Merger Model & Accretion/Dilution Analysis

A merger model is the financial framework that evaluates how an acquisition impacts the acquirer's earnings per share (EPS). This guide covers how to build robust merger models, analyze accretion/dilution, and evaluate different deal structures and financing scenarios.

What is a Merger Model?

Definition: A merger model is a financial model that combines two companies' financial statements to analyze the impact of an acquisition on the acquirer's pro forma earnings, particularly EPS accretion or dilution.

Core Purpose: Determine whether the transaction is accretive (increases EPS) or dilutive (decreases EPS) to the acquirer's shareholders.

Key Outputs:

- Pro Forma Income Statement - Combined company financials

- Sources & Uses - Deal financing structure

- EPS Impact - Accretion/dilution analysis

- Returns Analysis - IRR and ROIC

- Credit Metrics - Leverage ratios and coverage

While DCF analysis determines what you should pay based on intrinsic value, a merger model tells you what you can pay while maintaining earnings accretion. These are complementary but distinct analyses.

When to Use Merger Models

Use merger models when:

- Evaluating public company acquisitions

- Acquirer's stock is the primary currency

- Board/shareholders care about EPS impact

- Analyzing alternative financing structures

- Negotiating purchase price and terms

- Modeling earnouts or contingent payments

Critical for:

- Public company M&A

- Large strategic acquisitions

- Stock-heavy deal structures

- Transactions requiring shareholder approval

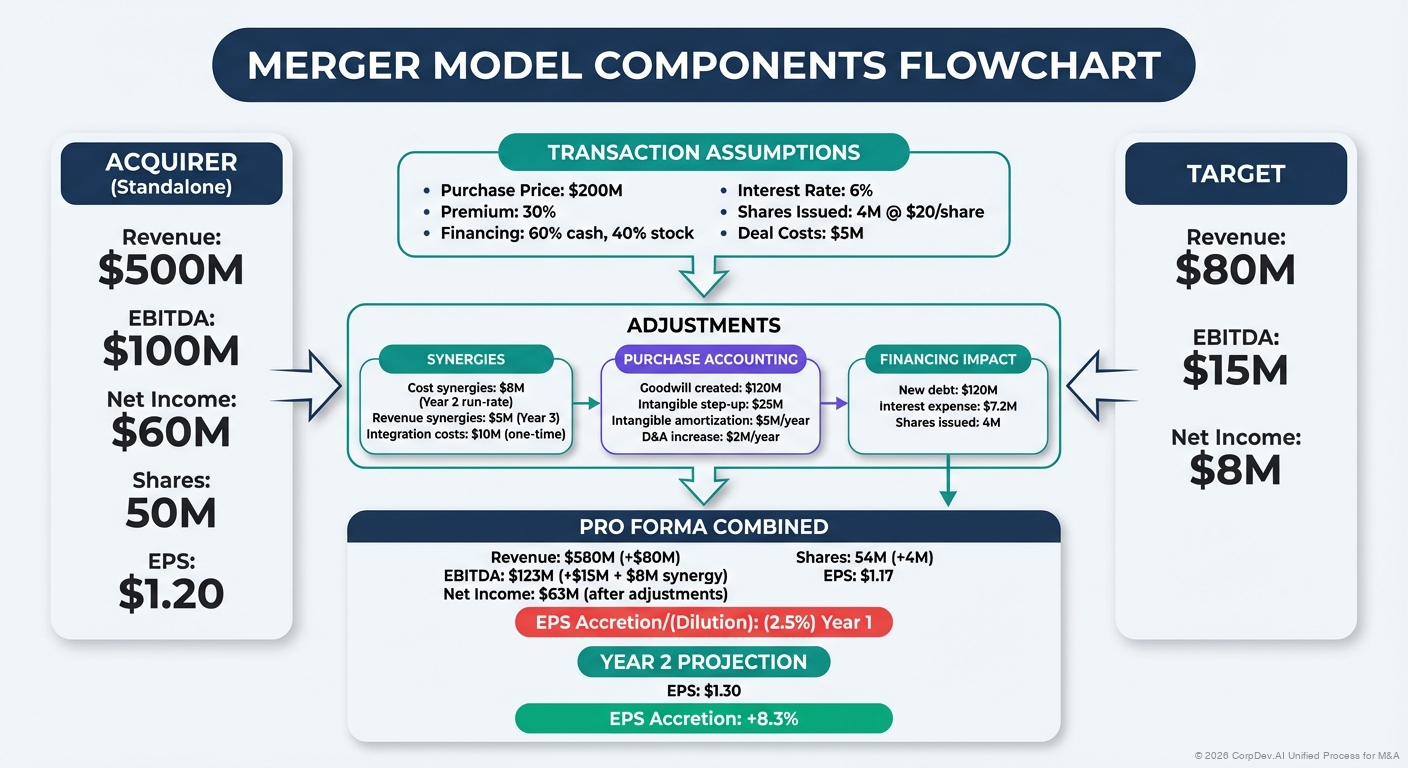

Merger Model Components

1. The Three Core Sections

Sources & Uses

Transaction Financing

How will the deal be funded? Cash, stock, debt, or combination? Includes purchase price allocation and transaction costs.

Pro Forma Financials

Combined Company

Consolidated income statement, balance sheet, and cash flow statement reflecting the combined entity with purchase accounting adjustments.

Accretion/Dilution

EPS Impact Analysis

Calculate standalone vs. pro forma EPS to determine if the deal is accretive (increases EPS) or dilutive (decreases EPS).

2. Key Assumptions

Every merger model requires:

Transaction Assumptions:

- Purchase price and structure

- Form of consideration (cash, stock, mix)

- Transaction and financing costs

- Expected closing date

- Purchase price allocation

Operating Assumptions:

- Standalone financial projections for both companies

- Revenue synergies (if any)

- Cost synergies and timing

- Integration costs

- Tax rate and structure

Financing Assumptions:

- Debt capacity and terms

- Interest rates and amortization

- Stock price for acquirer

- Exchange ratio (if stock deal)

- New share issuance

Step-by-Step Merger Model Construction

Step 1: Gather Financial Information

For Acquirer:

- Historical financial statements (3-5 years)

- Current share count and treasury stock method details

- Current stock price and trading multiples

- Existing debt schedule and terms

- Current credit metrics and rating

- Standalone financial projections

For Target:

- Historical financial statements

- Quality of earnings (QofE) analysis

- Management projections

- Current capital structure

- Working capital requirements

- Tax attributes (NOLs, basis, etc.)

Example Data Gathering:

ACQUIRER (BuyerCo)

Current Stock Price: $45.00

Shares Outstanding: 100M shares

Market Cap: $4,500M

Current Year EPS: $3.00

Next Year Est. EPS: $3.30

Existing Debt: $500M

TARGET (TargetCo)

Purchase Price: $1,500M

Current Revenue: $400M

Current EBITDA: $80M

Current Net Income: $45M

Existing Debt: $100M

Existing Cash: $50M

Step 2: Build Sources & Uses Table

The Sources & Uses table shows how the transaction is financed.

Uses of Funds (What You're Paying For):

Purchase Equity Value

+ Refinance Target Debt

+ Transaction Fees

+ Financing Fees

= Total Uses

Sources of Funds (How You're Paying):

New Debt

+ Acquirer Stock Issued

+ Cash from Balance Sheet

= Total Sources

Must Balance: Total Sources = Total Uses

Complete Example:

| USES OF FUNDS | $ Millions | % |

|---|---|---|

| Purchase Equity Value | $1,500 | 92.0% |

| Refinance Target Debt | $100 | 6.1% |

| Transaction Fees (2%) | $30 | 1.8% |

| TOTAL USES | $1,630 | 100.0% |

| SOURCES OF FUNDS | $ Millions | % |

|---|---|---|

| New Term Loan | $600 | 36.8% |

| Acquirer Stock (@ $45.00) | $900 | 55.2% |

| Cash from Balance Sheet | $130 | 8.0% |

| TOTAL SOURCES | $1,630 | 100.0% |

Key Calculations:

Enterprise Value = Equity Value + Debt - Cash

= $1,500M + $100M - $50M

= $1,550M

Implied Multiples:

EV / Revenue = $1,550M / $400M = 3.9x

EV / EBITDA = $1,550M / $80M = 19.4x

New Shares Issued = Stock Consideration / Stock Price

= $900M / $45.00 = 20.0M shares

Pro Forma Shares = Acquirer Shares + New Shares

= 100M + 20M = 120M shares

Step 3: Purchase Price Allocation (PPA)

Purchase price allocation determines how the purchase price is allocated on the balance sheet.

