DCF Analysis & Intrinsic Valuation

Discounted Cash Flow (DCF) analysis is the foundation of intrinsic valuation in M&A. This guide covers how to build robust DCF models and apply intrinsic valuation principles to acquisition targets.

What is DCF Analysis?

Definition: DCF analysis values a company based on the present value of its projected future cash flows.

Core Principle: A dollar today is worth more than a dollar tomorrow. DCF discounts future cash flows to their present value using an appropriate discount rate.

When to Use:

- Primary valuation method for mature, stable businesses

- Companies with predictable cash flows

- Long-term hold acquisitions

- Situations where you have good visibility into future performance

When NOT to Use:

- Early-stage companies without revenue

- Highly volatile or unpredictable businesses

- Situations with limited financial information

- Turnaround or distressed situations

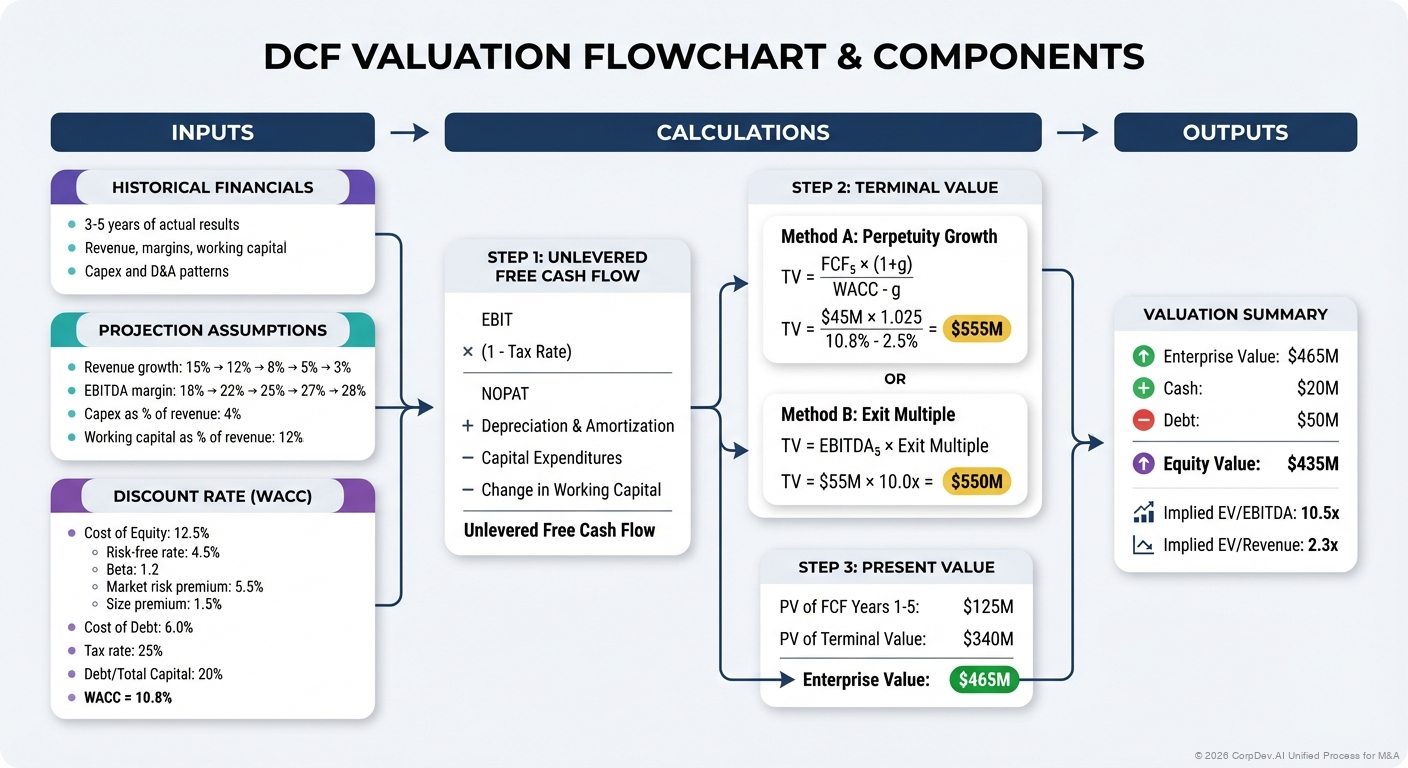

The DCF Formula

Basic Formula:

Enterprise Value = PV of Cash Flows + Terminal Value

────────────────────────────────────

(1 + WACC)^n

Components:

- Projection Period: Typically 5-10 years

- Free Cash Flows: Operating cash generated

- Terminal Value: Value beyond projection period

- Discount Rate: Risk-adjusted required return (WACC)

Step-by-Step DCF Process

Step 1: Project Revenue

Approaches:

Top-Down:

- Start with total addressable market (TAM)

- Apply market share assumptions

- Consider market growth rates

- Adjust for competitive dynamics

Bottom-Up:

- Unit economics × volume projections

- Customer cohorts and retention

- Product/service mix analysis

- Pricing trajectory

Hybrid (Recommended):

- Combine both approaches

- Triangulate to reasonable range

- Stress test assumptions

Example Revenue Projection:

Year 1: $50M (historical base)

Year 2: $58M (+16% growth)

Year 3: $68M (+17% growth)

Year 4: $79M (+16% growth)

Year 5: $91M (+15% growth)

Growth drivers:

- Market growing at 12%

- Gaining 2-3% market share annually

- New product launch contributing 5% in Y3-Y5

Step 2: Project Operating Expenses

Cost of Goods Sold (COGS):

- % of revenue (typically 30-70% depending on industry)

- Scale efficiencies over time

- Input cost inflation

- Mix shift impacts

Operating Expenses:

- Sales & Marketing (often 15-30% of revenue)

- R&D (varies widely, 5-25%)

- G&A (typically 10-20% of revenue)

- Model as % of revenue with scale efficiencies

Best Practice: Interview management on unit economics and cost structure

Example:

Y1 Y2 Y3 Y4 Y5

Revenue 100% 100% 100% 100% 100%

COGS (45%) (44%) (43%) (42%) (41%)

Gross Margin 55% 56% 57% 58% 59%

S&M (20%) (19%) (18%) (17%) (16%)

R&D (10%) (10%) (10%) (9%) (9%)

G&A (12%) (11%) (10%) (10%) (9%)

EBITDA Margin 13% 16% 19% 22% 25%

Step 3: Calculate Free Cash Flow

Unlevered Free Cash Flow Formula:

EBIT (Operating Income)

× (1 - Tax Rate)

= NOPAT (Net Operating Profit After Tax)

+ Depreciation & Amortization

- Capital Expenditures

- Increase in Net Working Capital

= Unlevered Free Cash Flow (FCF)

Key Considerations:

Tax Rate:

- Use effective rate, not statutory

- Consider NOL carryforwards

- Factor in international tax planning

- Typical range: 20-30% for US companies

D&A:

- Non-cash charges, add back

- Based on historical % of revenue

- Or detailed capex depreciation schedule

Capital Expenditures:

- Maintenance capex: Keep business running

- Growth capex: Support expansion

- Normalize irregular spending

- Typical range: 2-5% of revenue for asset-light, 10-20% for capital intensive

Net Working Capital:

- Working Capital = (AR + Inventory) - (AP + Accrued Expenses)

- Change in WC = Cash use (increase) or source (decrease)

- Normalize WC as % of revenue

- Watch for seasonality

Example FCF Calculation (Year 1):

EBIT: $6.5M

Tax @ 25%: ($1.6M)

NOPAT: $4.9M

Add: D&A: $2.0M

Less: Capex: ($2.5M)

Less: Increase in NWC: ($0.8M)

Unlevered FCF: $3.6M

Step 4: Calculate Terminal Value

Terminal Value represents ~60-80% of total DCF value, so get it right!

Method 1: Perpetuity Growth

Formula:

Terminal Value = FCF(n+1) / (WACC - g)

Where:

FCF(n+1) = Free cash flow in first year beyond projection

WACC = Weighted average cost of capital

g = Perpetual growth rate

Selecting Growth Rate (g):

- Never exceed long-term GDP growth (2-3% for US)

- Consider industry maturity

- Typical range: 2.0% - 3.0%

- Conservative: Use 2.5%

Example:

Year 5 FCF: $10M

Growth rate: 2.5%

Year 6 FCF: $10M × 1.025 = $10.25M

WACC: 10%

Terminal Value = $10.25M / (10% - 2.5%) = $136.7M

Method 2: Exit Multiple

Formula:

Terminal Value = EBITDA(n) × Exit Multiple

Selecting Exit Multiple:

- Based on comparable company trading multiples

- Typically use median industry multiple

- Often 8-12x EBITDA for quality businesses

- Consider company maturity at end of projection

Example:

Year 5 EBITDA: $22.7M

Exit Multiple: 10.0x

Terminal Value: $227M

Which Method?

