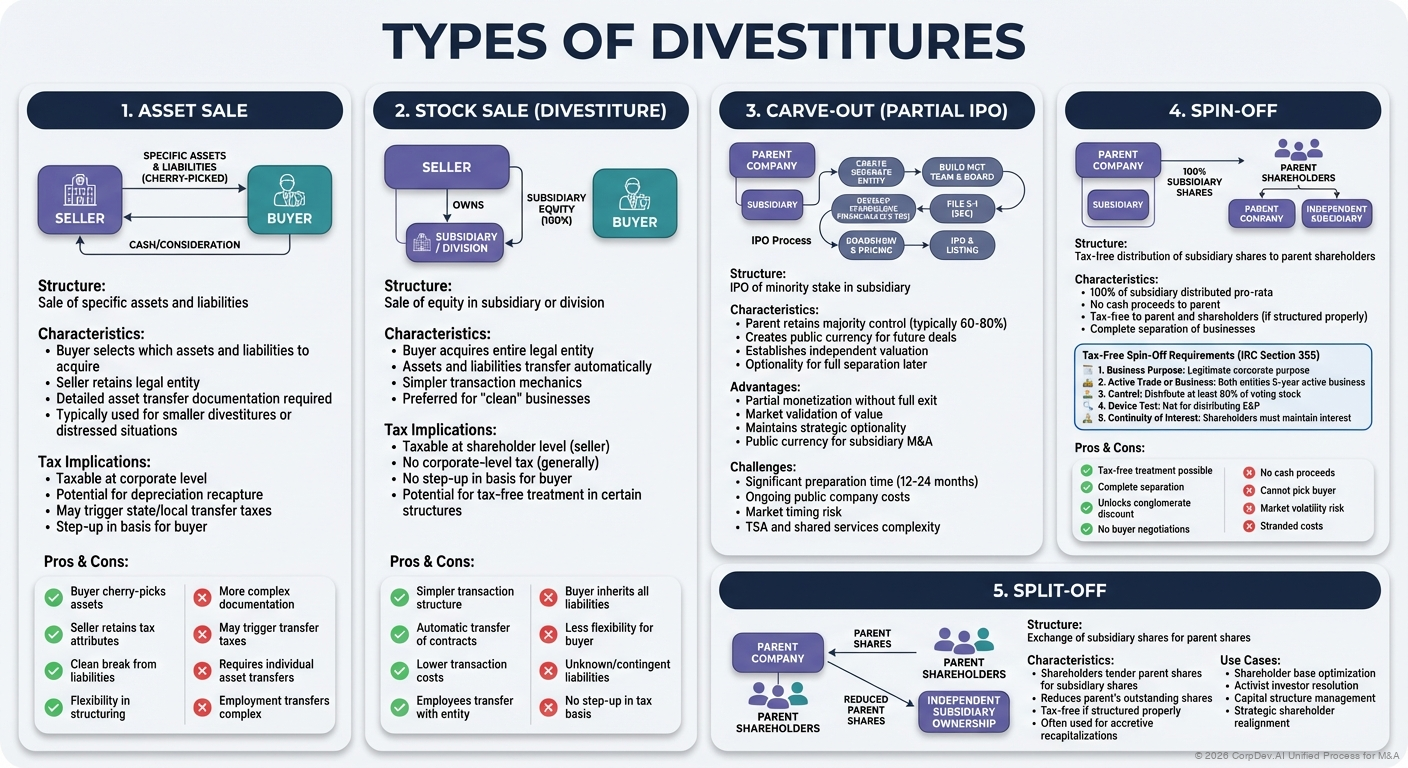

Types of Divestitures

1. Asset Sale

Structure: Sale of specific assets and liabilities

Characteristics:

- Buyer selects which assets and liabilities to acquire

- Seller retains legal entity

- Detailed asset transfer documentation required

- Typically used for smaller divestitures or distressed situations

Tax Implications:

- Taxable at corporate level

- Potential for depreciation recapture

- May trigger state/local transfer taxes

- Step-up in basis for buyer

Pros & Cons:

| Pros | Cons |

|---|---|

| Buyer cherry-picks assets | More complex documentation |

| Seller retains tax attributes | May trigger transfer taxes |

| Clean break from liabilities | Requires individual asset transfers |

| Flexibility in structuring | Employment transfers complex |

2. Stock Sale (Divestiture)

Structure: Sale of equity in subsidiary or division

Characteristics:

- Buyer acquires entire legal entity

- Assets and liabilities transfer automatically

- Simpler transaction mechanics

- Preferred for "clean" businesses

Tax Implications:

- Taxable at shareholder level (seller)

- No corporate-level tax (generally)

- No step-up in basis for buyer

- Potential for tax-free treatment in certain structures

Pros & Cons:

| Pros | Cons |

|---|---|

| Simpler transaction structure | Buyer inherits all liabilities |

| Automatic transfer of contracts | Less flexibility for buyer |

| Lower transaction costs | Unknown/contingent liabilities |

| Employees transfer with entity | No step-up in tax basis |

3. Carve-Out (Partial IPO)

Structure: IPO of minority stake in subsidiary

Characteristics:

- Parent retains majority control (typically 60-80%)

- Creates public currency for future deals

- Establishes independent valuation

- Optionality for full separation later

Process:

- Create separate legal entity (if not already)

- Develop standalone financials (2-3 years)

- Build management team and board

- File S-1 registration with SEC

- Roadshow and pricing

- IPO and listing

Advantages:

- Partial monetization without full exit

- Market validation of value

- Maintains strategic optionality

- Public currency for subsidiary M&A

Challenges:

- Significant preparation time (12-24 months)

- Ongoing public company costs

- Market timing risk

- TSA and shared services complexity

4. Spin-Off

Structure: Tax-free distribution of subsidiary shares to parent shareholders

Characteristics:

- 100% of subsidiary distributed pro-rata

- No cash proceeds to parent

- Tax-free to parent and shareholders (if structured properly)

- Complete separation of businesses

IRS Requirements for Tax-Free Treatment:

- Business purpose (not primarily tax avoidance)

- 5-year active trade or business

- 80% distribution requirement

- Continuity of interest

- Device test (not primarily for E&P distribution)

Pros & Cons:

| Pros | Cons |

|---|---|

| Tax-free treatment possible | No cash proceeds |

| Complete separation | Cannot pick buyer |

| Unlocks conglomerate discount | Market volatility risk |

| No buyer negotiations | Stranded costs |

Tax-Free Spin-Off Requirements:

To qualify for tax-free treatment under IRC Section 355:

- Business Purpose: Must serve legitimate corporate business purpose

- Active Trade or Business: Both parent and spun-off entity must conduct 5-year active businesses

- Control: Parent must distribute at least 80% of voting stock

- Device Test: Not principally a device for distributing E&P

- Continuity of Interest: Shareholders must maintain continuity of interest

5. Split-Off

Structure: Exchange of subsidiary shares for parent shares

Characteristics:

- Shareholders tender parent shares for subsidiary shares

- Reduces parent's outstanding shares

- Tax-free if structured properly

- Often used for accretive recapitalizations

Use Cases:

- Shareholder base optimization

- Activist investor resolution

- Capital structure management

- Strategic shareholder realignment

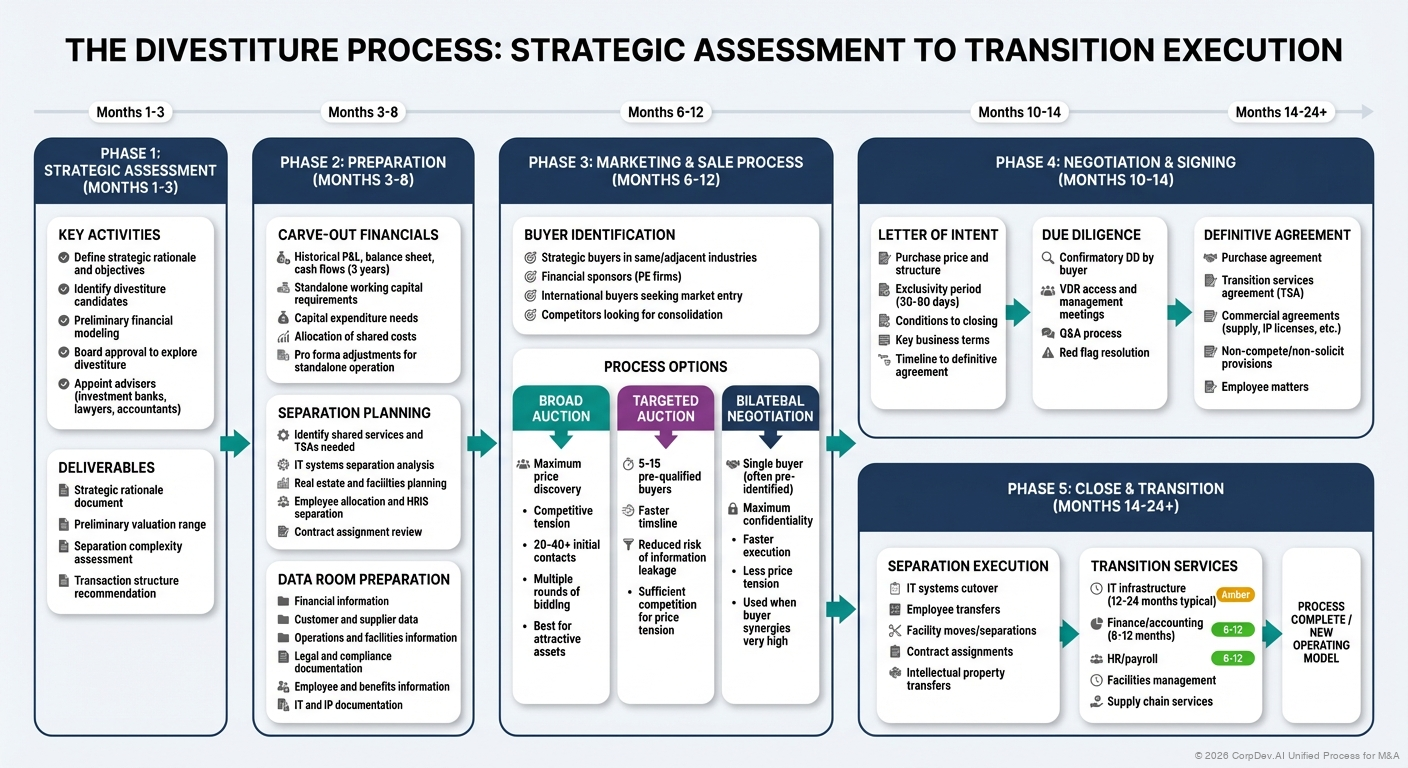

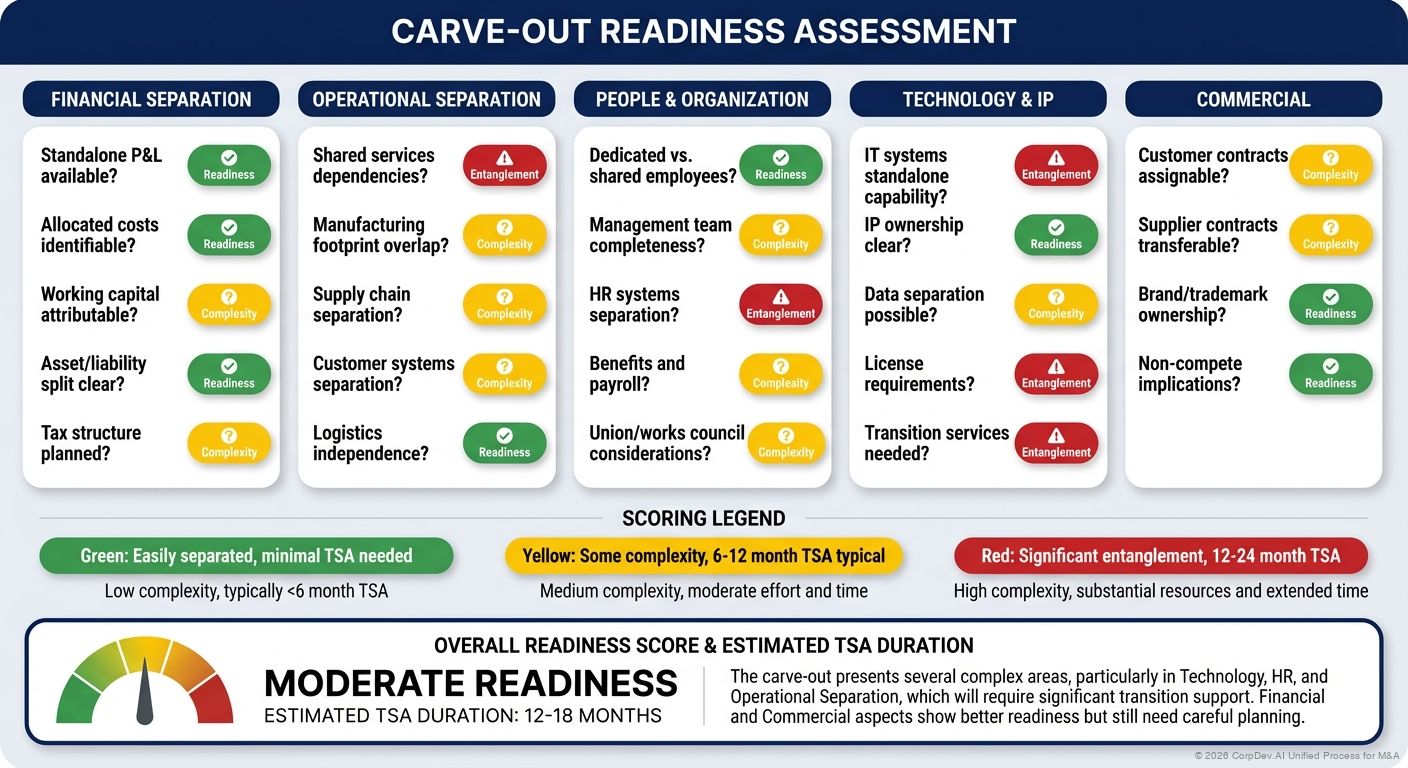

The Divestiture Process

Phase 1: Strategic Assessment (Months 1-3)

Key Activities:

- Define strategic rationale and objectives

- Identify divestiture candidates

- Preliminary financial modeling

- Board approval to explore divestiture

- Appoint advisors (investment banks, lawyers, accountants)

Deliverables:

- Strategic rationale document

- Preliminary valuation range

- Separation complexity assessment

- Transaction structure recommendation

Phase 2: Preparation (Months 3-8)

Carve-Out Financials:

- Historical P&L, balance sheet, cash flows (3 years)

- Standalone working capital requirements

- Capital expenditure needs

- Allocation of shared costs

- Pro forma adjustments for standalone operation

Separation Planning:

- Identify shared services and TSAs needed

- IT systems separation analysis

- Real estate and facilities planning

- Employee allocation and HRIS separation

- Contract assignment review

Data Room Preparation:

- Financial information

- Customer and supplier data

- Operations and facilities information

- Legal and compliance documentation

- Employee and benefits information

- IT and IP documentation

Phase 3: Marketing & Sale Process (Months 6-12)

Buyer Identification:

- Strategic buyers in same/adjacent industries

- Financial sponsors (PE firms)

- International buyers seeking market entry

- Competitors looking for consolidation

Process Options:

Broad Auction:

- Maximum price discovery

- Competitive tension

- 20-40+ initial contacts

- Multiple rounds of bidding

- Best for attractive assets

Targeted Auction:

- 5-15 pre-qualified buyers

- Faster timeline

- Reduced risk of information leakage

- Sufficient competition for price tension

Bilateral Negotiation:

- Single buyer (often pre-identified)