Purchase Price Allocation Formula:

Purchase Price

- Fair Value of Net Assets Acquired

= Goodwill

Key Steps:

- Identify Acquired Assets and Liabilities

- Fair Value Adjustments - Revalue to fair market value

- Identify Intangible Assets - Customer relationships, technology, brand

- Calculate Goodwill - Residual amount

Example Purchase Price Allocation:

Purchase Price: $1,500M

NET ASSETS ACQUIRED:

Current Assets $150M

PP&E (at fair value) $200M

Identified Intangibles:

- Customer Relationships (10yr) $250M

- Technology/IP (5yr) $150M

- Trade Names (indefinite) $50M

Current Liabilities ($100M)

Deferred Tax Liability (25% on intangibles) ($112M)

─────────────────────────────────────────────

Fair Value of Net Assets $588M

GOODWILL = $1,500M - $588M = $912M

Tax Impact: Intangibles create deferred tax liability because book basis ≠ tax basis (often not tax deductible)

Step 4: Build Pro Forma Income Statement

Combine both companies' income statements with adjustments.

Pro Forma Adjustments:

- Revenue - Standalone projections + synergies (if applicable)

- Cost Synergies - Cost savings from integration

- D&A - New depreciation/amortization from PPA

- Interest Expense - New debt service

- Share Count - Include new shares issued

Complete Pro Forma Example:

| Pro Forma Income Statement (Year 1) | BuyerCo | TargetCo | Adjustments | Pro Forma |

|---|---|---|---|---|

| Revenue | $2,000 | $400 | — | $2,400 |

| Cost of Revenue | (800) | (200) | — | (1,000) |

| Gross Profit | 1,200 | 200 | — | 1,400 |

| Operating Expenses | (600) | (120) | 30 | (690) |

| Cost Synergies | — | — | +$30M | — |

| D&A | (100) | (20) | (50) | (170) |

| PPA Intangible Amort. | — | — | -$50M | — |

| EBIT | 500 | 60 | (20) | 540 |

| Interest Expense | (25) | (5) | (30) | (60) |

| New Debt Interest @ 5% | — | — | -$30M | — |

| Pre-Tax Income | 475 | 55 | (50) | 480 |

| Taxes @ 25% | (119) | (14) | 13 | (120) |

| Net Income | $356 | $41 | ($37) | $360 |

Key Adjustments Explained:

- Cost Synergies (+$30M): Elimination of redundant roles, facilities, systems

- PPA Amortization (-$50M): New intangible assets amortization

Customer Relationships: $250M / 10 years = $25M/year Technology: $150M / 5 years = $30M/year Total Annual Amortization = $55M (rounded to $50M shown) - New Interest Expense (-$30M): $600M debt × 5.0% = $30M/year

- Tax Benefit (+$13M): Tax shield on incremental interest expense

Step 5: Calculate Accretion/Dilution

The Critical Question: Does the deal increase or decrease EPS?

EPS Calculation:

EPS = Net Income / Weighted Average Shares Outstanding

Accretion/Dilution Formula:

Accretion/(Dilution) % = (Pro Forma EPS - Standalone EPS) / Standalone EPS

Complete Accretion/Dilution Analysis:

| Metric | BuyerCo Standalone | Pro Forma Combined | Change |

|---|---|---|---|

| Net Income ($M) | $356 | $360 | +$4 |

| Shares Outstanding (M) | 100.0 | 120.0 | +20.0 |

| EPS | $3.56 | $3.00 | ($0.56) |

| Accretion/(Dilution) | — | — | (15.7%) |

Interpretation:

Accretion/Dilution = ($3.00 - $3.56) / $3.56 = -15.7%

Result: The deal is 15.7% DILUTIVE in Year 1

A dilutive deal can still create shareholder value if:

• The acquisition becomes accretive in future years

• Strategic value justifies near-term dilution

• Synergies create long-term value exceeding dilution

• Target's growth rate exceeds acquirer's growth rate

Step 6: Multi-Year Accretion/Dilution

Show how accretion/dilution evolves over time as synergies ramp and financing costs are paid down.

Multi-Year Analysis:

| Metric ($M except EPS) | Year 1 | Year 2 | Year 3 |

|---|---|---|---|

| STANDALONE BUYERCO | |||

| Net Income | $356 | $392 | $431 |

| Shares Outstanding | 100.0 | 100.0 | 100.0 |

| Standalone EPS | $3.56 | $3.92 | $4.31 |

| PRO FORMA COMBINED | |||

| Pro Forma Net Income | $360 | $450 | $540 |

| Pro Forma Shares | 120.0 | 120.0 | 120.0 |

| Pro Forma EPS | $3.00 | $3.75 | $4.50 |

| ACCRETION/(DILUTION) ANALYSIS | |||

| EPS Difference | ($0.56) | ($0.17) | $0.19 |

| Accretion/(Dilution) % | (15.7%) | (4.3%) | +4.4% |

Key Insights:

- Year 1: 15.7% dilutive due to high amortization and interest costs

- Year 2: 4.3% dilutive as synergies ramp up

- Year 3: 4.4% accretive as full synergies realized and growth accelerates

Synergy Ramp Assumption:

Year 1: 50% of run-rate synergies ($30M × 50% = $15M realized)

Year 2: 100% of run-rate synergies ($30M fully realized)

Year 3: Full synergies + faster growth from integration

Step 7: Alternative Deal Structures

Model multiple financing scenarios to understand trade-offs.

Scenario Comparison:

| Scenario | All Cash | 50/50 Mix | All Stock |

|---|---|---|---|

| SOURCES ($M) | |||

| Debt | $1,200 | $600 | $0 |

| Stock | $0 | $900 | $1,500 |

| Cash | $430 | $130 | $130 |

| NEW SHARES ISSUED | |||

| New Shares (M) | 0.0 | 20.0 | 33.3 |

| Pro Forma Shares (M) | 100.0 | 120.0 | 133.3 |

| YEAR 1 EPS IMPACT | |||

| Pro Forma Net Income | $307 | $360 | $397 |

| Pro Forma EPS | $3.07 | $3.00 | $2.98 |

| Accretion/(Dilution) | (13.8%) | (15.7%) | (16.3%) |

| CREDIT METRICS | |||

| Total Debt / EBITDA | 6.4x | 3.8x | 1.6x |

| Interest Coverage (EBIT/Int) | 7.3x | 9.0x | 21.6x |

Trade-offs Analysis:

All Cash/Debt:

- ✓ No dilution from new shares

- ✓ Existing shareholders maintain ownership %

- ✗ Highest interest expense drag

- ✗ Leveraged balance sheet

- ✗ Credit rating risk

50/50 Mix (Base Case):

- ✓ Balanced approach

- ✓ Manageable leverage

- ✓ Moderate dilution

- ✗ Some share dilution

- ✗ Some interest expense

All Stock:

- ✓ No debt, pristine balance sheet

- ✓ Preserves financial flexibility

- ✓ Highest net income (no interest)

- ✗ Significant dilution (33% more shares)

- ✗ Ownership dilution for existing shareholders

- ✗ Deal value fluctuates with stock price

Advanced Merger Model Considerations

Treasury Stock Method for Options/RSUs

When calculating pro forma shares, include dilutive securities.

Treasury Stock Method:

Diluted Shares = Options Outstanding - (Options × Strike Price) / Current Price

Example:

10M options outstanding @ $30 strike

Current stock price: $45

Diluted Shares = 10M - (10M × $30) / $45

= 10M - 6.7M

= 3.3M additional shares

Convertible Debt Treatment

If-Converted Method:

- Add back interest expense (after-tax)

- Add converted shares to denominator

Example:

$100M convertible debt @ 3% interest, converts to 2M shares

Add back to numerator: $100M × 3% × (1 - 25% tax) = $2.25M

Add to denominator: 2M shares

Purchase Price True-Up

Model potential purchase price adjustments:

Working Capital Adjustment:

Target Working Capital: $50M

Actual at Close: $47M

Purchase Price Reduction: $3M

Earnout Modeling:

Base Purchase Price: $1,500M

Earnout (Year 2): $100M if EBITDA > $90M

Probability-Weighted: $100M × 70% = $70M

Model as contingent liability, expense over earnout period

Synergy Modeling Deep Dive

Cost Synergies (More certain, faster to realize):

Headcount Reduction

Redundant roles: 150 positions Avg. fully-loaded cost: $150K Annual savings: 150 × $150K = $22.5M Severance cost: 150 × $100K = $15M (one-time)Facility Consolidation

Duplicate offices: 3 locations Annual rent savings: $5M One-time exit costs: $8MTechnology/Vendor Consolidation

Duplicate SaaS subscriptions: $2M/year Professional services savings: $1M/year

Revenue Synergies (Less certain, slower to realize):

Cross-Selling

Target customer base: 5,000 customers Cross-sell rate: 15% Avg. deal size: $50K Year 1 Revenue: 5,000 × 15% × $50K × 50% (ramp) = $18.8M Year 2 Revenue: 5,000 × 15% × $50K = $37.5MProduct Bundling

Price increase from bundle: 10% Affected revenue: $200M Incremental revenue: $20M/year

Synergy Capture Rate:

Year 1 Year 2 Year 3

Cost Synergies 50% 100% 100%

Revenue Syn. 20% 50% 80%

Balance Sheet Modeling

Don't forget the pro forma balance sheet!