- Use both, compare results

- Perpetuity growth is more theoretical

- Exit multiple is more practical

- Average the two if similar

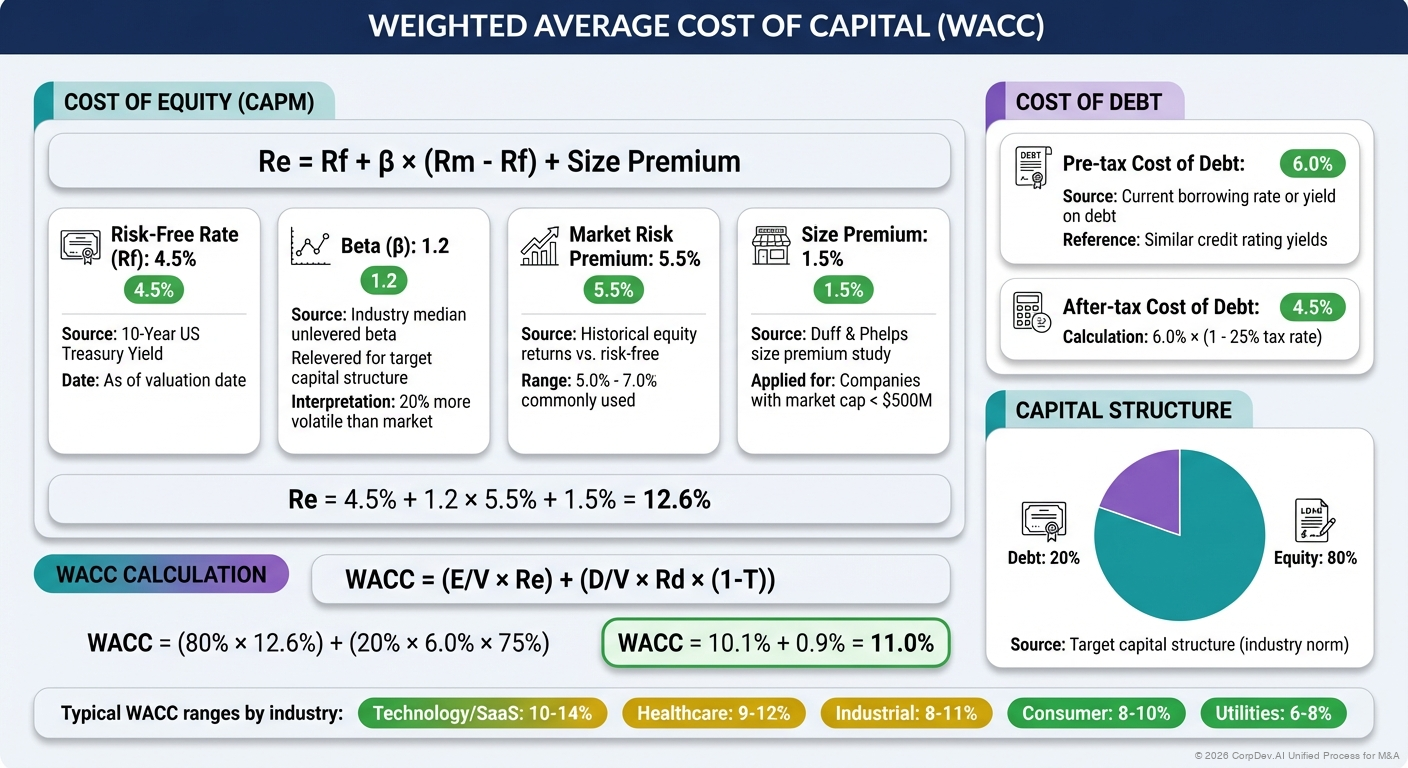

Step 5: Calculate WACC (Discount Rate)

WACC Formula:

WACC = (E/V × Re) + (D/V × Rd × (1 - Tc))

Where:

E = Market value of equity

D = Market value of debt

V = E + D (Total firm value)

Re = Cost of equity

Rd = Cost of debt

Tc = Corporate tax rate

Cost of Equity (Re) - CAPM:

Re = Rf + β × (Rm - Rf) + Size Premium

Where:

Rf = Risk-free rate (10-year Treasury)

β = Beta (systematic risk)

Rm - Rf = Equity risk premium

Component Details:

Risk-Free Rate (Rf):

- Use 10-year US Treasury yield

- Current environment: 3.5% - 4.5%

- Use rate at time of valuation

Beta (β):

- Measure of systematic risk vs. market

- Look up industry beta (Damodaran database)

- Adjust for leverage if needed

- Typical range: 0.8 - 1.3 for most industries

Market Risk Premium (Rm - Rf):

- Historical average: 5-7%

- Common assumption: 5.5% - 6.0%

Size Premium:

- Smaller companies have higher risk

- Add 1-5% for small/mid-cap companies

- Based on company market cap decile

Example Cost of Equity Calculation:

Risk-free rate: 4.0%

Beta: 1.2

Market risk premium: 5.5%

Size premium: 2.0%

Re = 4.0% + (1.2 × 5.5%) + 2.0% = 12.6%

Cost of Debt (Rd):

- Use current borrowing rate

- Or implied yield on existing debt

- Typical range: 4-8% depending on credit quality

Target Capital Structure:

- Use target debt/equity mix

- Not current capital structure

- Industry norms: 10-30% debt for most

- Acquirer's typical leverage is reasonable

Example WACC Calculation:

Cost of Equity: 12.6%

Cost of Debt: 6.0%

Tax Rate: 25%

Target D/V: 20%

Target E/V: 80%

WACC = (80% × 12.6%) + (20% × 6.0% × (1 - 25%))

= 10.1% + 0.9%

= 11.0%

Step 6: Calculate Present Value

Discount Each Year's Cash Flow:

PV = FCF / (1 + WACC)^n

Where n = year number

Example:

Year 1 FCF: $3.6M / (1.11)^1 = $3.2M

Year 2 FCF: $5.1M / (1.11)^2 = $4.1M

Year 3 FCF: $6.8M / (1.11)^3 = $5.0M

Year 4 FCF: $8.6M / (1.11)^4 = $5.7M

Year 5 FCF: $10.5M / (1.11)^5 = $6.2M

PV of Terminal Value:

$136.7M / (1.11)^5 = $81.2M

Enterprise Value = $24.2M + $81.2M = $105.4M

Step 7: Calculate Equity Value

From Enterprise Value to Equity Value:

Enterprise Value: $105.4M

+ Cash and Equivalents: $5.0M

- Total Debt: ($10.0M)

- Minority Interests: $0M

- Preferred Stock: $0M

= Equity Value: $100.4M

Per Share Value (if applicable):

Equity Value / Shares Outstanding = Price per Share

$100.4M / 10M shares = $10.04 per share

Complete DCF Example

Target Company: SaaS business with $50M revenue

Revenue Projections:

Y0 Y1 Y2 Y3 Y4 Y5

Revenue $50M $58M $68M $79M $91M $105M

Growth - 16% 17% 16% 15% 15%

Margin Projections:

Y0 Y1 Y2 Y3 Y4 Y5

Gross Margin 70% 71% 72% 73% 74% 75%

EBITDA Margin 10% 13% 16% 19% 22% 25%

Free Cash Flow:

Y1 Y2 Y3 Y4 Y5

EBITDA $7.5 $10.9 $15.0 $20.0 $26.3

- Taxes @ 25% (1.9) (2.7) (3.8) (5.0) (6.6)

+ D&A 2.3 2.7 3.2 3.6 4.2

- Capex (2.9) (3.4) (4.0) (4.6) (5.3)

- Δ NWC (0.8) (1.0) (1.1) (1.2) (1.4)

FCF $4.2 $6.5 $9.3 $12.8 $17.2

Terminal Value:

Year 6 FCF (2.5% growth): $17.6M

WACC: 11.0%

Terminal Value = $17.6M / (11.0% - 2.5%) = $207.1M

DCF Valuation:

PV of Year 1-5 FCF: $37.5M

PV of Terminal Value: $123.0M

Enterprise Value: $160.5M

+ Cash: $8.0M

- Debt: ($15.0M)

Equity Value: $153.5M

Implied Valuation Multiples:

EV / Current Revenue: 3.2x

EV / Year 1 Revenue: 2.8x

EV / Current EBITDA: 32.1x

EV / Year 1 EBITDA: 21.4x

Sensitivity Analysis

Always conduct sensitivity analysis on key assumptions!