- Maximum confidentiality

- Faster execution

- Less price tension

- Used when buyer synergies very high

Phase 4: Negotiation & Signing (Months 10-14)

Letter of Intent:

- Purchase price and structure

- Exclusivity period (30-90 days)

- Conditions to closing

- Key business terms

- Timeline to definitive agreement

Due Diligence:

- Confirmatory DD by buyer

- VDR access and management meetings

- Q&A process

- Red flag resolution

Definitive Agreement:

- Purchase agreement

- Transition services agreement (TSA)

- Commercial agreements (supply, IP licenses, etc.)

- Non-compete/non-solicit provisions

- Employee matters

Phase 5: Close & Transition (Months 14-24+)

Regulatory Approvals:

- HSR filing and clearance (if applicable)

- Foreign investment approvals

- Industry-specific approvals

Separation Execution:

- IT systems cutover

- Employee transfers

- Facility moves/separations

- Contract assignments

- Intellectual property transfers

Transition Services:

- IT infrastructure (12-24 months typical)

- Finance/accounting (6-12 months)

- HR/payroll (6-12 months)

- Facilities management

- Supply chain services

Critical Success Factors

1. Clean Carve-Out

Financial Separation:

- Standalone financials with clear assumptions

- Reasonable cost allocations (defensible methodology)

- Appropriate working capital levels

- Clean balance sheet (no stranded liabilities)

Operational Separation:

- Minimal dependencies on parent post-close

- Clear service agreements for ongoing needs

- Dedicated management team in place

- Identified and transferable customer relationships

2. Effective Marketing

Positioning:

- Compelling equity story for standalone business

- Clear growth strategy and opportunities

- Credible management team

- Articulated competitive advantages

Materials:

- Professional CIM (Confidential Information Memorandum)

- Management presentation

- Detailed financial model

- Comprehensive data room

3. Process Management

Timeline Management:

- Realistic timeline accounting for complexity

- Built-in buffer for regulatory approvals

- Coordinated internal workstreams

- Clear milestones and accountability

Information Control:

- Confidential process (code names, NDAs)

- Controlled dissemination of information

- Employee communication plan

- Customer/supplier management

4. Valuation Optimization

Value Drivers:

- Demonstrate growth potential

- Highlight margin improvement opportunities

- Showcase competitive moats

- Articulate synergy potential for buyers

Negotiation:

- Create competitive tension among buyers

- Understand buyer-specific value drivers

- Structure deal to maximize after-tax proceeds

- Retain upside through earn-outs if appropriate

Common Pitfalls

1. Stranded Costs

Problem: Costs that cannot be eliminated after divestiture

Examples:

- Corporate overhead with insufficient scale economies

- IT infrastructure committed long-term

- Facilities/real estate with long leases

- Shared services that lose economies of scale

Mitigation:

- Early identification and quantification

- Cost reduction plan for remaining business

- Restructuring charges if needed

- Honest reflection in pro formas

2. TSA Dependency

Problem: Excessive reliance on transition services

Risks:

- Operational disruption if services terminated

- Buyer dissatisfaction with service quality

- Seller distraction supporting sold business

- Underestimated TSA costs

Best Practices:

- Right-size TSA scope and duration

- Charge appropriate fees (at cost or market)

- Build exit plans from day one

- Escalating fees to encourage migration

3. Employee Issues

Challenges:

- Key employee retention through process

- Morale impact from uncertainty

- Benefits and compensation harmonization

- WARN Act and labor law compliance

Solutions:

- Retention bonuses for critical employees

- Clear and timely communication

- Comparable benefits packages

- Employee transfer agreements

4. Inadequate Preparation

Symptoms:

- Incomplete or poor-quality financials

- Lack of standalone cost structure clarity

- Insufficient documentation in data room

- Unprepared management team

Consequences:

- Lower valuations due to buyer uncertainty

- Extended timeline and increased costs

- Deal fatigue and momentum loss

- Potential process failure

Valuation Considerations

Valuation Methods

1. Comparable Company Analysis:

- Identify pure-play public comparables

- Apply sector-appropriate multiples

- Adjust for size, growth, and profitability differences

- Consider liquidity discount if applicable

2. Precedent Transaction Analysis:

- Recent divestitures in sector

- Control premium analysis

- Synergy assumptions from prior deals

- Market condition adjustments

3. DCF Analysis:

- Standalone business plan projections

- Appropriate discount rate (WACC)

- Terminal value assumptions

- Sensitivity analysis on key drivers

Typical Valuation Ranges by Buyer Type

| Buyer Type | Valuation Range | Key Value Drivers |

|---|---|---|

| Strategic Buyer | 6-12x EBITDA | Synergies, market share, vertical integration |

| Private Equity | 5-9x EBITDA | Operational improvements, add-on potential, exit multiple |

| Management Buyout | 4-7x EBITDA | Limited capital, higher leverage, operational expertise |

| International Buyer | 7-12x EBITDA | Market entry, technology access, premium for platform |

Divestiture Discounts

Conglomerate Discount Elimination: 15-25% uplift typical when separating from multi-industry parent

Distressed Sale Discount: 20-40% below fair value for forced/quick sales

Carve-Out Complexity Discount: 5-15% for highly integrated businesses requiring significant separation

Key Takeaways

Essential Points

Strategic Clarity: Divestitures must have clear strategic rationale—portfolio optimization, regulatory requirement, or value unlocking

Preparation Critical: 6-12 months minimum to properly prepare high-quality divestiture; rushed processes yield lower values

Clean Carve-Out: Standalone financials with defensible allocations and minimal parent dependencies command premium valuations

Process Matters: Competitive auction processes typically yield 15-25% higher prices than bilateral negotiations

Tax Structuring: Early tax planning critical; difference between taxable sale and tax-free spin can be significant

TSA Balance: Transition services necessary but should be right-sized; 12-18 months typical with migration plans

Stranded Costs: Identify and plan for costs that cannot be eliminated after divestiture; be transparent with buyers

Employee Retention: Key employee retention through transaction critical; consider retention bonuses and clear communication

Regulatory Timeline: Build 6-12 months for regulatory approvals into timeline for significant divestitures

Value Realization: Well-executed divestitures typically create 25%+ stock price increase as conglomerate discount eliminated

Related Articles:

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: 2025-10-30