Key Line Items:

Assets:

- Cash (post-transaction)

- Working capital (combined)

- PP&E (fair value adjustments)

- Intangible assets (PPA)

- Goodwill

Liabilities:

- New debt balances

- Deferred tax liabilities (from PPA)

- Assumed liabilities

Equity:

- Common stock (par value of new shares)

- APIC (additional paid-in capital)

- Retained earnings

Example Balance Sheet Impact:

Pre-Deal Post-Deal Change

Total Assets $5,000M $7,100M +$2,100M

Total Debt $500M $1,200M +$700M

Shareholders' Equity $4,000M $5,300M +$1,300M

Debt/Equity Ratio 12.5% 22.6% +10.1 pts

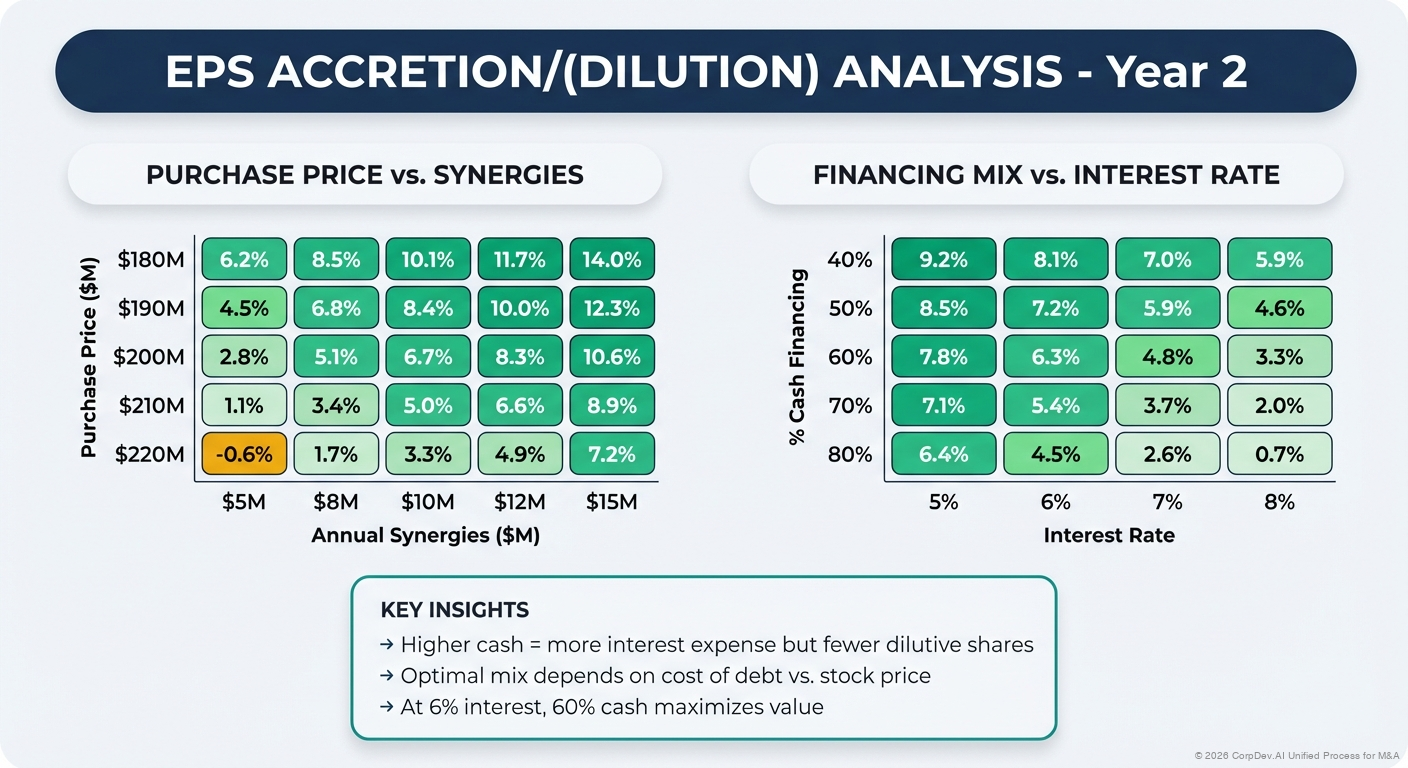

Sensitivity Analysis & Scenario Modeling

Model multiple scenarios to understand deal dynamics.

Price Sensitivity

Purchase Price vs. Accretion:

| Purchase Price | $1,300M | $1,400M | $1,500M | $1,600M |

|---|---|---|---|---|

| EV / EBITDA | 16.9x | 18.1x | 19.4x | 20.6x |

| Y1 Accretion | -10.2% | -13.1% | -15.7% | -18.5% |

| Y3 Accretion | +9.1% | +6.5% | +4.4% | +1.8% |

Synergy Sensitivity

Synergies vs. Accretion (Year 3):

Cost Synergies Realized

$20M $30M $40M

Stock Price

$40 -2.1% +4.4% +10.9%

$45 -5.3% +1.2% +7.7%

$50 -8.1% -1.8% +4.7%

Break-Even Analysis

What purchase price makes deal accretion-neutral?

Target Year 1 EPS: $3.56 (standalone)

Pro Forma Shares: 120M

Required Net Income: $3.56 × 120M = $427M

Working backwards:

Required EBITDA: $600M

Less: Target EBITDA: $80M

Implied Max Purchase EBITDA Multiple: ~17.5x

Max Purchase Price: ~$1,400M

Common Merger Model Pitfalls

1. Ignoring Transaction Costs

Problem: Forgetting fees and expenses that reduce net income or increase purchase price

Transaction Costs Include:

- Investment banker fees (1-3% of deal value)

- Legal and accounting fees ($5M-$20M)

- Due diligence costs ($2M-$5M)

- Financing fees (1-2% of debt raised)

- Consent and control change fees

Solution:

- Model all transaction costs explicitly

- Determine if costs are capitalized (added to goodwill) or expensed (reduce NI)

- Most M&A advisory fees are expensed in period incurred

Example Impact:

$1,500M deal

Transaction fees @ 2%: $30M

After-tax impact: $30M × (1 - 25%) = $22.5M hit to Year 1 NI

EPS impact: $22.5M / 120M shares = $0.19/share

2. Incorrect Share Count Calculation

Problem: Using wrong share count or forgetting dilutive securities

Common Mistakes:

- Using basic shares instead of diluted

- Forgetting to add new shares from stock consideration

- Not accounting for treasury stock method on options

- Using wrong weighted average for partial year transactions

Solution:

Pro Forma Shares =

Acquirer Diluted Shares

+ New Shares Issued for Purchase

+ Shares from Assumed Target Options (treasury method)

- Buyback from Cash Proceeds (if applicable)

Partial Year Example:

Deal closes June 30 (mid-year)

Standalone shares: 100M (full year)

New shares: 20M (half year)

Weighted Avg = 100M + (20M × 0.5) = 110M shares

3. Double-Counting or Missing Synergies

Problem: Including synergies incorrectly or missing negative synergies

Common Issues:

- Counting same synergy in multiple categories

- Ignoring costs to achieve synergies

- Forgetting revenue dis-synergies (customer losses)

- Over-estimating timing of realization

Solution:

- Build detailed synergy bridge

- Include integration costs and timeline

- Model negative synergies (customer churn, employee departures)

- Use conservative realization assumptions (50%/100% over 2 years)

Example Synergy Bridge:

Gross Cost Synergies Identified: $40M

- Integration costs (Year 1): ($15M)

- Realization rate (80%): × 80%

Net Cost Synergies: $17M (run-rate)

Revenue Synergies: $25M

- Customer churn: ($5M)

- Delayed realization (Year 1): × 30%

Net Revenue Synergies (Year 1): $6M

4. Wrong Tax Rate

Problem: Using inappropriate tax rate for pro forma entity

Issues:

- Using statutory rate instead of effective rate

- Not adjusting for non-deductible expenses

- Forgetting NOL utilization

- Ignoring international tax considerations

Solution:

- Use effective tax rate from historical financials

- Adjust for one-time items

- Model NOL usage if applicable

- Consider 163(j) interest deduction limitations

Example:

Statutory rate: 21%

State taxes: 4%

Permanent differences: +1%

Effective tax rate: 26%

NOT 21%!