Key Variables to Sensitize:

- Revenue growth rate

- EBITDA margin

- WACC (discount rate)

- Terminal growth rate

- Terminal multiple

Example Sensitivity Table (EV in $M):

WACC vs. Terminal Growth Rate:

Terminal Growth Rate

WACC 2.0% 2.5% 3.0%

9.0% $185 $198 $214

10.0% $165 $176 $189

11.0% $148 $157 $168

12.0% $133 $141 $150

13.0% $121 $128 $135

Revenue Growth vs. EBITDA Margin:

EBITDA Margin (Year 5)

Growth 20% 25% 30%

12% $130 $145 $160

15% $145 $161 $177

18% $162 $179 $196

Common DCF Pitfalls

1. Overly Optimistic Projections

Problem: Hockey stick projections with unrealistic growth

Solution:

- Benchmark against historical performance

- Compare to peer growth rates

- Stress test downside scenarios

- Get management to explain trajectory

2. Terminal Value Dominates

Problem: 90%+ of value in terminal value

Solution:

- Extend projection period

- Re-evaluate growth assumptions

- Consider if business model is truly sustainable

- May indicate overvaluation

3. Circular References in WACC

Problem: WACC depends on capital structure which depends on valuation

Solution:

- Use industry average capital structure

- Or iterate to converge on consistent structure

- Or use acquirer's target capital structure

4. Ignoring Working Capital

Problem: Forgetting working capital impacts cash

Solution:

- Model working capital as % of revenue

- Understand days sales outstanding, inventory turns, etc.

- Growth consumes working capital

5. Inappropriate Discount Rate

Problem: Using wrong risk-adjusted rate

Solution:

- Match risk profile of business

- Consider size premium for small companies

- Use unlevered beta for enterprise value

- Benchmark against comparable companies

6. Not Normalizing One-Time Items

Problem: Non-recurring items distort projections

Solution:

- Adjust for one-time expenses/gains

- Normalize to sustainable run-rate

- Remove acquisition-related costs

7. Double-Counting Synergies

Problem: Including synergies in both DCF and price

Solution:

- DCF should value target standalone

- Pay for synergies separately

- Or clearly mark synergy case separately

Best Practices

1. Build Three Cases

Base Case: Most likely scenario (50% probability)

Upside Case: Optimistic but achievable (25% probability)

Downside Case: Conservative scenario (25% probability)

Probability-Weighted Value:

Expected Value = (50% × Base) + (25% × Upside) + (25% × Downside)

2. Triangulate with Market Approaches

Don't rely solely on DCF:

- Compare to comparable company multiples

- Check against precedent transactions

- Use DCF to inform intrinsic value

- Use multiples for market reality check

3. Detailed Documentation

Document all assumptions:

- Revenue growth drivers and sources

- Margin improvement initiatives

- Capex requirements and timing

- Working capital assumptions

- WACC component calculations

4. Management Validation

Pressure-test your model:

- Review projections with management

- Understand key business drivers

- Validate unit economics

- Test sensitivities with them

5. Use Football Field Valuation

Present range of values:

Low Mid High

DCF Analysis $140M $160M $180M

Comparable Cos $145M $165M $185M

Precedent Trans $150M $170M $190M

Implied Range: $145M $165M $185M

6. Link to Strategic Value

DCF shows intrinsic value, but consider:

- Strategic value to your company

- Synergy potential

- Competitive dynamics

- Time value of waiting

- Alternative uses of capital

Advanced DCF Topics

Adjusted Present Value (APV)

Alternative to WACC approach:

Formula:

APV = Unlevered Firm Value + PV(Tax Shield) + PV(Other Effects)

When to Use:

- Changing capital structure

- Significant tax shields

- Multiple financing sources

Real Options Valuation

Value of flexibility and strategic options:

- Option to expand

- Option to delay

- Option to abandon

- Platform value for future acquisitions

Monte Carlo Simulation

Model range of outcomes:

- Define probability distributions for key variables

- Run thousands of scenarios

- Generate expected value and confidence intervals

- Understand risk profile

References

© 2026 CorpDev.Ai Unified Process for M&A

Last updated: Wed Jan 29 2025 19:00:00 GMT-0500 (Eastern Standard Time)