5. Incorrect PPA Treatment

Problem: Wrong amortization periods or missing deferred tax impact

Common Errors:

- Amortizing goodwill (not allowed under GAAP)

- Using wrong useful lives for intangibles

- Forgetting deferred tax liability on intangibles

- Not adjusting D&A in future years

Solution:

Intangible Asset Amount Life Annual Amort

Customer Relationships $250M 10yr $25M

Technology/IP $150M 5yr $30M

Trade Names $50M Indef $0

Goodwill $912M Indef $0

Total PPA Amortization: $55M/year

Deferred Tax Liability = ($250M + $150M) × 25% = $100M

(Reduces net assets acquired, increases goodwill)

6. Forgetting Balance Sheet Impact

Problem: Only modeling P&L, ignoring B/S and credit metrics

Solution:

- Model pro forma balance sheet

- Calculate leverage ratios (Debt/EBITDA)

- Calculate coverage ratios (EBIT/Interest)

- Ensure compliance with debt covenants

- Consider rating agency impact

7. Static Stock Price Assumption

Problem: Not stress-testing impact of stock price changes on deal value

For Stock Deals:

- Deal value fluctuates with stock price

- Fixed exchange ratio vs. fixed value collar

- Impact on accretion/dilution

Solution: Model multiple stock price scenarios

Example:

Fixed exchange ratio: 0.5 shares per target share

Target shares: 30M

Fixed shares issued: 15M

Acquirer Stock Price Deal Value Impact

$40 $600M Underpay

$45 $675M Base

$50 $750M Overpay

Consider collar: 0.45 - 0.55 ratio based on $40-$50 range

Best Practices

1. Build a Flexible Model

Model Architecture:

- Separate assumptions tab (all inputs in one place)

- Scenario dropdowns for different cases

- Data validation and error checks

- Clear color coding (blue = input, black = formula)

Key Toggles:

Purchase Price: $1,500M

Stock/Cash Mix: 60% / 40%

Synergy Realization: 50% / 100% (Y1/Y2)

Closing Date: Q2 2025

Tax Rate: 25%

2. Multiple Scenarios and Sensitivities

Build Three Core Cases:

- Base Case: Most likely scenario

- Upside Case: Optimistic but achievable

- Downside Case: Conservative scenario

Key Sensitivities:

- Purchase price (±10-20%)

- Stock price (±20%)

- Synergies (50%-150% of plan)

- Growth rates

- Financing costs

3. Link to Strategic Rationale

Beyond the Numbers:

- Why does deal make strategic sense?

- How does valuation compare to standalone DCF?

- What's the walk from DCF value to offer price?

- What are the key value creation drivers?

Strategic Value Bridge:

DCF Standalone Value: $1,200M

+ Control Premium (20%): $240M

+ PV of Cost Synergies: $180M

+ PV of Revenue Synergies: $120M

+ Strategic/Platform Value: $100M

─────────────────────────────────

Justifiable Price: $1,840M

Actual Offer: $1,500M

Margin of Safety: $340M (23%)

4. Credit and Leverage Analysis

Key Metrics to Track:

| Metric | Investment Grade Target | High Yield Target |

|---|---|---|

| Debt / EBITDA | < 3.0x | < 5.0x |

| EBIT / Interest | >> 5.0x | >> 3.0x |

| Debt / Total Cap | < 40% | < 60% |

| FCF / Debt | > 20% | > 10% |

5. Football Field Valuation Summary

Present merger model results alongside other valuation methods:

Valuation Method Low Mid High

─────────────────────────────────────────────────────

DCF Analysis $1,200 $1,350 $1,500

Comparable Companies $1,150 $1,300 $1,450

Precedent Transactions $1,300 $1,450 $1,600

─────────────────────────────────────────────────────

Implied Range $1,150 $1,367 $1,517

Management Target $1,500

Control Premium 15.8%

6. Returns Analysis

Calculate returns metrics beyond accretion/dilution:

Internal Rate of Return (IRR):

Year 0: Purchase Price ($1,500M)

Year 1-5: Annual FCF $100M - $180M

Year 5: Exit Value $2,100M (14x EBITDA)

IRR = 18.5%

Return on Invested Capital (ROIC):

ROIC = NOPAT / Invested Capital

Year 3 ROIC:

NOPAT: $85M

Invested Capital: $1,500M

ROIC = $85M / $1,500M = 5.7%

Target: Exceed WACC (typically 8-12%)

7. Risk-Adjusted Analysis

Probability-Weight Scenarios:

Prob EPS Weighted

Base Case 50% $3.00 $1.50

Upside 25% $3.75 $0.94

Downside 25% $2.40 $0.60

─────────────────────────────────────────

Expected EPS $3.04

Standalone EPS: $3.56

Expected Dilution: -14.6%

8. Board Presentation Framework

Key Slides for Board:

- Transaction Overview - Price, structure, rationale

- Strategic Fit - Why this deal, why now

- Valuation Summary - Football field

- Sources & Uses - Deal financing

- Financial Impact - Accretion/dilution

- Sensitivities - Key risk factors

- Synergy Bridge - Cost and revenue synergies

- Integration Plan - Timeline and risks

- Alternatives - Why not other targets

- Recommendation - Go/no-go with clear logic

Real-World Merger Model Example

Case Study: TechAcquirer buys CloudTarget

Deal Parameters

TechAcquirer (Buyer):

Current Stock Price: $85.00

Shares Outstanding: 500M

Market Cap: $42.5B

LTM Revenue: $10.0B

LTM EBITDA: $2.5B

LTM Net Income: $1.5B

Current EPS: $3.00

P/E Ratio: 28.3x

CloudTarget (Target):

Purchase Price: $5.0B

LTM Revenue: $800M

LTM EBITDA: $160M

LTM Net Income: $85M

Existing Debt: $200M

Cash: $100M

Deal Structure

| Sources & Uses | $ Millions |

|---|---|

| USES | |

| Purchase Equity Value | $5,000 |

| Refinance Target Debt | $200 |

| Transaction Fees (2%) | $100 |

| Total Uses | $5,300 |

| SOURCES | |

| Stock (70% @ $85.00) | $3,710 |

| New Term Loan (30%) | $1,590 |

| Total Sources | $5,300 |

New Shares Issued: $3,710M / $85.00 = 43.6M shares

Pro Forma Shares: 500M + 43.6M = 543.6M shares

Accretion/Dilution Analysis

Year 1 Pro Forma:

TechAcquirer Standalone NI: $1,500M

CloudTarget NI: $85M

Combined Pre-Synergies: $1,585M

Adjustments:

- PPA Amortization ($800M/8yr) ($100M)

- New Interest @ 5.0% ($80M)

+ Cost Synergies (50% realized) $60M

- Transaction Costs ($75M)

+ Tax Benefit @ 25% $49M

═══════════════════════════════════════

Pro Forma Net Income: $1,439M

Pro Forma EPS = $1,439M / 543.6M = $2.65

Standalone EPS: $3.00

Pro Forma EPS: $2.65

Accretion/(Dilution): -11.7% DILUTIVE

Year 3 Pro Forma (Full Synergies):

Pro Forma Net Income: $1,950M

Pro Forma Shares: 543.6M

Pro Forma EPS: $3.59

Standalone EPS (projected): $3.50

Accretion: +2.6% ACCRETIVE

Conclusion: Deal is dilutive in Year 1 but becomes accretive by Year 3 as synergies fully realize.

Full Merger Model Template

This section provides a complete, production-ready merger model template that can be used as-is for mid-market and large company M&A transactions. Copy this template into Excel and customize the inputs for your specific deal.

SECTION 1: Transaction Assumptions & Inputs

Use this section for all deal-specific inputs. Keep all assumptions in one place for easy scenario analysis.

═══════════════════════════════════════════════════════════════

MERGER MODEL INPUTS

═══════════════════════════════════════════════════════════════

TRANSACTION OVERVIEW

───────────────────────────────────────────────────────────────

Deal Announcement Date: [MM/DD/YYYY]

Expected Close Date: [MM/DD/YYYY]

Transaction Structure: [Stock/Cash/Mixed]

Target Company Name: [TargetCo]

Acquirer Company Name: [AcquirerCo]

PURCHASE PRICE & CONSIDERATION

───────────────────────────────────────────────────────────────

Purchase Equity Value ($M): $1,500

Premium to Current Price: 25.0%

Premium to 30-Day VWAP: 22.5%

Form of Consideration:

% Cash: 40.0%

% Stock: 60.0%

Total: 100.0%

Cash Consideration ($M): $600

Stock Consideration ($M): $900

IMPLIED VALUATION MULTIPLES

───────────────────────────────────────────────────────────────

Target LTM Revenue ($M): $400

Target LTM EBITDA ($M): $80

Target LTM EBIT ($M): $60

Target Net Debt ($M): $50

(Debt $100M - Cash $50M)

Enterprise Value ($M): $1,550

(Equity Value $1,500 + Net Debt $50)

EV / LTM Revenue: 3.9x

EV / LTM EBITDA: 19.4x

EV / LTM EBIT: 25.8x

P / LTM Net Income ($45M): 33.3x

ACQUIRER INFORMATION

───────────────────────────────────────────────────────────────

Current Stock Price: $45.00

Shares Outstanding - Basic (M): 100.0

Treasury Stock Options (M): 5.0

Diluted Shares Outstanding (M): 103.0

Market Capitalization ($M): $4,500

Current Year Est. EPS: $3.00

Next Year Est. EPS: $3.30

Current P/E Ratio: 15.0x

Existing Total Debt ($M): $500

Existing Cash ($M): $300

Net Debt ($M): $200

TARGET INFORMATION

───────────────────────────────────────────────────────────────

Target Shares Outstanding (M): 30.0

Implied Price per Share: $50.00

Pre-Announcement Price: $40.00

Target Existing Debt ($M): $100

Target Cash ($M): $50

Target Net Debt ($M): $50

FINANCING ASSUMPTIONS

───────────────────────────────────────────────────────────────

New Debt Issuance ($M): $600

Revolver Draw ($M): $0

Term Loan A ($M): $400

Term Loan B ($M): $200

Senior Notes ($M): $0

Weighted Average Cost of Debt: 5.00%

Revolver Rate: 4.50%

Term Loan A Rate: 4.75%

Term Loan B Rate: 5.50%

Senior Notes Rate: 5.25%

Target Debt to Refinance ($M): $100

Cash from Balance Sheet ($M): $130

New Stock Issuance:

Dollar Amount ($M): $900

Stock Price for Issuance: $45.00

New Shares Issued (M): 20.0

Pro Forma Shares Outstanding (M): 123.0

TRANSACTION COSTS & FEES

───────────────────────────────────────────────────────────────

M&A Advisory Fees (% of Equity Value): 2.0%

M&A Advisory Fees ($M): $30.0

Legal & Accounting ($M): $15.0

Due Diligence Costs ($M): $3.0

Financing Fees (% of Debt): 1.5%

Financing Fees ($M): $9.0

Other Transaction Costs ($M): $3.0

Total Transaction Costs ($M): $60.0

Treatment of Transaction Costs:

Expensed in Current Period: $48.0

Capitalized (Debt Fees): $9.0

Seller-Paid Fees: $3.0

TAX ASSUMPTIONS

───────────────────────────────────────────────────────────────

Acquirer Effective Tax Rate: 25.0%

Target Effective Tax Rate: 25.0%

Pro Forma Tax Rate: 25.0%

Tax Structure: [Taxable/Tax-Free]

Target NOLs ($M): $0

Annual NOL Limitation (§382): $0

SYNERGY ASSUMPTIONS

───────────────────────────────────────────────────────────────

COST SYNERGIES (Run-Rate):

Headcount Reduction:

Positions Eliminated: 150

Avg. Fully-Loaded Cost ($K): $150

Annual Savings ($M): $22.5

Facility Consolidation ($M): $5.0

Vendor/Technology Consolidation ($M): $3.0

Other Operating Expense Savings ($M): $2.5

Total Run-Rate Cost Synergies ($M): $33.0

Cost Synergy Realization:

Year 1 (% of run-rate): 50%

Year 2 (% of run-rate): 100%

Year 3+ (% of run-rate): 100%

One-Time Costs to Achieve:

Severance ($M): $15.0

Facility Exit Costs ($M): $8.0

System Integration ($M): $12.0

Other Integration Costs ($M): $5.0

Total Integration Costs ($M): $40.0

Integration Cost Timing:

Year 1: 75%

Year 2: 25%

REVENUE SYNERGIES (Run-Rate):

Cross-Selling Revenue ($M): $15.0

Product Bundling Uplift ($M): $8.0

Market Expansion ($M): $5.0

Total Run-Rate Revenue Synergies ($M): $28.0

Revenue Synergy Realization:

Year 1 (% of run-rate): 20%

Year 2 (% of run-rate): 50%

Year 3 (% of run-rate): 80%

Year 4+ (% of run-rate): 100%

Incremental Margin on Revenue Synergies: 60%

DIS-SYNERGIES:

Customer Churn ($M): $10.0

Key Employee Departures Impact ($M): $5.0

Total Dis-Synergies ($M): $15.0

WACC / DISCOUNT RATE ASSUMPTIONS

───────────────────────────────────────────────────────────────

Risk-Free Rate (10Y Treasury): 4.0%

Beta (Levered): 1.2

Market Risk Premium: 5.5%

Size Premium: 2.0%

Cost of Equity: 12.6%

= Rf + (Beta × MRP) + Size Premium

= 4.0% + (1.2 × 5.5%) + 2.0%

After-Tax Cost of Debt: 3.75%

= 5.0% × (1 - 25%)

Target Capital Structure:

Debt / (Debt + Equity): 20%

Equity / (Debt + Equity): 80%

WACC: 11.1%

= (80% × 12.6%) + (20% × 3.75%)

SECTION 2: Sources & Uses of Funds

═══════════════════════════════════════════════════════════════

SOURCES & USES

═══════════════════════════════════════════════════════════════

USES OF FUNDS $M % of Total

───────────────────────────────────────────────────────────────

Purchase Target Equity $1,500 92.0%

Repay/Refinance Target Debt $100 6.1%

Transaction Fees & Expenses $30 1.8%

Financing Fees $0 0.0%

─────────────────────

TOTAL USES $1,630 100.0%

SOURCES OF FUNDS $M % of Total

───────────────────────────────────────────────────────────────

New Term Loan $600 36.8%

Acquirer Stock Issued $900 55.2%

Cash from Balance Sheet $130 8.0%

Revolver Draw $0 0.0%

─────────────────────

TOTAL SOURCES $1,630 100.0%

Check (must = $0): $0 ✓

TRANSACTION SUMMARY METRICS

───────────────────────────────────────────────────────────────

Total Transaction Value ($M): $1,630

Enterprise Value ($M): $1,550

Equity Value ($M): $1,500

Net Debt Assumed ($M): $50

Purchase Price per Target Share: $50.00

Target Shares Acquired (M): 30.0

Premium Paid:

vs. Unaffected Price ($40): 25.0%

vs. 30-Day VWAP ($41): 22.0%

vs. 52-Week High ($48): 4.2%

New Acquirer Shares Issued (M): 20.0

Exchange Ratio (per target share): 0.667x

Fixed Collar Range: $42 - $48

Pro Forma Ownership:

Existing Acquirer Shareholders: 83.7%

Former Target Shareholders: 16.3%

SECTION 3: Purchase Price Allocation (PPA)

═══════════════════════════════════════════════════════════════

PURCHASE PRICE ALLOCATION (PPA)

═══════════════════════════════════════════════════════════════

PURCHASE PRICE $M

───────────────────────────────────────────────────────────────

Total Consideration Paid $1,500

LESS: FAIR VALUE OF NET ASSETS ACQUIRED

───────────────────────────────────────────────────────────────

ASSETS:

Current Assets:

Cash & Equivalents $50

Accounts Receivable $60

Inventory $30

Other Current Assets $10

Total Current Assets $150

Fixed Assets (PP&E):

Book Value $150

Fair Value Step-Up $50

Fair Value of PP&E $200

Identified Intangible Assets:

Customer Relationships

Fair Value $250

Useful Life (years) 10

Annual Amortization $25

Developed Technology/IP

Fair Value $150

Useful Life (years) 5

Annual Amortization $30

Trade Names & Trademarks

Fair Value $50

Useful Life Indefinite

Annual Amortization $0

Non-Compete Agreements

Fair Value $20

Useful Life (years) 3

Annual Amortization $7

Total Identified Intangibles $470

Total Annual Amortization $62

Other Assets $10

TOTAL ASSETS ACQUIRED $830

LIABILITIES:

Current Liabilities:

Accounts Payable $50

Accrued Expenses $30

Deferred Revenue $20

Total Current Liabilities ($100)

Long-Term Liabilities:

Deferred Tax Liability (on intangibles)

Tax Rate 25%

Taxable Intangibles $470

DTL Created ($118)

Other Long-Term Liabilities ($10)

TOTAL LIABILITIES ASSUMED ($228)

NET ASSETS ACQUIRED (Fair Value) $602

GOODWILL CALCULATION

───────────────────────────────────────────────────────────────

Purchase Price $1,500

Less: Fair Value of Net Assets ($602)

──────

GOODWILL $898

Goodwill as % of Purchase Price: 59.9%

ANNUAL AMORTIZATION EXPENSE SCHEDULE

───────────────────────────────────────────────────────────────

Y1 Y2 Y3 Y4 Y5 Total

Customer Relationships $25 $25 $25 $25 $25 $125

Technology/IP $30 $30 $30 $30 $30 $150

Trade Names $0 $0 $0 $0 $0 $0

Non-Compete $7 $7 $7 $0 $0 $20

─────────────────────────────────────

Total PPA Amortization $62 $62 $62 $55 $55 $295

Note: Goodwill and indefinite-lived intangibles are not

amortized but subject to annual impairment testing.

SECTION 4: Pro Forma Income Statement (5-Year Projection)

═══════════════════════════════════════════════════════════════════════════════════════

PRO FORMA INCOME STATEMENT

═══════════════════════════════════════════════════════════════════════════════════════

($M except per share data) LTM Year 1 Year 2 Year 3 Year 4 Year 5

───────────────────────────────────────────────────────────────────────────────────────

ACQUIRER STANDALONE

Revenue $2,000 $2,200 $2,420 $2,662 $2,928 $3,221

% Growth — 10.0% 10.0% 10.0% 10.0% 10.0%

COGS (800) (880) (968) (1,065) (1,171) (1,288)

Gross Profit 1,200 1,320 1,452 1,597 1,757 1,933

Gross Margin % 60.0% 60.0% 60.0% 60.0% 60.0% 60.0%

Operating Expenses (600) (638) (665) (692) (721) (750)

D&A (100) (110) (121) (133) (146) (161)

EBIT 500 572 666 772 890 1,022

EBIT Margin % 25.0% 26.0% 27.5% 29.0% 30.4% 31.7%

Interest Expense (25) (25) (25) (24) (23) (22)

Pre-Tax Income 475 547 641 748 867 1,000

Taxes @ 25% (119) (137) (160) (187) (217) (250)

Net Income $356 $410 $481 $561 $650 $750

Diluted Shares (M) 103.0 103.0 103.0 103.0 103.0 103.0

EPS - Standalone $3.46 $3.98 $4.67 $5.45 $6.31 $7.28

───────────────────────────────────────────────────────────────────────────────────────

TARGET STANDALONE

Revenue $400 $460 $529 $608 $699 $804

% Growth — 15.0% 15.0% 15.0% 15.0% 15.0%

COGS (200) (230) (265) (304) (350) (402)

Gross Profit 200 230 264 304 349 402

Gross Margin % 50.0% 50.0% 50.0% 50.0% 50.0% 50.0%

Operating Expenses (120) (129) (138) (146) (154) (161)

D&A (20) (21) (22) (23) (24) (25)

EBIT 60 80 104 135 171 216

EBIT Margin % 15.0% 17.4% 19.7% 22.2% 24.5% 26.9%

Interest Expense (5) (5) (5) (5) (5) (5)

Pre-Tax Income 55 75 99 130 166 211

Taxes @ 25% (14) (19) (25) (33) (42) (53)

Net Income $41 $56 $74 $98 $125 $158

───────────────────────────────────────────────────────────────────────────────────────

PRO FORMA ADJUSTMENTS

PPA Amortization — (62) (62) (62) (55) (55)

New Interest Expense — (30) (30) (29) (28) (27)

Eliminate Target Interest — 5 5 5 5 5

Cost Synergies Realized — 17 33 33 33 33

Revenue Synergies (60% margin) — 3 8 13 17 17

Dis-Synergies — (15) (8) (3) 0 0

Integration Costs — (30) (10) 0 0 0

Transaction Costs (expensed) — (48) 0 0 0 0

Tax Impact of Adjustments @ 25% — 30 16 11 8 7

Total Pro Forma Adjustments — (130) (48) (32) (20) (20)

───────────────────────────────────────────────────────────────────────────────────────

PRO FORMA COMBINED

Revenue $2,400 $2,660 $2,949 $3,270 $3,627 $4,025

% Growth YoY — 10.8% 10.9% 10.9% 10.9% 11.0%

Combined Gross Profit 1,400 1,550 1,716 1,901 2,106 2,335

Gross Margin % 58.3% 58.3% 58.2% 58.1% 58.1% 58.0%

Combined Operating Expenses (720) (750) (775) (805) (842) (878)

Combined D&A (120) (131) (143) (156) (170) (186)

PPA Amortization — (62) (62) (62) (55) (55)

Cost Synergies — 17 33 33 33 33

Integration Costs — (30) (10) 0 0 0

Pro Forma EBIT 560 594 759 911 1,072 1,249

EBIT Margin % 23.3% 22.3% 25.7% 27.9% 29.6% 31.0%

Pro Forma Interest Expense (30) (50) (50) (48) (46) (44)

Pro Forma Pre-Tax Income 530 544 709 863 1,026 1,205

Pro Forma Taxes @ 25% (133) (136) (177) (216) (257) (301)

PRO FORMA NET INCOME $397 $408 $532 $647 $770 $904

Pro Forma Diluted Shares (M) 123.0 123.0 123.0 123.0 123.0 123.0

PRO FORMA EPS $3.23 $3.32 $4.33 $5.26 $6.26 $7.35

───────────────────────────────────────────────────────────────────────────────────────

ACCRETION / (DILUTION) ANALYSIS

Standalone EPS $3.46 $3.98 $4.67 $5.45 $6.31 $7.28

Pro Forma EPS $3.23 $3.32 $4.33 $5.26 $6.26 $7.35

Difference ($0.23) ($0.66) ($0.34) ($0.19) ($0.05) $0.07

Accretion / (Dilution) % (6.6%) (16.6%) (7.3%) (3.5%) (0.8%) 1.0%

Status DILUTIVE DILUTIVE DILUTIVE DILUTIVE DILUTIVE ACCRETIVE

SECTION 5: Pro Forma Balance Sheet

═══════════════════════════════════════════════════════════════

PRO FORMA BALANCE SHEET (Post-Close)

═══════════════════════════════════════════════════════════════

($M) Acquirer Target Adj. Pro Forma

───────────────────────────────────────────────────────────────

ASSETS

Current Assets:

Cash & Equivalents $300 $50 ($170) $180

Accounts Receivable 400 60 0 460

Inventory 200 30 0 230

Other Current Assets 100 10 0 110

Total Current Assets 1,000 150 (170) 980

Fixed Assets (PP&E):

Gross PP&E 2,000 150 50 2,200

Accumulated Depreciation (800) 0 0 (800)

Net PP&E 1,200 150 50 1,400

Intangible Assets:

Customer Relationships 0 0 250 250

Technology/IP 0 0 150 150

Trade Names 0 0 50 50

Non-Compete 0 0 20 20

Total Intangibles 0 0 470 470

Goodwill 500 0 898 1,398

Other Assets 100 10 0 110

TOTAL ASSETS $2,800 $310 $1,248 $4,358

───────────────────────────────────────────────────────────────

LIABILITIES

Current Liabilities:

Accounts Payable $200 $50 $0 $250

Accrued Expenses 150 30 0 180

Short-Term Debt 50 0 0 50

Deferred Revenue 0 20 0 20

Total Current Liabilities 400 100 0 500

Long-Term Debt:

Existing Acquirer Debt 450 0 0 450

Target Debt (refinanced) 0 100 (100) 0

New Debt 0 0 600 600

Total Long-Term Debt 450 100 500 1,050

Deferred Tax Liability 100 0 118 218

Other Liabilities 50 10 0 60

TOTAL LIABILITIES $1,000 $210 $518 $1,728

───────────────────────────────────────────────────────────────

SHAREHOLDERS' EQUITY

Common Stock (par) $10 $3 $2 $12

Additional Paid-In Capital 600 37 898 1,535

Retained Earnings 1,190 60 (170) 1,080

Treasury Stock 0 0 0 0

TOTAL EQUITY $1,800 $100 $730 $2,630

TOTAL LIABILITIES & EQUITY $2,800 $310 $1,248 $4,358

───────────────────────────────────────────────────────────────

KEY BALANCE SHEET METRICS

Total Debt $1,100

Cash $180

Net Debt $920

Book Value of Equity $2,630

Shares Outstanding (M) 123.0

Book Value per Share $21.38

Debt / Equity 41.8%

Debt / Total Capitalization 29.5%

SECTION 6: Credit Metrics & Leverage Analysis

═══════════════════════════════════════════════════════════════

CREDIT METRICS ANALYSIS

═══════════════════════════════════════════════════════════════

Year 1 Year 2 Year 3 Year 4 Year 5

───────────────────────────────────────────────────────────────────────────

EBITDA CALCULATION

Pro Forma EBIT $594 $759 $911 $1,072 $1,249

+ Pro Forma D&A 193 205 218 225 241

Pro Forma EBITDA $787 $964 $1,129 $1,297 $1,490

DEBT SCHEDULE

Beginning Debt Balance $1,100 $1,045 $985 $920 $850

Mandatory Amortization (50) (55) (60) (65) (70)

Optional Prepayment (5) (5) (5) (5) (5)

Ending Debt Balance $1,045 $985 $920 $850 $775

Average Debt $1,073 $1,015 $953 $885 $813

Interest Expense @ 5.0% $50 $50 $48 $46 $44

LEVERAGE RATIOS

Total Debt / EBITDA 1.3x 1.0x 0.8x 0.7x 0.5x

Net Debt / EBITDA 1.2x 0.9x 0.7x 0.5x 0.4x

Target Covenant: < 3.5x ✓ ✓ ✓ ✓ ✓

COVERAGE RATIOS

EBITDA / Interest 15.7x 19.3x 23.5x 28.2x 33.9x

EBIT / Interest 11.9x 15.2x 19.0x 23.3x 28.4x

(EBITDA - Capex) / Interest 13.1x 16.5x 20.3x 24.7x 29.9x

Target Covenant: >> 3.0x ✓ ✓ ✓ ✓ ✓

FREE CASH FLOW METRICS

EBITDA $787 $964 $1,129 $1,297 $1,490

- Cash Interest (50) (50) (48) (46) (44)

- Cash Taxes (136) (177) (216) (257) (301)

- Capex (132) (145) (163) (181) (201)

- Change in NWC (15) (18) (20) (23) (25)

Unlevered Free Cash Flow $454 $574 $682 $790 $919

- Debt Amortization (55) (60) (65) (70) (75)

Levered Free Cash Flow $399 $514 $617 $720 $844

FCF / Total Debt 38.2% 52.2% 67.1% 84.7% 108.9%

FCF Yield on Purchase Price 26.6% 34.3% 41.1% 48.0% 56.3%

RETURNS METRICS

ROIC (Unlevered):

NOPAT $446 $570 $684 $804 $937

Invested Capital $1,500 $1,500 $1,500 $1,500 $1,500

ROIC 29.7% 38.0% 45.6% 53.6% 62.5%

ROE:

Net Income $408 $532 $647 $770 $904

Avg. Shareholders' Equity $2,215 $2,630 $2,630 $2,630 $2,630

ROE 18.4% 20.2% 24.6% 29.3% 34.4%

SECTION 7: Sensitivity Analysis Tables

═══════════════════════════════════════════════════════════════

SENSITIVITY ANALYSIS

═══════════════════════════════════════════════════════════════

TABLE 1: PURCHASE PRICE vs. ACCRETION (Year 1)

───────────────────────────────────────────────────────────────

Purchase Price ($M)

Stock/Cash Mix $1,300 $1,400 $1,500 $1,600 $1,700

─────────────────────────────────────────────────────────────

100% Stock (8.2%) (11.5%) (14.9%) (18.1%) (21.2%)

75% Stock (9.5%) (12.9%) (16.3%) (19.6%) (22.8%)

50% Stock (11.1%) (14.6%) (18.0%) (21.3%) (24.6%)

25% Stock (13.2%) (16.8%) (20.3%) (23.7%) (27.0%)

100% Cash (16.8%) (20.5%) (24.1%) (27.6%) (31.0%)

Note: All-stock less dilutive short-term, but all-cash preserves

future upside for existing shareholders

TABLE 2: SYNERGIES vs. YEAR 3 ACCRETION

───────────────────────────────────────────────────────────────

Cost Synergies Realized ($M)

Revenue Syn. $20 $30 $40 $50 $60

─────────────────────────────────────────────────────────────

$0 (12.1%) (7.3%) (2.5%) 2.3% 7.1%

$15 (9.8%) (5.0%) (0.2%) 4.6% 9.4%

$30 (7.5%) (2.7%) 2.1% 6.9% 11.7%

$45 (5.2%) (0.4%) 4.4% 9.2% 14.0%

$60 (2.9%) 1.9% 6.7% 11.5% 16.3%

Base Case Assumptions: $33M cost synergies, $28M revenue synergies

TABLE 3: ACQUIRER STOCK PRICE vs. YEAR 1 ACCRETION

───────────────────────────────────────────────────────────────

Acquirer Stock Price at Close

% Stock Used $35 $40 $45 $50 $55

─────────────────────────────────────────────────────────────

40% (14.2%) (15.1%) (16.6%) (18.5%) (20.8%)

50% (13.8%) (14.8%) (16.3%) (18.2%) (20.5%)

60% (13.3%) (14.4%) (15.9%) (17.9%) (20.2%)

70% (12.9%) (14.0%) (15.6%) (17.5%) (19.9%)

80% (12.4%) (13.6%) (15.2%) (17.2%) (19.5%)

Lower stock price = More shares issued = More dilution

Higher stock price = Fewer shares issued = Less dilution

TABLE 4: INTEGRATION COSTS vs. NET SYNERGIES (NPV)

───────────────────────────────────────────────────────────────

Integration Costs ($M)

Synergies $25 $35 $45 $55 $65

─────────────────────────────────────────────────────────────

$50 Run-Rate $208 $198 $188 $178 $168

$60 Run-Rate $258 $248 $238 $228 $218

$70 Run-Rate $308 $298 $288 $278 $268

$80 Run-Rate $358 $348 $338 $328 $318

$90 Run-Rate $408 $398 $388 $378 $368

NPV = PV of synergies over 5 years @ 11% WACC - Integration Costs

Base Case: $61M run-rate synergies, $40M integration costs = $238M NPV

TABLE 5: BREAK-EVEN ANALYSIS

───────────────────────────────────────────────────────────────

To achieve Year 1 EPS accretion-neutral ($3.98):

OPTION 1: Reduce Purchase Price

Maximum EV: $1,285M

Implied EBITDA Multiple: 16.1x

Current Offer: 19.4x

Required Discount: 17%

OPTION 2: Increase Synergies

Required Additional Cost Synergies: $52M (vs. $33M base)

Increase Required: 58%

OPTION 3: Change Financing Mix

Required % Cash (vs. 40% base): 72%

Additional Debt Required: $480M

Pro Forma Leverage: 4.1x (vs. 1.3x base)

OPTION 4: Combination Approach

Purchase Price: $1,400M (-7%)

Cost Synergies: $42M (+27%)

% Cash: 50% (+10pp)

Result: ~0% Y1 Accretion

SECTION 8: Alternative Deal Structure Scenarios

═══════════════════════════════════════════════════════════════

DEAL STRUCTURE COMPARISON

═══════════════════════════════════════════════════════════════

Scenario A Scenario B Scenario C

All Stock 50/50 Mix All Cash

───────────────────────────────────────────────────────────────

DEAL TERMS

Purchase Price ($M) $1,500 $1,500 $1,500

Stock Consideration 100% 50% 0%

Cash Consideration 0% 50% 100%

FINANCING

New Debt ($M) $100 $850 $1,600

Stock Issued ($M) $1,500 $750 $0

Cash Used ($M) $30 $30 $30

New Shares Issued (M) 33.3 16.7 0.0

Pro Forma Shares (M) 136.3 119.7 103.0

YEAR 1 FINANCIALS

Pro Forma EBIT $594 $594 $594

Interest Expense (10) (48) (88)

EBT 584 546 506

Taxes @ 25% (146) (137) (127)

Net Income $438 $410 $380

EPS $3.21 $3.42 $3.69

Standalone EPS $3.98 $3.98 $3.98

Accretion/(Dilution) (19.3%) (14.1%) (7.3%)

YEAR 3 FINANCIALS

Pro Forma EBIT $911 $911 $911

Interest Expense (8) (43) (78)

EBT 903 868 833

Net Income $677 $651 $625

EPS $4.97 $5.44 $6.07

Standalone EPS $5.45 $5.45 $5.45

Accretion/(Dilution) (8.8%) (0.2%) 11.4%

CREDIT METRICS (Year 1)

Total Debt $600 $1,350 $2,100

EBITDA $787 $787 $787

Debt / EBITDA 0.8x 1.7x 2.7x

EBIT / Interest 59.4x 12.4x 6.8x

Rating Implication AA A BBB+

Cost of Debt 4.00% 5.00% 6.00%

STRATEGIC CONSIDERATIONS

─────────────────────────────────────────────────────────────

Scenario A (All Stock):

✓ Minimal debt, pristine balance sheet

✓ Maximum financial flexibility

✓ Aligns incentives (target shareholders stay invested)

✗ Significant dilution (25% more shares)

✗ Deal value fluctuates with stock price

✗ Most dilutive to existing shareholders

Scenario B (50/50 Mix):

✓ Balanced approach

✓ Moderate leverage

✓ Manageable dilution (16% more shares)

✓ Maintains investment grade rating

≈ Moderate risk/return profile

Scenario C (All Cash):

✓ No share dilution

✓ Fixed deal value

✓ Highest near-term EPS (lowest share count)

✗ High leverage (2.7x)

✗ Constrains financial flexibility

✗ Higher interest burden

✗ May require asset sales or equity raise later

RECOMMENDATION: Scenario B (50/50 Mix) offers best balance

SECTION 9: Deal Summary Dashboard

═══════════════════════════════════════════════════════════════

EXECUTIVE SUMMARY METRICS

═══════════════════════════════════════════════════════════════

TRANSACTION OVERVIEW

─────────────────────────────────────────────────────────────

Target Company: TargetCo

Purchase Price: $1,500M

Enterprise Value: $1,550M

Financing: 60% Stock / 40% Debt+Cash

Expected Close: Q2 2025

VALUATION

─────────────────────────────────────────────────────────────

EV / LTM Revenue: 3.9x

EV / LTM EBITDA: 19.4x

EV / LTM EBIT: 25.8x

Premium to Market Price: 25.0%

Benchmark Median Multiples:

Public Comps EV/EBITDA: 17.5x [Above]

Recent M&A EV/EBITDA: 18.2x [Above]

STRATEGIC RATIONALE

─────────────────────────────────────────────────────────────

1. Expand addressable market by $2.5B

2. Accelerate product roadmap by 18-24 months

3. Gain 350 enterprise customers

4. Achieve #1 or #2 market position in 3 verticals

5. Realize $61M annual run-rate synergies

FINANCIAL IMPACT (Year 1 → Year 3)

─────────────────────────────────────────────────────────────

Year 1 Year 3

Revenue $2,660M $3,270M

Growth Rate 10.8% 10.9%

EBITDA $787M $1,129M

Margin 29.6% 34.5%

EPS (Pro Forma) $3.32 $5.26

Accretion/(Dilution) (16.6%) (3.5%)

Free Cash Flow $399M $617M

FCF Yield 26.6% 41.1%

RETURNS ANALYSIS

─────────────────────────────────────────────────────────────

5-Year IRR on Investment: 17.8%

Year 3 ROIC: 45.6%

Year 5 ROIC: 62.5%

Payback Period (undiscounted): 3.2 years

NPV of Synergies (@ 11% WACC): $238M

NPV of Deal (vs. $1,500M price): Positive if synergies >> 85%

RISK FACTORS & MITIGANTS

─────────────────────────────────────────────────────────────

Risk Mitigation

────────────────────────────────────────────────────────────

Integration complexity Dedicated PMO team, 100-day plan

Customer churn (10% modeled) Retention bonuses, customer success

Key talent retention Stay bonuses for top 50 employees

Synergy realization (85% prob) Conservative phasing, external advisors

Regulatory approval Pre-filing with FTC, clean Hart-Scott

CREDIT PROFILE

─────────────────────────────────────────────────────────────

Pro Forma Debt / EBITDA: 1.3x

Interest Coverage: 15.7x

Pro Forma Rating: A (Stable)

Covenant Headroom:

Max Leverage (3.5x): 2.2x headroom ✓

Min Interest Coverage (3.0x): 12.7x headroom ✓

GOVERNANCE & APPROVALS

─────────────────────────────────────────────────────────────

Board Approval Required: Yes (>$1B transaction)

Shareholder Vote Required: Yes (>20% dilution)

Regulatory Approvals: Hart-Scott-Rodino (HSR)

Expected Vote Support: 75%+ (based on investor calls)

GO / NO-GO DECISION CRITERIA

─────────────────────────────────────────────────────────────

Criterion Target Actual Status

──────────────────────────────────────────────────────────────

EV/EBITDA < 20x <20x 19.4x ✓ PASS

Year 3 Accretive >>0% (3.5%) ✗ MISS

Debt/EBITDA < 2.5x <2.5x 1.3x ✓ PASS

ROIC > WACC by Year 3 >>11% 45.6% ✓ PASS

Synergy NPV > $200M >>$200M $238M ✓ PASS

Strategic Fit Score >>8/10 9/10 ✓ PASS

Integration Risk Medium Medium ✓ PASS

Overall Assessment: PROCEED

(6 of 7 pass)

SECTION 10: Model Usage Instructions

Step 1: Input Collection

Fill in all blue-highlighted cells in Section 1 (Transaction Assumptions). Ensure you have:

• Audited financials for both companies (3 years historical)

• Management projections

• Current stock prices and share counts

• Debt terms and schedules

• Quality of earnings adjustments

Step 2: PPA Development

Work with external valuation firm or accounting team to:

• Identify all intangible assets

• Determine fair values

• Assign useful lives

• Calculate deferred tax impacts

Step 3: Synergy Validation

Build bottom-up synergy analysis:

• Interview functional leaders (HR, IT, Facilities, Ops)

• Get specific headcount reduction lists

• Model revenue synergies conservatively

• Account for dis-synergies (churn, disruption)

• Estimate integration costs and timing

Step 4: Scenario Analysis

Build 3 cases (Base, Upside, Downside):

• Vary key assumptions (growth, synergies, price)

• Stress test financing structures

• Run sensitivities on critical variables

• Calculate break-even thresholds

Step 5: Validation & Review

Before presenting:

• Verify all formulas link correctly

• Check that balance sheet balances

• Confirm sources = uses

• Review reasonableness of all metrics

• Compare to comparable transactions

• Prepare answers to obvious objections

Common Checks

✓ Pro forma shares = Acquirer shares + New shares issued

✓ PPA intangibles + Goodwill = Purchase price - Fair value of net assets

✓ Interest expense = Average debt × Interest rate

✓ Taxes = Pre-tax income × Effective tax rate

✓ Cash flow statement ties to balance sheet changes

✓ All percentages sum to 100% where applicable

✓ No #REF, #DIV/0, or #VALUE errors

Model Maintenance Best Practices

Version Control:

- Save dated versions (MergerModel_2025-01-30_v1.xlsx)

- Track major assumption changes in change log

- Use Excel's "Track Changes" for collaborative reviews

- Maintain separate tabs for each scenario

Documentation:

- Add comments to all key assumption cells

- Document data sources (where did this number come from?)

- Explain any unusual adjustments

- Keep supporting schedules organized

Flexibility:

- Use named ranges for key inputs

- Build dropdown menus for scenarios

- Color code: Blue = Input, Black = Formula, Green = Link

- Avoid hard-coding; use cell references

Presentation:

- Keep output tabs clean and print-friendly

- Use conditional formatting for quick insights

- Build executive summary dashboard

- Create board-ready charts and graphs

Updates:

- Refresh model as new information arrives

- Update market data (stock prices, interest rates) daily during active negotiations

- Adjust synergies based on due diligence findings

- Revise timing assumptions as integration planning progresses

References

- Rosenbaum & Pearl - Investment Banking: Valuation, LBOs, M&A, and IPOs

- M&A Modeling - Wall Street Prep

- Accretion/Dilution Analysis - Corporate Finance Institute

- Purchase Price Allocation - Deloitte M&A Accounting Guide

- Merger Consequences - McKinsey on M&A

- ASC 805 Business Combinations - FASB

- Credit Metrics for M&A - S&P Global Ratings

- Merger Model Best Practices - EY M&A Valuations

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)